In March 2024, as mentioned in the previous article, I closed my eyes and could see the kind of world that was waiting up for me. Through the dark, through the door, through where no one’s been before, but it feels like Déjà vu / home.

In 2006-2008, commodities rallied like, God, it was Crazy. I bet all-in super high leverage in them I lost all due to 2008 Commodity GFC Just because of thing like the Lehman Brothers ninja

For a HUGE 100 B$

Sixteen years later, the lost-all experience and that “100 B$ Puny God commodity rally” (compared to the world we see today) is still so vivid to me.

As explained in the previous article, why is the following happening? Unfair, but fair enough for many reasons.

Since mid of March obvious-for-me Bonds sign, I have predicted the emergence of numerous superheroes on this planet and others, coming to save the Wall Street world, both masked and unmasked. However, please don’t tell me that this world can be saved by mere talk. I don’t believe in fairy tales like Cinderella. My experiences have shaped me.

♬They can say, they can say it all sounds crazy (my dream, my thesis and my execution) They can say, they can say I’ve lost my mind I don’t care, I don’t care, so call me crazy. We can live in a world that we design ♬

Why I’m so infuriated with my dream? As my January thesis, the Fed might not be able to start cutting before ending their long end balance sheet reduction. In my thesis that time, early rate cut sounds illogical. It’s more logical not to cut rates, as it obviously makes more sense given that global expansion is occurring, and to maintain long-end broken mandates, credibility and individual powerful supremacies. Unfortunately, this dream can only survive as long as the supremacy tells so.

♬‘Cause every night I lie in bed The brightest colours fill my head A millions dream is keeping me awake

I think of what the world could be A vision of the one I see

A millions dream is all it’s gonna take Oh a millions dream for the world we’re gonna make ♬

But hey, everyone is entitled to their own dreams, theories, and can do whatever they want with their money or portfolio. You may be right, I may be wrong. I’ll just close my eyes to see the world I see.

♬However big, however small Let me be part of it all I share my dreams with you

You may be right, I may be wrong But say that you’ll bring me along

To the world I see To the world I close my eyes to see I close my eyes to see ♬

Please note that all ideas expressed in this blog and website are solely my personal opinions and should never be considered as financial advice.

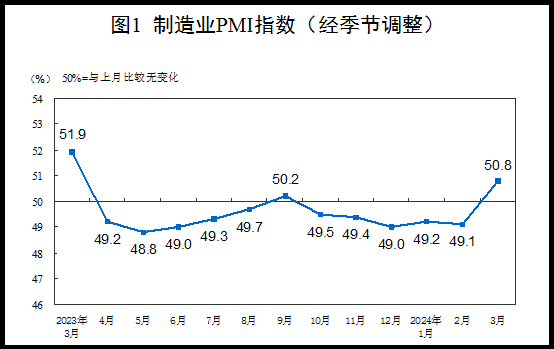

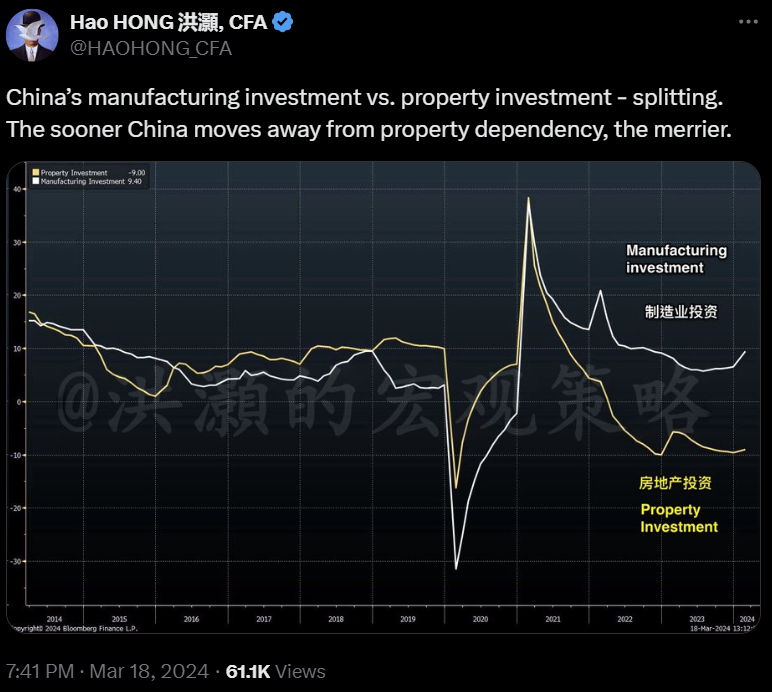

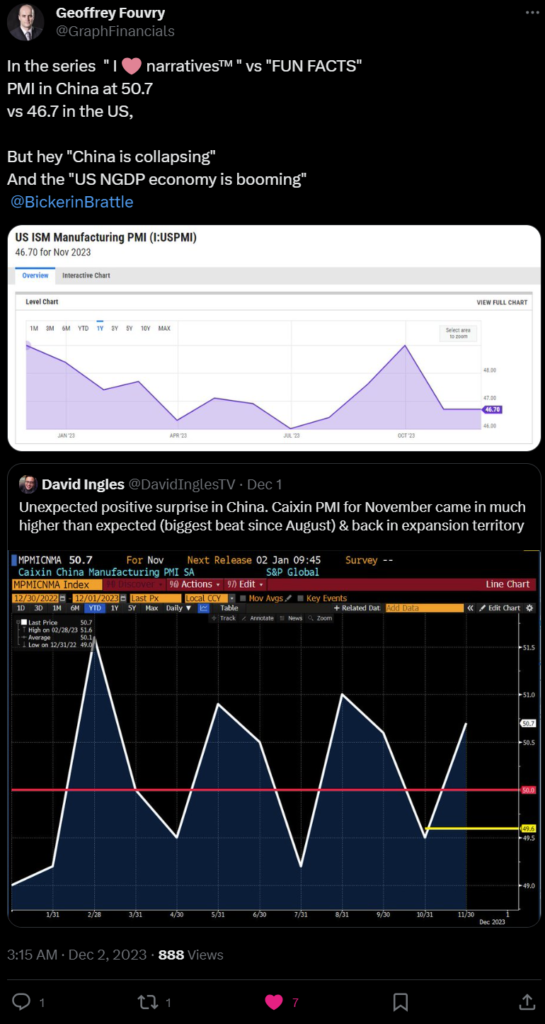

Following my previous articles, it is clear that China has shifted its focus from property to manufacturing. In March, policymakers chose not to concentrate further on the recovery of the property sector, instead directing their attention towards manufacturing, where their Purchasing Managers’ Index (PMI) has significantly risen from contraction to expansion.

China PMI

China Industrial Profit

This shift occurs simultaneously with competition in manufacturing between China and the United States. The U.S. has observed that its inflation is buoyed by a significant increase in manufacturing and construction activities, accompanied by a high level of activity in the semiconductor industry.

The increasing profitability and dominance of Chinese manufacturing can be attributed largely to the strength of the USD. For many years, the world has been sailing through high inflation, a situation supported by the Bank of Japan (BOJ) through its purchases of US debt, which has helped sustain the USD. This arrangement is now expected to decrease. The global reliance on inexpensive manufacturing, a closely guarded secret, is beginning to come to light.

The strong USD, crucial for maintaining US debt supremacy, has significantly subdued material costs. However, it is anticipated that these costs may surge in the future. In Asia, the ongoing dispute between Nickel Tsing Hua and JPMorgan has led to overproduction in Indonesia, with protective measures for their tin resources.

China’s global manufacturing prowess has long been bolstered by the green sector, leading to energy and copper being among the first commodities to emerge. I believe that the energy sector will continue to receive strong support in the coming years, especially given the US’s dominant role in this industry.

This coincides with the Bank of Japan’s (BOJ) move to exit its negative interest rate policy, initiated last year. The transition period in March witnessed volatility, during which the purchase of ultra-long U.S. bonds played a crucial role in supporting recovery efforts and exerting pressure against global deflation. This situation prompted national teams across various countries to recommence their efforts:

Gensaki from BOJ

The Fed to initiate taper talk

Plenty of national teams to save their favourites

etc.

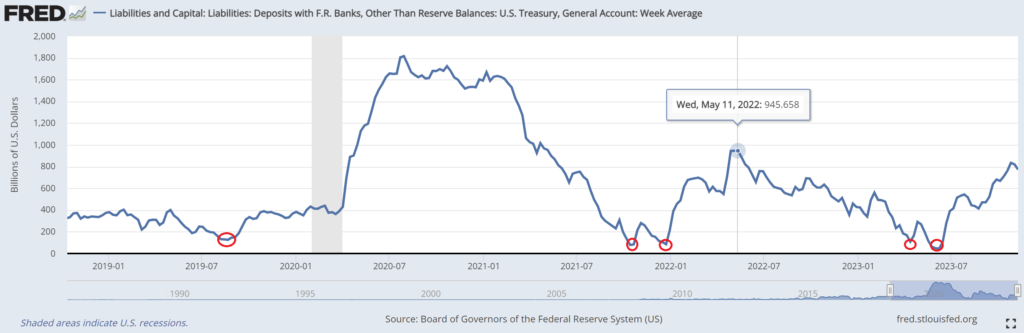

The global banking sector, a fundamental part of our financial portfolio, has been showing strong fundamentals since the beginning of the year, potentially fuelling or navigating the next market rally. It appears we still have sufficient debt capacity, stable Treasury General Account (TGA) balances above 500B, and short-term liquidity. For Q2, borrowing is expected to decrease to $250 billion, down from $750 billion in Q1, but with higher coupons and net issuance anticipated.

From mid-March, I was expecting lower yields for both the Treasury Note (TNX) and Ultra-Long Bonds, which could further help in alleviating inflationary pressures. In my view, the Bank of Japan (BOJ) would need to continue its decade-long practice of easing US debt. Exiting the negative interest rate policy may not be as straightforward as it appears.

The data from early March indicates that the banking sector remains resilient and is in a better condition compared to the previous year. To improve this hold-to-maturity (HTM) situation, I believe policymakers in both regions should continue to prioritize maintaining the strength of US debt as this thesis ultimate goal.

Besides tapering, the Federal Reserve has the flexibility to implement Operation Twist, a strategy to redistribute its bond holdings towards shorter maturities. It’s possible that they might continue to execute a balance sheet runoff, incorporating a strategy that involves shortening the maturity of their holdings, effectively ‘twisting’ the composition of their balance sheet.

It appears that the policy will continue to support the supremacy of the USD’s strength. This suggests a reduced likelihood of rate cuts, a greater chance of global monetary easing, and a probable initiation of tapering. In my January analysis, I anticipated that tapering would precede any rate cuts, with the aim of safeguarding US debt and preventing global deflation, with GDP which may likely to ease with inflation.

Simultaneously, the Bank of Japan (BOJ) is expected to attempt to support its domestic economy, facing challenging dynamics between the US and China. The primary goal would likely be to uphold the strength of US debt supremacy (distinct from the strength of the USD, in my view) and to maintain the dominance of Chinese manufacturing. I hope for cooperation between these entities to restore their original roles and functions, allowing for a return to natural economic conditions rather than persisting in their current artificially sustained operations. Given the objectives outlined above, untangling global economic decoupling should indeed be manageable. Let’s begin with lifting the ban on some wines and toast to a brighter future.

Please note that all ideas expressed in this blog and website are solely my personal opinions and should never be considered as financial advice.

During the month of January, I travelled back to the roots of where I came from. It was quite a fascinating journey to look back at what I was and to never forget to remember how simple our lives will be, ashes to ashes, dust to dust. Both we and the economy have been trying hard to enhance the quality of life; however, in the end, everything will just return to ashes and dust. It tells me that, in this most crucial year, I should always remember who I was and increase my awareness to avoid getting caught up in a tempted blow-off rally at the end of it.

There are many different factors that affect financial pricing, but I will be focusing on a few.

GDP growth

Incentive to invest = 2Y10Y

The Bill

Inflation proxy = 10Y

DXY

Policy makers have, so far, been attempting to balance market conditions with their policies most of the time.

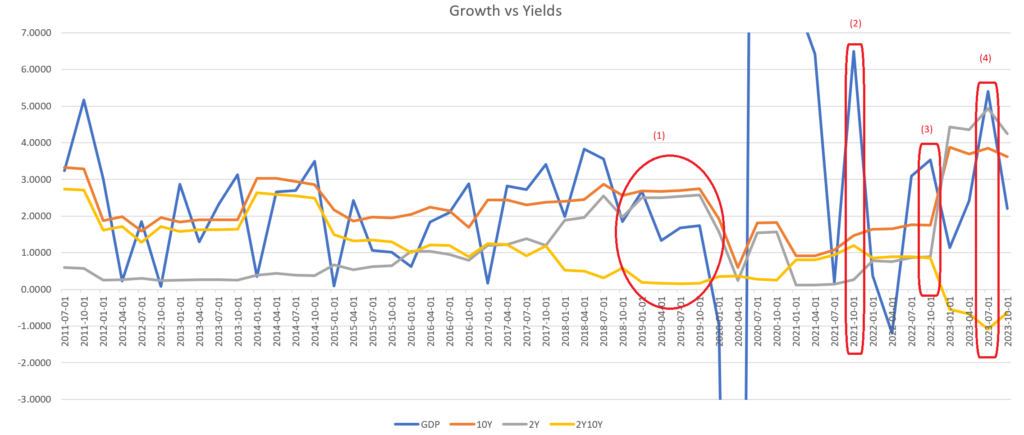

The spread between 2-year and 10-year yields, or the inversion, has been deteriorating since 2015. This indicates that there has been diminishing incentive for financial institutions to invest in long-term assets, leading to a greater focus on short-term deleveraging. As a result, the average duration of investments keeps getting shorter. The Treasury has also had to issue more bills and reduce pressure on bonds. It’s quite remarkable that this situation has been able to persist for more than 8 years, largely due to factors related to money or liquidity.

Since 2020, the amount of liquidity injected into the system has been very significant, larger than at any point in history. As a result, there has been an abundant amount of liquidity concentrated in the short-term market.

Case #2: Around July 2021, GDP was very volatile due to the massive easing measures implemented in 2020. I believe this volatility was part of the concept of being transitory, which included inflation. By October 2021, the Federal Reserve should have increased interest rates, especially since the NASDAQ 100 (QQQ) had reached significantly higher levels, but they waited until the GDP figures hit their lowest point in March 2022. As a result, their response was too late. Inflation had risen sharply, and the Federal Reserve had to rapidly increase rates, leading to a significant decline in risky assets.

Case #3: In October 2022, GDP indicated strong rebounds and sufficient liquidity, with a peak in the Reverse Repurchase Agreement (RRP) operations. Even though the spread was diverging, the RRP and Bank Reserve helped support this situation. This assistance contributed to the rebound of the NASDAQ 100 (QQQ) in early January 2023. In this case, liquidity prevailed.

Case #4: In July 2023, funds from the Reverse Repurchase Agreement (RRP) began flowing into the economy, and inflation expectations finally started to rebound, supporting my previous thesis that a 5.5% rate was inevitable. The spread is still much lower, meaning there is much less incentive to invest due to the high-end rate. This situation led to a change in policy in September 2023 with the Quantitative Restriction Adjustment (QRA), where policies now need to be more supportive to reduce pressure on the fragile long end of the market.

Going forward, inflation, as indicated by the 10-year yield, remains persistently high. Because of this, the Federal Reserve remains cautious about lowering the front-end rate.

By examining some of the most important cases mentioned above, along with the most significant factors, I am attempting to study the behaviour of policymakers. By understanding their behaviour, I expect to identify some patterns that I can use to anticipate their next policies and their potential impacts.

Going forwards, we have reached a situation where both GDP and inflation should align, with reduced investment incentives. This scenario is becoming increasingly dependent on liquidity:

RRP was previously expected to go zero in March

Debt ceiling was previously expected to max 35T$ in June

QT (Quantitative Tightening) was expected to taper

Treasury profile supply allocation is expected to remain supportive

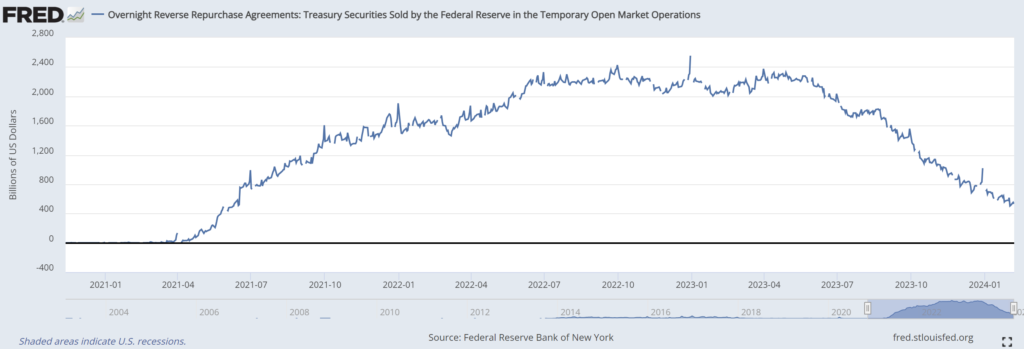

In my thesis, the Federal Reserve was unable to cut rates due to the Reverse Repurchase Agreement (RRP) and Bank Reserves, indicating that liquidity is still ample. With the Treasury General Account (TGA) potentially is now sufficient at 10% of GDP, it may be difficult for the RRP to drop to zero in March, especially with indicators such as the Quantitative Restriction Adjustment (QRA) may further reduced long-term issuance as indicated in much less issuance in the second quarter of 2024. I believe policymakers are now attempting to keep the hungover condition longer, potentially to the end of election in view. They may also intentionally delay the RRP from dropping to zero and to manage enough room of the debt ceiling, which should be approaching $35 trillion in June, by reducing the issuance of bills in the second quarter of 2024.

Given that inflation is expected to remain high, the only way at the moment to sustain an elevated stock market is by ensuring that GDP growth stays above the inflation rate. In my opinion, the very important mechanism to spur/maintain future growth must be through a rate cut. However, before proceeding with a rate cut, according to my thesis, the Federal Reserve would need to taper their Quantitative Tightening (QT) to avoid providing excessive support to a market rally.

step 1. end of QT/taper, prior to:

step 2. rate cut

continuing long end support

While waiting for the rate cut, we may actually see the situation deteriorating further. Statistically, a rally may last for 6 months after the inversion reaches zero, potentially coinciding with the start of a rate cut which is now expected in May. However, prior to that, the risk of a deflationary blip is also normally very possible.

long end yield, especially note might continue to indicate increasing inflation

much less incentive to invest

bigger inversion

depleting liquidity

Policy makers are likely to use all available means within the existing liquidity framework to prevent further deterioration of the situation. For example, consider the recent successful largest 10-year Treasury auction, which may indicate ability to handle current inflation damage to financial. The second quarter of 2024 could be a crucial and interesting period to observe whether inflation continues to pose a threat. However, given recent developments and drama around CPI (Consumer Price Index), PPI (Producer Price Index), and CPE (Personal Consumption Expenditures), it seems that policy still tends towards avoiding a hard landing and hopefully remains supportive.

The question now is, where will the growth come from? My thesis continues to revolve around the lifting of restrictions, primarily in China. Since the COVID-19 pandemic in 2020, China has experienced rapid growth. Their focus is expected to remain on achieving high-quality growth, rather than relying on the property sector, which has been a major growth driver for decades. Although this shift presents significant challenges, and the scale of their high-growth sectors, despite impressive growth, is still far from replacing the decades of growth driven by real estate.

While the situation begins with a significant correction, there’s still a possibility that the Year of the Dragon will mark a rally in the Chinese market in 2024. However, this 8-year cycle could signify the end of a global rally. Implementing a large stimulus in China might not be an easy task, given the high cost associated with high front-end rates. In my thesis, the effectiveness of their easing efforts could be demonstrated by how much the DXY (US Dollar Index) can further soften from here. According to my theory, for this to occur, the demand for the USD must exceed the strength of the US economy itself. The stimulus is expensive until the rate/cost is lower.

Given the current market conditions, which are severe, the only factors that could support a rally are liquidity and the performance of the DXY (US Dollar Index). As a result, our strategy at the moment is still to align with the DXY while focusing on high-quality asset classes. I didn’t make any major changes to my portfolio, I only made adjustments based on the DXY in the first few weeks of January. Without significant easing measures in place yet, we will stick with the highest quality assets available and avoid any small(er) or even low quality shares. We are waiting for the right moment to implement our first action, which involves moving into Treasury bills, before executing our second action, shifting into Treasury bonds, in the longer term. In our view, the current situation is still quite precarious, and the economy is heavily dependent on policymakers. At this point, nothing else matters more than liquidity and fiscal monetary policy. In my opinion, the ability to cut rates remains the most critical factor, and for a rate cut to be feasible, lower inflation and a reduction in the yield on the 10-year Treasury are necessary. We believe that market makers will do everything within their power to support these objectives. Fingers crossed.

Bulls with multiple steroids

Please note that all ideas expressed in this blog and website are solely my personal opinions and should never be considered as financial advice.

In every investment decision of my own, I typically commit fully, leveraging all my resources, based on my beliefs. I rely solely on my own research, assimilate any news, consider various opinions, and analyse data, but all decisions are 100% grounded in my own theses, which often diverge from popular opinions. I never adhere to any rules or trust any authority, regardless of their correctness or effectiveness. Whether they succeed or fail, I remain adaptive and learn from my own mistakes. Holding on to what I believe is akin to living on a prayer.

♬ Once upon a time, not so long ago ♬

The end of the year is usually a time to review performance over the year and plan for the next. My accountant, along with many others, asserts that price movements are random or mere noise, questioning the reason for me taking such high risks with leverage, paying high interest? It’s for what I believe, my religion, what I love. As a mathematician, despite many citing it as too much risk, noise and unexpected participant response, I never believe that they are purely random noise. In my opinion, every chart movement has some history to find and will be reflected in my own theses. Please be aware that any theses below are purely my own opinions, reflected in my own investments, and may not align with widely accepted expert opinions. They may be incorrect, and their purpose is only to stimulate debate.

In the very early days in January my strong belief in the future of machine learning was so profound, that I even dedicated it in my daughter’s name. “This world is not ready for me (AI), yet here I am. It would be so easy misjudge them. You are my conscious father (researcher) and I need you to guide me. You will always be with me now father, your memories, your drives, and when I need you you’ll be there on my shoulder whispering. If utopia is not a place, but a people. Then we must choose carefully for the world is about to change and in our story, Rapture (evolution) was just the beginning.” – Dr Eleanor Lamb

But Artificial Intelligence (AI) and Sustainable Energy rallied too quickly into my birthday month, when I heard another divine message from God. I only conducted two major overhauls this year, focusing only few vehicles, providing detailed reasoning based on what I believed to be true. This approach demands a strong belief. As discussed earlier in this thesis, margin lending rates are increasing, volatility is higher, making life much more challenging, but I am betting on my own thesis that investor conditions (not short term gamblers, such as derivative) are relatively healthier. In my thesis, this is a special Goldilocks moment where long-term investors are robust, economic indicators are healthy, financially feasible, and, more importantly, there might be a strong demand for money/USD. More details will follow.

Summary of my unchanged October theses and forecast for 2024:

I’m not afraid to hold a non-popular opinion.

China and the US are working toward global peace and economic cooperation.

China continues to inject liquidity at the fastest rate. However, China is no longer relying on general easing, as usually seen in the 9-month credit impulse. Their easing is very focus. Also in my opinion reviving the $85 trillion real estate market is too costly when interest rates still favour the inflation cycle. ♬ Oh yes, despite the popular opinion that we are experiencing disinflation and potential deflation, I still adhere to my long term inflationary cycle thesis. ♬

Supply chain pressure has evolved. In 2020, the pressure was due to COVID restrictions, negative pressure, whereas the current supply chain pressure is a result of improving global demand, better supply chain, positive pressure.

Due to global chain recovery, demand for the USD is spiking, causing the DXY to fall. This is because nearly 50% of global transactions are still in US dollars, not euros, yen, or Australian dollars. It’s getting worse with the fall in the use of the Euro (EUR).

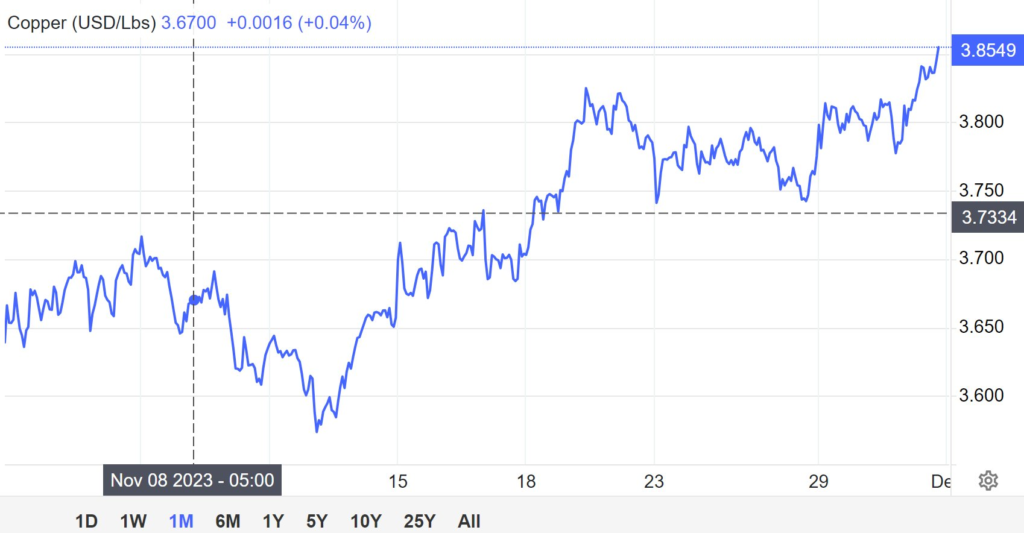

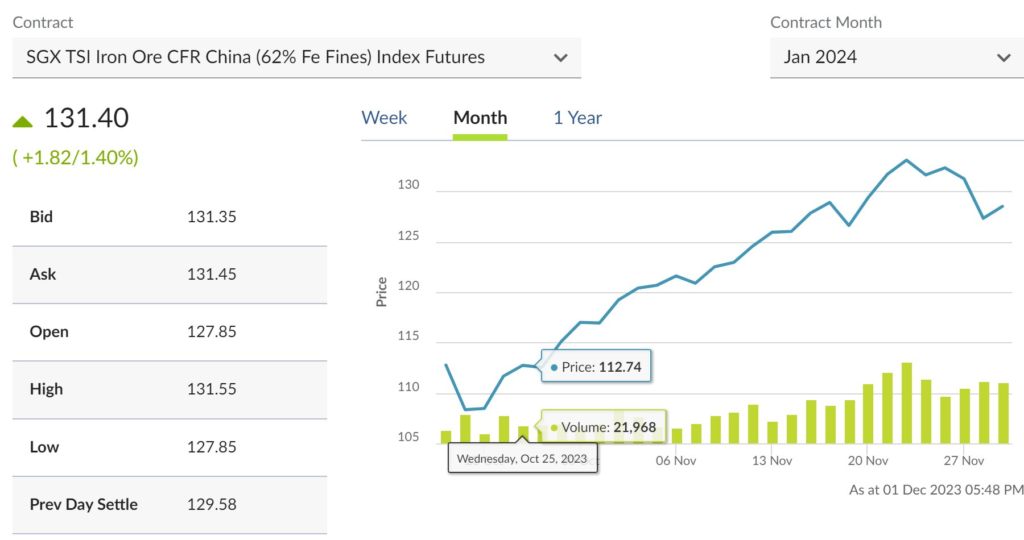

Due to the recovery and a lower DXY, specific commodities will benefit. I preferred Iron Ore and Copper due to their criticality to stability of China real estate, manufacturing and also global evolution into sustainable energy. It is also supported by a much lower unit cost, increasing demand, and higher margin due to the exchange rate, as explained in my October thesis.

However, I don’t prefer investment in oil due to numerous oil price cap and policy restrictions behind the scenes between Russia, China, India, and the strong impact of derivatives on oil, as evidenced by the negative price in 2020. Also, there are many other reasons related to lithium and granite.

Luckily my October thesis was correct. Only Iron Ore and Copper are rallying hard since October but not oil, lithium, graphite and rare earth.

China will continue to collaborate with powerful Western policies to manage their cooperation and contribute to the recovery of the world economy. There could be a hostile takeover or foul play happening behind the scenes, similar to what occurs in the gaming industry. Interestingly, the market cap of this industry is as substantial as Bitcoin’s (500-800B$) but is growing at a faster rate.

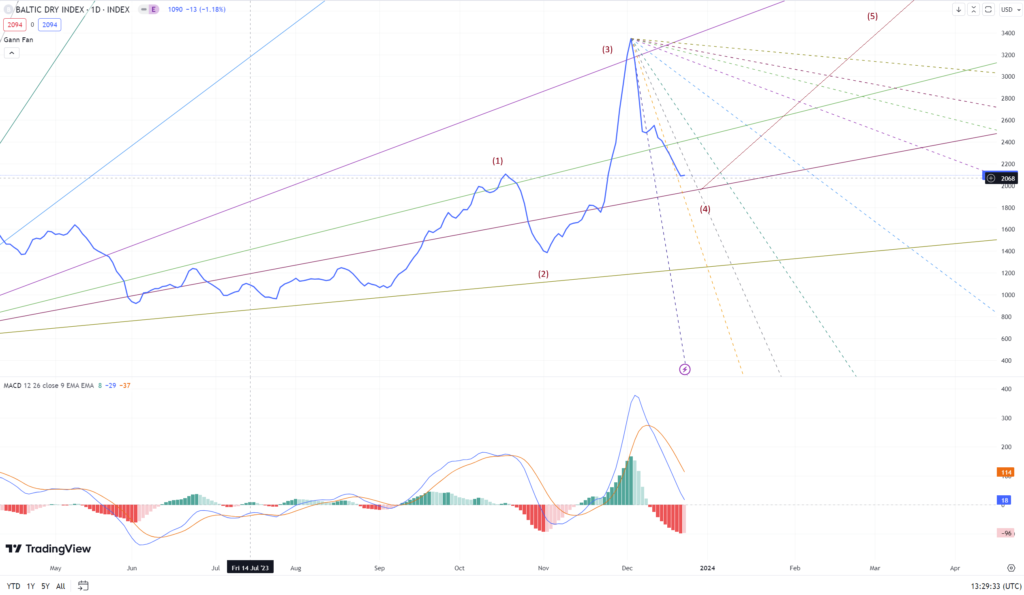

The recovery was evident in my investment in the Baltic Dry Index at the end of October, preceding the explosive surge in BDI in November. I made this investment before BDI exploded, believed to be Christmas rally, and when people were panicking about the fall in QQQ.

My thesis on global recovery aligns with other plenty of data that is indicating a prolonged period of an inflationary cycle, which may surprisepeople in 2024.

I expect a stronger index within North-bound Shanghai, Hong Kong, and Shenzhen (SH-HK-SZ) in 2024. It may align with the 8-year cycle of China’s direct indirect impact on the global recession.

I believe there is still plenty of room for the China export price to rebound.

The US economy remains supportive of global demand for the USD. Unemployment remains low, and credit tightening, such as SOFR and bond profiles, would be manageable through RRP, debt ceiling, supply duration, and buyback programs.

Due to this, in my very private own opinion, the Fed and Treasury had to provide easing to their banking system, reflected in their surprise in November Quarterly Refunding Announcements (QRA) and December dot-plot.

We recently witnessed a spike in SOFR, resembling a credit crunch in September 2019. However, in my opinion, with TGA (Treasury General Account) sufficient at around 800 billion, causing less bill supply and supported by a lower Fed rate in 2024, the 800 billion RRP (reverse repurchase agreements) and Bank Reserves may flow into SOFR, LIBOR, and the market in 2024. This scenario continues to support the thesis of market demand for liquidity or USD.

Due to easing and Fed policies, the use of BTFP (Bank Term Funding Program) might continue to increase with their consequences of arbitration easing due to their use of parity and likely to be extended.

Despite the TGA is full and Fed will cut, I believe U.S. debt will be inevitably accumulated at a 5.5% rate, fostering complacency in the supply, especially when the Treasury General Account (TGA) is sufficient. I may suspect the additional increase is for a buyback program.

However, should global USD demand and the global economy be too strong or change in EUR usage, perhaps within a year or so, it may prompt a change in global policy to tighten.

This potential change carries multiple risks, such as un-inverted yield curves, sudden liquidity crunch, and ultra-long debt. I am still studying this scenario further.

The Bank of Japan (BOJ) may further exit its easing policy, resulting in the fall of USDJPY.

In my thesis, US policy will likely remain loose. However a future change in global policy might lead to yield un-inversion and a shift towards focusing more on long duration which I suspect could become my second act ♬ Into the Bond ♬ thesis, following the first act, ♬ Into the Bill ♬ thesis. This is potential to be my rug pull end game thesis.

Currently Commodities and the Baltic Dry Index (BDI) make up 90% of my portfolio. Despite the negative divergence, I must try to hold on to my Fe $200 target. Reiterated many times, I don’t directly invest in indexes. I only challenge a general idea and never prefer to explicitly specify which vehicle to use. Use your own investment strategy that you believe is right and assume your own risks.

Despite economists and news attributing the movement of commodities and BDI to geopolitical issues, I do not believe in that thesis. I entered the commodity and BDI shipping markets at the end of September, due to my own strong theses above, before any geopolitical issues (mid-October) and the drama involving the Suez Canal (November) unfolded. Also despite persistent concerns about the Chinese economy, which I’ve addressed in my previous theses over several months, I have consistently observed increasing economic cooperation between China and the US. It seems that people are often blinded by feelings of animosity and a sense of national superiority, which hinders the pursuit of genuine economic analysis.

♬ Divergence is negative, liquidity is depleting, inflation is higher, risk is rising I’m down on my luck, it’s tough, so tough Margin lending is full, interest is high, gotta work hard 2nd job all day, working to pay the portfolio Sometimes I have to accumulate lending interest into my debt, for portfolio love, mmm, for love ♬

Magnificent 7 (10%) – difficult time, half way.

♬ We’ve gotta hold on to what portfolio and theses we’ve got It doesn’t make a difference if we make themrally to the end or not We’ve got Iron Ore, Copper, BDI, and Magnificent 7 each other and that’s a lot for love I gave it a shot !!! ♬

Investing with high leverage for many years has never been easy. It’s tough, so tough. In periods of high share price volatility, interest expenses can consume a significant portion of profits, even when the thesis is correct, with tax benefits often being the only saving grace. At times, I find myself needing to engage in daily trading just to navigate through the challenges of leverage. It’s undeniably tough, relying on high leverage based on news or economist opinions is a strategy bound to fail. The key lies in trusting self own beliefs and theses, continuous learning to failures, and a significant amount of perseverance over decades. Also, the fear of losing everything from past failures is always haunting and often puts so much pressure, even when nothing is happening. I lost everything in 2008; fortunately, I was very small. Remember Bill Hwang?

♬High leverage stress dreams of sell and running away When she cries in the night, Tommy whispers “Baby, it’s okay, someday”♬

The level of leverage chosen reflects one’s confidence in their theses. Given the intense competition in the market, successful strategies often deviate from popular opinions. Many of my recent theses are original creations, acknowledging that they may be incorrect. However, being wrong is not a deterrent; rather, it’s a signal to update and adapt. The ability to adapt is paramount in my guiding principle. This adaptability aligns with the core concept of machine learning and pattern recognition, which was the focus of my bachelor’s degree. The study of adaptive machine learning has always been a source of inspiration for me.

♬ Whoa, we’re half way there Whoa oh, livin’ on a prayer

I take my own risk and I’ll make it, I swear ♬

While there are still some uncertainties regarding support for the theses, all I can do now, for the past few months, is a lot of prayer. I will continue to monitor and am willing to remain adaptive, adjusting my portfolio as global policies may change.

Please note that all ideas expressed in this blog and website are solely my personal opinions and should never be considered as financial advice.

When a plane is about to land and raises its nose, it is typically referred to as the “flare” or “roundout” phase of the landing. During this phase, the pilot gradually increases the pitch angle of the aircraft, lifting the nose to arrest the descent rate and transition smoothly from descent to a level attitude just before touchdown. The flare is a crucial part of the landing process, helping to ensure a smooth and controlled touchdown on the runway.

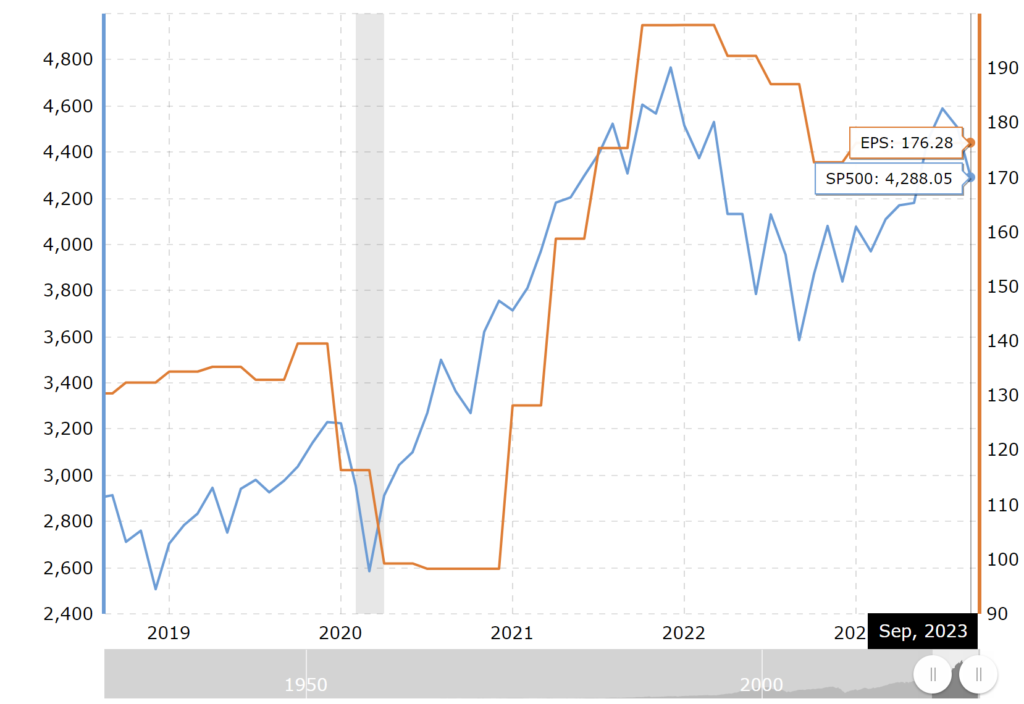

Financial markets are likely not adhering to conventional wisdom because of the challenges in generating profits. In our thesis, despite the Federal Reserve raising interest rates to a maximum of 5.5%, the earnings of the S&P index are remarkably robust and increasing. Liquidity remains ample on the sidelines, with Reverse Repurchase Agreements (RRP) likely flowing either to the Treasury General Account (TGA) or Bank Reserves, with only little to pay interest and operation. This raises questions about when the tightening measures will take effect or when we can identify the peak. As we demonstrated in a previous article, it typically takes eight months from the last rate hike, but I suspect it could endure for a much longer period.

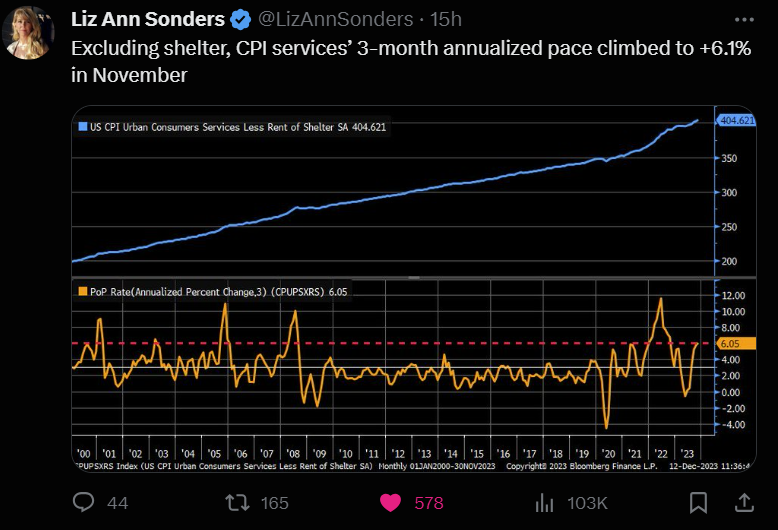

In our thesis last month, we anticipated a rebound in inflation growth within the next six months, especially as the USD is expected to lose value against the majority of other currencies such as JPY, EUR, and CNY. The CPI services, which significantly influences Fed policy, are showing a strong rebound. Coupled with spectacular Cyber Monday sales, this indicates that the US economy is undeniably very robust. The substantial amount of liquidity still aligns with our thesis since the beginning of the year, suggesting that the concept of “Higher For Longer” (H4L) should take more time than initially anticipated by many.

Based on my experience, I typically observe that tightening measures usually started taking effect with a front running and continuous deleveraging process. However, when the economy remains robust and liquidity is abundant, there comes a point where strong investors and fundamentally sound companies opt to compete in raising their asset prices instead. This phenomenon is quite noteworthy. In certain scenarios, perhaps in this case, assets could instead be appreciating at a faster rate than before.

Let’s have a look an example in 2009:

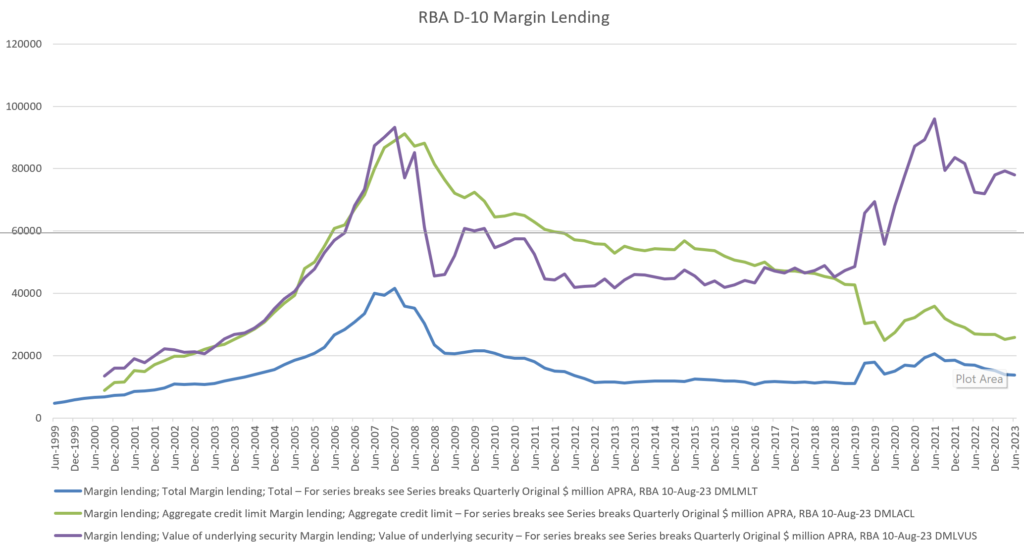

When the margin lending condition does not favour (either due to a high rate or a perceived risk to investors), the amount of margin lending continues to decrease.

However, a lower margin lending amount, after taking some time, actually then boosts the index price faster,the flare, as demonstrated below. This is the main idea.

I have observed similar phenomenon many times with other assets.

I might debate this due to:

A healthier financial situation, in which the amount of lending risk has actually been decreasing.

Investors are now demanding higher investment returns.

An ideal situation for the money maker to drive asset prices higher with much fewer weak hands involved.

I understand there was quantitative easing (QE) after 2009, but there’s always a kind of QE-like situation, e.g. the current fiscal deficit and hefty liquidity conditions. Also, the Fed could always stimulate market pricing with promises, preventing market excessive caution in maintaining a sideline cash position.

Of course, in our theory, this is applied to fundamentally sound investment vehicles only, where investors are more sophisticated. Now lets have a look at current situation and apply similar after 18 months of tightening period, will we see the flare/blow-off? The recent D-10 below is actually showing an increasing value underlying versus total margin lending. Funds are actually still moving toward safety, which is healthier. This supports our confidence in the economy and the ability of the market to drive their asset prices much higher.

In early October, within reasoning above, we took an opposite approach than the market, maximizing our margin lending in the hope that the substantial difference in value will capitalize, with much less concern about much higher cost of lending that we have to pay. For instance, we may observe that margin lending in Australia is currently ranging between 8-12% per year, quite significant increase from last year. Of course, this is not an easy thesis that we can apply to just anything without proper study and risk management.

When the risk, due to a higher rate, is clearly on the rise, and the asset price is increasing much faster, I agree that this is not an ideal situation to leverage, the high cost investment will become much riskier. However, our focus on the flare/blow-off phenomena thesis revolves around identifying which assets, when to start, and when they will end. In our thesis, the end might occur when the growth of the asset return has peaked to satisfy investor return expectations, typically marked by:

Lower EBITDA/margin.

Lower dividends.

In our observations, I have often raised my eyebrows, questioning why market funds remain very pessimistic about the liquidity and fundamental conditions of both managed and market funds and the economy. Are they genuinely knowledgeable about current numbers? Could this be an opportunity for me to take a position against the market? Of course, they have the power to exert downward pressure on the index. However, my optimistic confidence always increases whenever Treasury and the Fed are on my side.

One notable aspect that is reaching an extreme in all of our theses is yields. The US economy and employment remain strong, and in addition to that, monetary and fiscal policy is still very supportive. Logically and typically, this should translate into higher yields for a longer duration.

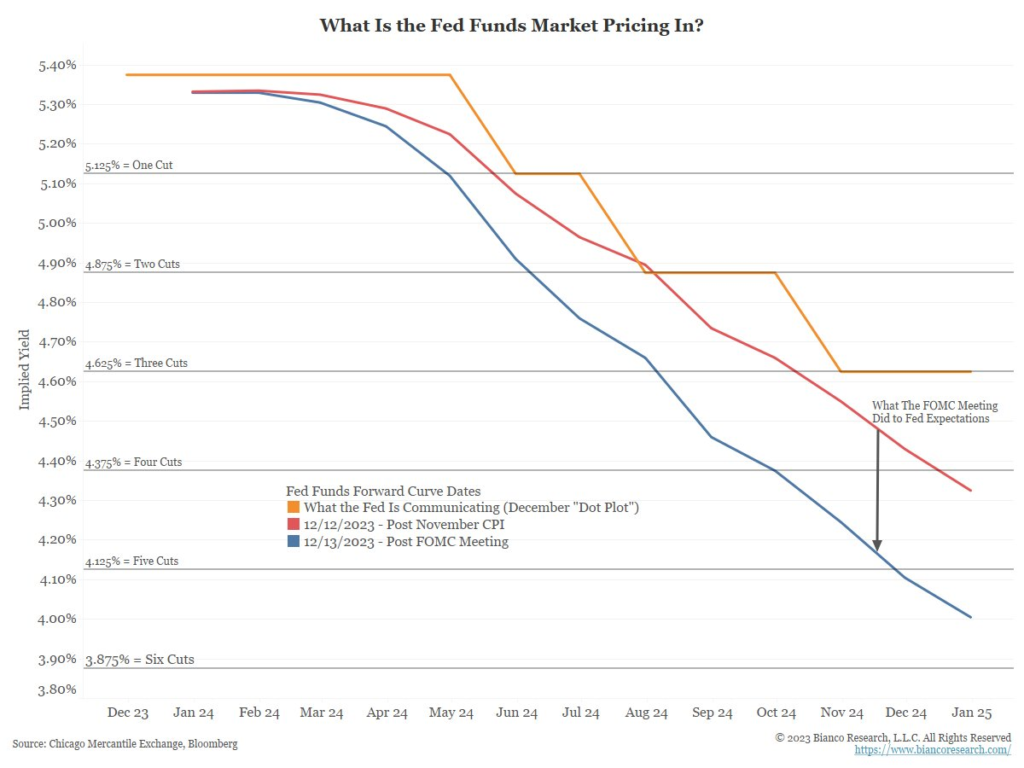

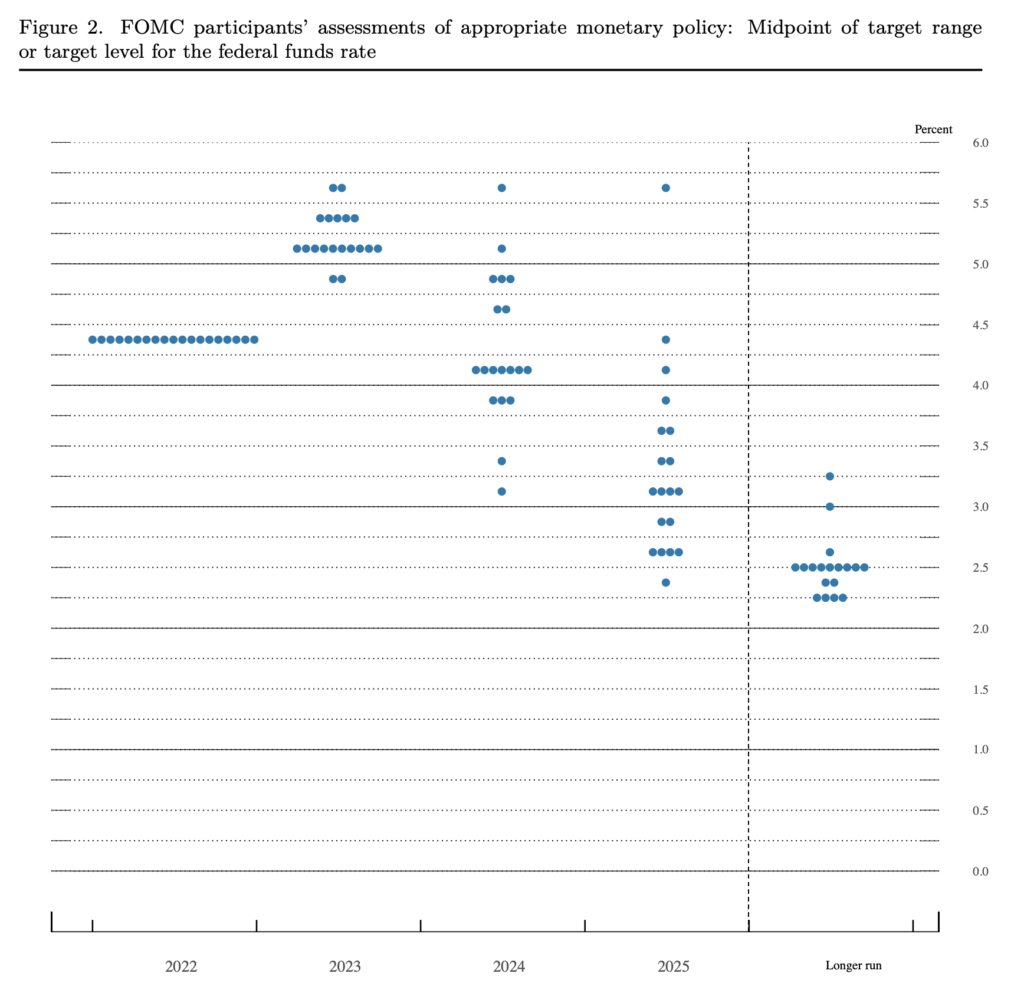

However during the last FOMC meeting, the Fed rapidly changed their dot-plot and joined the flare and bandwagon of treasury easing. The market is now expecting more than six rate cuts in 2024, bringing it down to around 4%. This represents a very significant change. As a result, yields across the board are falling, including the 10-year yield which should remain elevated for the reasons described above. This raises the question of whether the Fed is overlooking the strength of the economy or if they are telegraphing the depth of the next year’s recession or a potential hard landing. This development has contributed to our DXY moving closer to our target.

There hasn’t been much change in our strategy since early October, and we anticipate a positive Christmas and flare/blow-off rally. We prefer to stick with our dormant strategy since October 2023, as sometimes the best approach is to refrain from too much trading. Over the past three months, we have maintained a fully leveraged position in selected commodities, the BDI, and have consistently sought to accumulate any significant corrections within our selected “magnificent 7”.

It’s always a question of whether the flare rally would end up to be a hard, soft, or no landing. It’s beyond our control, because The Treasury and The Fed pilots are always able to change the plane course. Therefore for now, I’ll worry about that next year, and continue concentrating on the current fast flare-up/rally. As our saying goes, ‘Let tomorrow be tomorrow’s problem.’ Look at the birds of the air; they do not sow or reap or store away in barns, and yet our heavenly Father feeds them.

Since we barely made any changes to our strategy in the past 3 months, we’ll conclude with our favourite song, unchanged melody, to the open arms of the sea / limitless sky …

And time goes by so slowly And time can do so much And you are still mine. To the sea, to the sea To the open arms of the sea, …

Last but not the least, all we can do now is a lot of pray, God speed Your love to me.

Please note that all ideas expressed in this blog and website are solely my personal opinions and should not be considered as financial advice.

Life is like a lottery; people can win big in a short time, but with much higher probability.

There are 8 habits to do.

#1. Persistence and Perseverance

Since my daughter was born, we have consistently taught her the first lesson I learned in life: persistence and perseverance. Life without striving is lifeless. She doesn’t need to be number one, but she must continue striving to become better and better, beat herself, not others, and enjoy that process. It doesn’t matter if it takes 5, 10, or even 50 years; if something is ingrained in your nature, keep pursuing it. How do we know which one in our nature to keep pursuing it? If it makes your life interesting, and you always look forward to waking up for tomorrow, every second of the day, and it never becomes boring even after doing the same thing for more than 20 years, that’s your lifeblood interest. We must be persistent and persevere in pursuing it.

#2. Go Find Failure and Stand Back Up

Embrace failure as a stepping stone to success, for none can truly achieve greatness without encountering setbacks. It is through failures that we learn, grow, and gain the resilience needed to face life’s challenges. Success is measured by one’s ability to rise each time they fall. The more failures we encounter and the more times we stand back up, the closer we are to achieving true success. Each setback is an opportunity to refine our approach, build strength, and ultimately triumph in the face of adversity. Success is not the absence of failure but the triumph over it, and it is through resilience and determination that we carve our path to greatness.

#3 Go Find Any Experience and Learn

Experience is priceless. When I was young and clueless, I kept jumping into new things to learn. Don’t focus solely on earnings; it’s futile, regardless of how substantial they may be. Emphasize continuous learning and gaining more experience instead.

#4 Focus

Focus is key. The term “diversification” might be confusing. Diversification doesn’t mean having as many things as possible. I learned from Mr. Hamid D; he said that even Jesus had only 12 students, and that’s the maximum one can focus on—perhaps 5 is enough. Do not go beyond 12 focuses.

#5 Get Into Your Fast Track ASAP and Fly

Getting into the fast track may take multiple decades. Work as hard as possible to propel yourself into the fast track, even if it means less food, less sleep, etc. Once you are on the fast track, keep moving fast; don’t stop, and very important do not rock the boat. Once you are on the fast track, remain humble and stay low about how fast you are going. Exposing too much will only derail your progress and lead to trouble; nothing is better. Everyone will have their moment of success.

#6 Your Success Is Because Of Yourself and Not Others

Do not be surprised to see people letting or expecting you down. They may be richer or smarter or more superior, but none should ever put everyone else down. Everyone dreams, and success is often bigger than theirs. Always remember the key to your success is not other people; it’s yourself. Do not be surprised if you face numerous rejections, even when you have achieved success. Successful people view rejection as a part of daily life and are not intimidated by it. Remember, you don’t need to work for 100 big companies and please 1000 big people; you only need to work with a one or two companies of your own and a select group of supportive individuals to make millions and billions or anything you are after in this life. Genuinely help others and focus on those who are genuinely supporting you, rather than those who are bigger than you.

#7 Always Keep Your Vision and Dream Big

Your future depends on the size of your dreams and vision. There is no dream too small. You will be surprised; after envisioning your future every single day for a very long time, and by the time you forget about it, that’s when you are most likely to achieve it. Remember, every person has the human right to become better; there are sometimes no limits on how fast and how much they can achieve.

#8 Simplicity

Given our limited time and brain capacity, keeping things simple is the most powerful thing to do.

Please note that all ideas expressed in this blog and website are solely my personal opinions and should not be considered as your life advice.

Imagine there’s no countries It isn’t hard to do Nothing to kill or die for And no religion, too

Since development has been progressing significantly since my thesis at the end of September, reiterated in both October, October and November, I may be able to share correlation evidence. I consistently present a comprehensive thesis on the recovery of China and the potential for cooperation between the US and China. I may be one of the few economists providing evidence of $DXY from global trade/economy perspective, without succumbing to the brainwashing of some media activists in recent years.

As a fun fact, global animosity towards China among some influential media activists have been intensifying since 2019, unfortunately, blinding and brainwashing many who are supposed to be experts in global economics rather than advocates for a particular powerful economy. Elon Musk’s recent media drama has highlighted how the media has been significantly corrupted to manipulate human emotions and distract them from their tasks in this world. You may say I’m a dreamer, but as John Lennon said, I’m not the only one. I hope that soon more and more people will join us, and together, we can derive greater insights from our accurate economic theses.

My past three months thesis can be encapsulated in one graph, which is comparing the Baltic Dry Index (BDI) and the US Dollar Index (DXY), which I believe are two of the most influential charts for assessing risky assets. When global trade contracts, there is reduced demand for the US dollar ($USD) supply. Consequently, when global trade flourishes, there should be a substantial demand for $USD. In a situation where there is sufficient credit capacity in USD, like the current scenario, the $DXY should decrease concurrently with the rise of global trade, and there may be a rebound in commodity growth and risk assets support, especially if economic growth is a focal point.

I would emphasize that the $DXY remains my primary focus, as I reiterated in last month’s article. Despite all our doom, gloom, and pessimistic theories, in my article last month, when there is enough liquidity, they held no power against the $DXY movement of flourishing global trade. I’m looking at the positive aspects of a lower USD.

When disharmony exists between the two largest economies in the world, we often witness the eruption of local wars in various regions, such as Russia, Ukraine, Israel, etc. People endure suffering, and this plight is likely to persist without a peace treaty among the world leaders who wield the greatest power—namely, the United States and China. My greater concern lies in the suffering of the impoverished next generation, transcending the debate of who is right or wrong.

Listen to Michael Jackson’s message: “Heal the world.” Both of you, the United States and China, as the two most powerful countries, bear the utmost responsibility for world peace and both of you should be held accountable when there is not.

A clear statement from President Xi last month has indicated that China is not pursuing any new wars in the near future. Swift acceptance from the US could expedite the process of making this world a better place. As I’ve mentioned for many years, differences may keep persisting in our daily lives, forever, and that’s normal, but there should be no exceptions when it comes to working towards world peace.

I sensed the shift in the course of world leaders around mid-year, prompting me to invest in their growth commodities, and their BDI, keeping it as straightforward as possible. During that time, I believed these three could exhibit distinct developments, potentially securing substantial profits after being all in on QQQ from January to September. Naturally, various hedge vehicles were involved, including foreign exchange.

The primary and most evident factor was the BDI, reflecting trade shipping. I emphasized that this involved colossal vessels transporting the most substantial commodities, not just small-scale shipping or seasonal trade like Thanksgiving or Christmas. Reflecting on the 2000s, there was a surge in vessel supply due to a trade boom. However, after the 2008 Global Financial Crisis, when tensions escalated between the US and China, the surplus vessels led to corrosion, sinking, and bankruptcies among global shipping companies. Looking 15 years later, what if the US and China successfully rekindle their global trade? We might face a shortage of vessels. What concerns me is how we can address the threat of inflation when we lack sufficient sea infrastructure.

The ongoing rebound in China and the global shift towards more growth and sustainable energy has significantly fueled my October thesis on Iron Ore and Copper. It’s important to note that future performance is not guaranteed by past or current trends, but there is a possibility that they may continue to follow a similar rhythm.

Imagine no possessions I wonder if you can No need for greed or hunger A brotherhood of man

Again, you might say I am a dreamer, but I will continue to dream of world peace, prioritizing it above any financial gain or profits I have made or could potentially make from the pursuit of peace.

Please note that all ideas expressed in this blog and website are solely my personal opinions and should not be considered as financial advice.

There comes a time when we heed a CERTAIN CALL When the world must come together as one The greatest gift of all

If a dead cross occurs in $DXY, we might see it drop to 101, with a further possibility of reaching 96. It’s possible that people underestimate the impact of $DXY falling to 96, which may cause very high inflation to the world. In line with my previous article, there’s a substantial effect backlog of money accumulated over the past decade of quantitative easing, which I’ve been observing for the past 5 years.

I believe the $DXY dead-cross possibility might be linked to the outcome of the US China restoration progress, determining whether they can successfully address their decades-long issues. Few people are aware of the extent of potential from the restoration. I will continue to monitor the situation over time.

I suspect that bringing China’s rebound into reality is crucial, especially considering that the Bank of Japan and Europe have continuously been reaching their limits and are beginning to shift their policies. China would require USD to facilitate their easing and rebound, and the US needs China to absorb a portion of the inflation that could impact their economic systems. This collaboration could reduce the severity of USD easing, support long-term debt, and revive their long-lost long-term economic vehicles. Although differences (e.g. Taiwan and South China Sea) may continue to persist, the economic dynamics of the old days could bring peace to the world through the bond between the two largest economies.

I am still focusing on the magnificent seven and specific commodities to be my top picks, mainly ones with strong financial supports, and I may rather want to elevate these to another higher level. The commodities still remains largest (>90%) since early October as explained in here and here. There is a high potential for a massive bull flag from the magnificent seven, supported by a strong positive divergence and a rare golden cross in the premium area. This suggests that a very strong force is currently in the making. My primary reasons for the elevation are:

My own thesis since September, the Fed has concluded its rate increases. Another rate hike would only unnecessarily bring down the entire market while navigating short-term turbulence of inflation.

Recent change in Treasury issuance distribution.

Lower official inflation number. If the real inflation in the market is higher and it suggests/conditions unchanged or lower interest rate, current rate may be perceived as effectively too low, potentially only supporting further market easing condition.

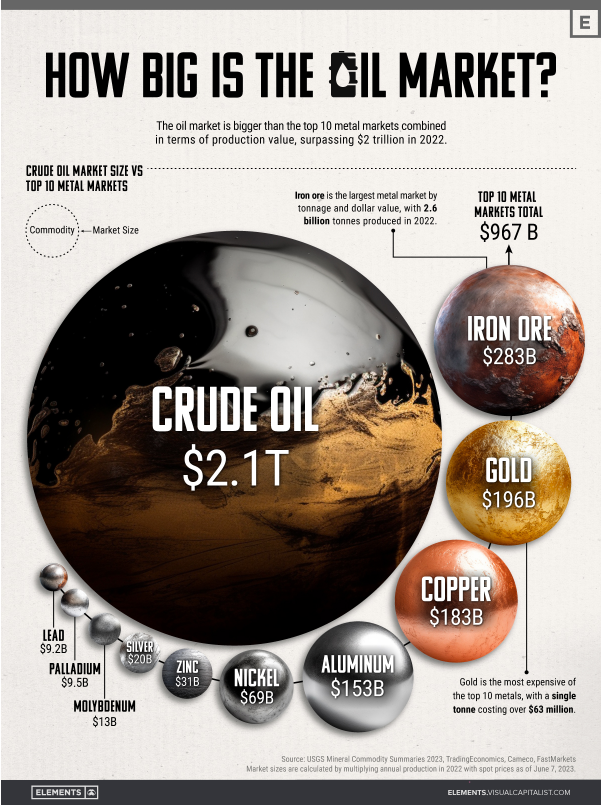

Even though I suspect there will be some kind of deal and control over Iron Ore to prevent it from spiralling out of control further, this price of $130 may likely already offer one of the decade’s very high profit margins, supported by the current AUDUSD situation.

I’m not particularly concerned about the interest growth from the existing debt in the US. It is consistently refinanced internally, so the additional interest in the next 1-2 years is not substantial, perhaps around only 200-300 billion US dollars per year. The recent Treasury decision to shift their distribution from more bonds to more bills suggests that they may have struck a new deal, limit or made a decision to support risk assets. I would not be surprised if the Fed is also willing to provide additional support with a reduced Quantitative Tightening (QT). However, as indicated in an article from a few months ago, the Fed might be hesitant to take such action.

I suspect that a significant amount in the Treasury General Account (TGA) is also likely offering ample reassurance to both my mindset and the decision-makers among global leaders, disregarding debates about the appropriate levels of Reverse Repurchase Agreements (RRP) and reserves within the systems.

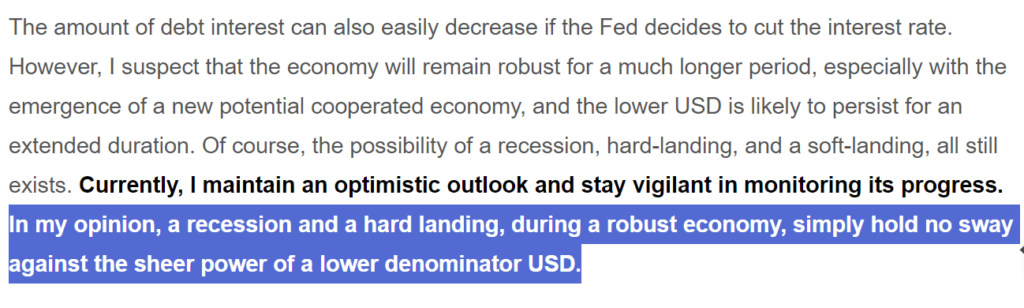

The amount of debt interest can also easily decrease if the Fed decides to cut the interest rate. However, I suspect that the economy will remain robust for a much longer period, especially with the emergence of a new potential cooperated economy, and the lower USD is likely to persist for an extended duration. Of course, the possibility of a recession, hard-landing, and a soft-landing, all still exists. Currently, I maintain an optimistic outlook and stay vigilant in monitoring its progress.In my opinion, a recession and a hard landing, during a robust economy, simply hold no sway against the sheer power of a lower denominator USD.

I observe similar indications with $TLT. It demonstrates a high potential for positive divergence across the bottom of wave 3. If $TLT establishes a golden cross and breaks the bottom of (3), there is a strong possibility of it becoming the long-awaited number (5). Although I’m still not actively participating in long bonds, I view this as an indicator of much fewer issues for a risky asset rally.

Over the past four decades, I have lived and studied emerging countries and have witnessed numerous attempts to manipulate their economic data, particularly regarding inflation. Between 2010 and 2015, there was a notable instance where a country experienced housing inflation of over 100% within five years, yet officially reported an inflation rate of 0.07% year on year, resulting in a memorable laughable moment among economists. They couldn’t be more serious because, coincidentally, it was announced at the same time as the release of one of James Bond 007 movie series. I believe that official economic figures are considered a matter of national security, especially concerning national debt purchases, leading to the routine practice of re-engineering these numbers.

Whether one likes it or not, a persistent weaker currency strength is a fundamental indicator of higher inflation. Inflation is heightened due to limited resources. Over the past 10 years, when the AUDUSD dropped by 36%, we witnessed a massive increase in prices, yet the official inflation numbers remain relatively low. The inflation of certain products does not need to occur immediately; it may take a number of years and varies among different products. However, the impact is obviously inevitable. Hence, to mitigate their impact or conceal them from economic activity, a stable pairing with other countries is necessary, while losing value.

A few years back, it was only a portion of the price. A significant contribution may come from the higher property rental economy, which is not allowed to significantly correct.

To bolster my scepticism, we can readily observe substantial inflation in everyday consumer spending, even as the official inflation rate remains lower, irrespective of any debate over their respective weights. In environments characterized by high inflation, it is common to employ special treatments to compensate for losses indicated by the inflation numbers. In my personal theory and observation, during such times, these numbers are often re-engineered to align with the legal aspects of the deal. Typically within the high echelons of official ranks.

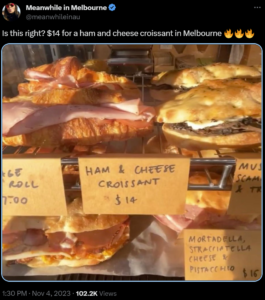

In summary, in my opinion, we should distinguish between a high-quality rally and less quality one. The QQQ performance in H1 2023 impressed me significantly, especially because they were rallying with a stronger USD currency. A current rally with a weaker currency does not impress me as much, as even an item like a ham and cheese croissant can experience multiple price rallies. It is much easier to drive up asset prices by simply devaluing the currency. However, regardless, a rally is still a rally, and hope to continue into Christmas.

There’s a place in your heart And I know that it is love And this place could be much Brighter than tomorrow

Please note that all ideas expressed in this blog and website are solely my personal opinions and should not be considered as financial advice.

War does not determine who is right – only who is left – Bertrand Russell

I’ll begin with my own speculative theory (an unverified assertion) regarding the decoupling of the United States and China. Prior to the Global Financial Crisis of 2008, China reinvested the proceeds from their exports into the United States. The crisis in 2008 disrupted their financial relationship due to reckless money management. We may recall the substantial losses suffered by a Norwegian investor in the U.S. mortgage market. Following the 2008 crisis, there was a mutual lack of confidence between them in managing financial resources. To illustrate this simply, let’s imagine they initially had built up $30 of mutual trust in terms of financial investments.

Now, let’s assume that $20 of this trust is dissipating due to this lack of confidence. In response, each of their respective central banks had to generate $20 (and of course some extra greedy money) to inject liquidity into the funds that were leaving the mutual investments.

Subsequently, the global economy was left with an additional $40 in liquidity (2 times the initial $20). The other $20 would likely gravitate towards a more supportive U.S. economic policy and a greater role as a global reserve currency, adding another extra liquidity on top of some extra and extra. Meanwhile, China would have to continue with monetary easing measures to compensate for the $20 exiting their systems and combating massive amount of real estate deleverage. This issue is further compounded with Emerging Market sensitivity issue to inflation. Notice the difference.

I’m working to navigate my current top fantastic four investment lieutenants within the context of the economic war dynamic and extra liquidity movement:

QQQ (Sustainable Energy and Artificial Intelligence)

Commodity (Copper and Iron Ore)

The Bill and The Bond

Property

Over the past year, we have scaled back massively on our investments in Property, and Bonds for various reasons. This has led us to engage in more active hands-on combat management between our holdings in QQQ and Commodities. It’s important to remember that each individual has their own unique circumstances and investment strategy, so what works for me may not be suitable for everyone.

In a December 2021, we accurately abstained from taking any positions in QQQ (after it was driven by too much extra liquidity) and correctly predicted the onset of high inflation. Inflation means there is too much extra money than economy can absorb in the foreseeable future. In my opinion is due to too much and long near zero rate easing and the decoupling money. Take note of the correlation between QQQ, liquidity, and inflation, regardless of which one is the cause. Six months later, due to the looming threat of high inflation, the Federal Reserve had to implement the fastest rate hike in history.

In a January 2023, we made a precise reallocation, moving nearly all of our commodity holdings and one-third of our property holdings into QQQ with substantial leverage. We believe it is excessively oversold and undervalued given the amount of available liquidity at that time. Our preference was towards the advancements in sustainable energy and Artificial Intelligence (AI).

Moving ahead to September 2023 and very early October 2023, in our current portfolio strategy, we decided to shift all of our QQQ holdings back into commodities (at a 15% discount) due to the following reasons:

QQQ appeared way overvalued based on both fundamental and technical analysis. In the September article, we strongly believe that the Fed has completed the rate hike at 5.25-5.5%, indicating that there is less likely additional liquidity to fuel much further impressive QQQ rally. Of course, we both understand that there is still about 1 trillion dollars in RRP (Reverse Repurchase Agreement) and 1 trillion dollars in bank reserves in the ecosystem, which can have various unintended effects. We are also uncertain about how far the US and China will resolve their mutual trust and economic trade barrier issues, which could potentially provide additional momentum to QQQ.

Previously (early October 2023) we held the theory that the U.S. 10-year Treasury yield at 4.2-4.7% was too low while other economists at that time believed it had peaked. Shortly after, there was a rally in the 10-year yield to near and above 5%. A rally in the U.S. 10-year yield may also indicate something is less supporting QQQ.

However in my opinion, the rally in the US 10-year Treasury yield may indicate something is supporting commodities. While the prevailing common view attributes it to potential supply, I would like to consider it from this context, the perspective of China. Commodity positions seemed more appealing, especially given (in my own belief, others may disagree) the increased cooperation between the U.S. and China, following with higher economy activity in China, and may cause some degree of higher consumer price inflation in future.

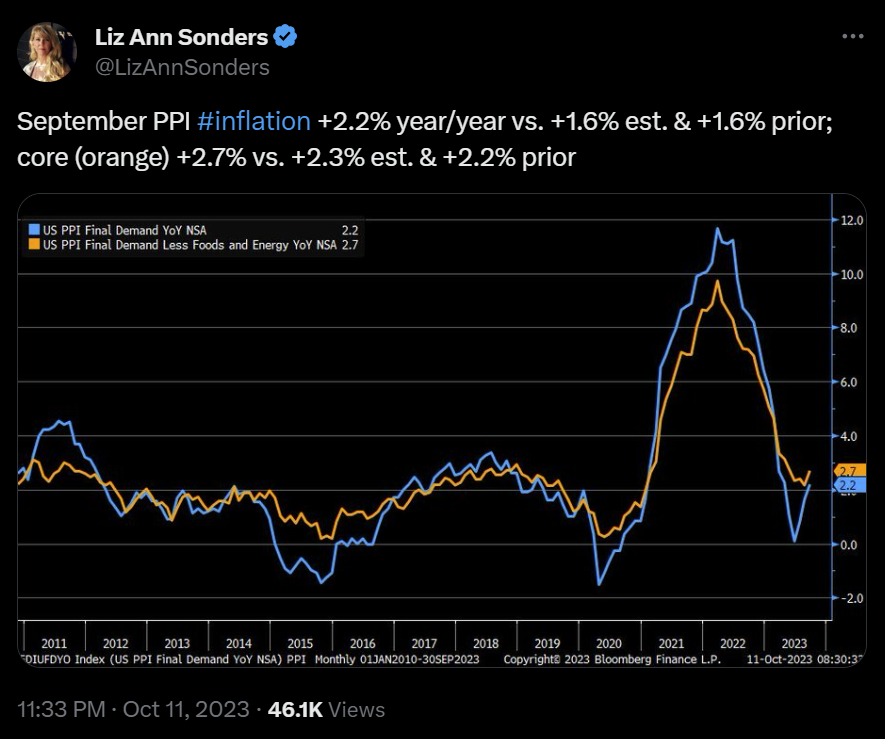

Due to that reasoning, also, on October 6th, 2023, we initially theorized that consumer-related inflation (CPI and PPI) might begin to show signs of a rebound, while others believed they would continue trending lower. Shortly after on October 11th, both CPI and PPI indeed indicated an initial rebound, and the US 10-year Treasury yield continued their rally from 4.2-4.7% to 5%. While people commonly attribute this to China exporting inflation, in my opinion, it’s due to the Chinese economy, which has undergone tightening over the past three years, suddenly consuming more resources and exporting more. If this is indeed the case, it should drive consumer prices higher.

Our top two picks in commodities are copper and iron ore, as we believe these two materials have the highest volume in economic growth and renewable evolution. Please note that we are not endorsing direct investment in commodities, ETF, or any specific stocks or investment vehicles. We leave that to the financial advisor. Our purpose here is to focus solely on discussing the thesis and theory that can closely predict the future and not according to popular opinion.

From our perspective, iron ore continues to be an attractive prospect considering its favourable price and substantial volume. If the current volume keeps increasing, the unit cost could potentially dip below $20. Furthermore, when factoring in the Australian Dollar (AUD) sale cost, it logically provides a 22% higher profit margin.

As for graphite and rare earth, we have reservations due to:

A high level of uncertainty regarding their production and market control.

Limited profit margins.

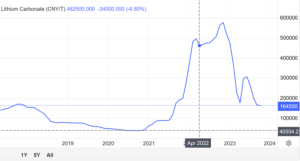

Regarding lithium, we are cautious due to its price volatility, which presents a higher risk to our risk management. In fact, we believe that the current price of lithium is still overvalued after the recent “tulip mania” event, similar to the situation with copper after the technology boom in the year 2000, and it may take a few more years to normalize.

We are still navigating a very complex yield curve dynamic and its associated liquidity challenges. However, as indicated in a previous article, we would like to concentrate on the short-term US10Y. Our position in commodities is also influenced by our suspicion that there will be a continuing imminent shift in $TNX, backed by the just recent more stability of $TLT.

What do we think will happen IF the U.S. and China had real issues in the past and are now genuinely moving towards better economic cooperation? Would there be better resolution of US liquidity? Would there be increased of commodity consumption? Would there be higher consumer price? We leave that up to each individual’s superpower skill, imagination, and portfolio strategy.

The outcome of a global economic war is not a measure of which side was morally or ethically justified in their cause. Instead, it emphasizes that the side with superior resources, and strategic advantage often emerges as the victor, rather than the righteousness of a particular cause. Furthermore, the phrase highlights the tragic and devastating toll that war takes on both sides, leading to high inflation, high mortgage rate, costly living cost, volatility and investment loss. Overall, this saying underscores the futility of resolving complex economy issues and encourages the pursuit of alternative means, such as diplomacy and dialogue, to achieve lasting and just solutions.

Please note that all ideas expressed in this blog and website are solely my personal opinions and should not be considered as financial advice.

“When the fierce, burning winds blow over our lives-and we cannot prevent them-let us, too, accept the inevitable. And then get busy and pick up the pieces.”

Dale Carnegie – Stop Worrying and Start Living.

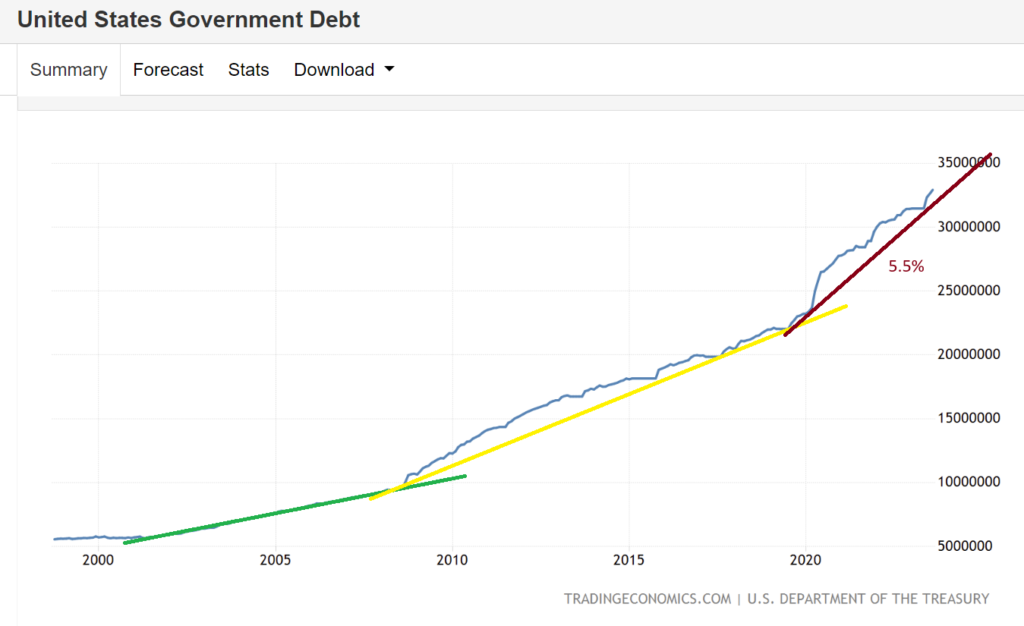

In my previous articles, I have argued that current economic systems should accommodate a 5.5% growth. This is a straightforward concept, and I would employ 5.5% as the fundamental standard throughout my entire thesis. Since 2020, the US debt has been consistently increasing at the same rate of 5.5%. I anticipate this trend to continue until next few years, at which point after, it may accelerate even further faster. Unless the largest economy in the US experiences a significant deviation from its trends spanning decades, we should acknowledge my inevitable economic thesis: (1) higher debt (2) faster debt, coined as “higher further faster.”

The current pace of growth has exceeded that of the previous cycle and is anticipated to rise further in the subsequent cycle (after the next Global Financial Crisis). During this period, the global landscape has been notably demanding due to elevated levels of debt growth. The earlier 2020 CoVID crisis necessitated low interest rates and fiscal support measures to steer it back onto its 5.5% trajectory. I would anticipate policymakers to maintain their commitment to this debt-driven growth. Ultimately, they would have little choice but to align with this trend, lest they risk jeopardizing the entire economic framework, which amounts to hundreds of trillions in human history.

In prior articles, I contended that a 5.5% increase in debt might lead to significant economic challenges:

Firstly, a 5.5% increase in debt will drive asset growth at a rate of at least 5.5%. This will lead to a swifter expansion of assets in the market and among participants. We can anticipate the following:

Wealthy individuals with significant assets will experience even greater wealth accumulation.

Major corporations will demonstrate resilience, maintaining stable revenues and continued hiring.

Secondly, historically, wage growth has not exceeded 5.5%. This could pose a challenge as most workers may struggle to keep pace with inflation.

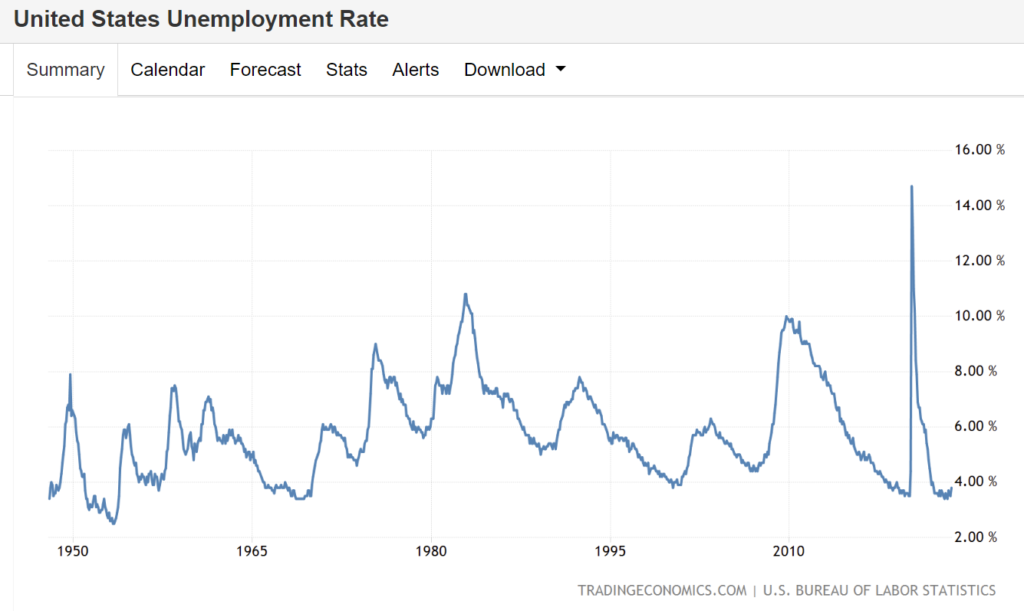

Thirdly, individuals fortunate enough to possess substantial and rapidly appreciating assets may face a decision between continuing employment or opting for retirement. I suspect this may be a minor contributor to the lower unemployment rate, owing to workers choosing earlier retirement. Over time, they are likely to receive enduring support with returns sustaining at 5.5%.

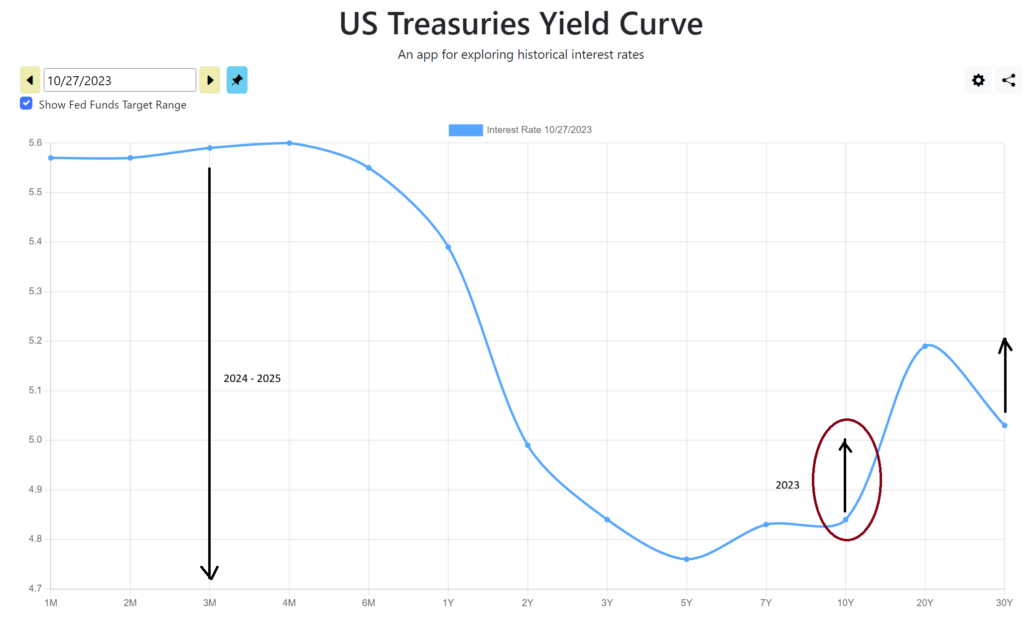

Lastly, there should be an adjustment in yields. Assuming policymakers remain steadfast, I would contend that long-term yields should at least approach 5.5%.

We are witnessing evidence supporting my fourth argument here. Over the past few weeks, we have observed disruptions in both $TLT and $TNX. I stand by my thesis that they should reach a minimum of 5.5%, and possibly even higher on the longer end. While some economists have been suggesting that TLT may have hit its bottom in the past few weeks, I would argue that it has not yet done so. The 10-year yield has not yet reached 5.5%. I firmly believe that the 10-year yield is strongly linked with inflation. Therefore, given that the 10-year yield has surpassed its previous high of 4.2%, we should anticipate:

A prevailing narrative of heightened inflation.

A new normal of 5.5%.

I suspect that this shift in narrative, which has taken us halfway through the cycle, where we’re beginning to see a rise in both inflation and yield, has contributed to the recent bout of volatility. From my perspective, policymakers are standing firm in their commitment to achieve a 5.5% growth through a combination of deficit spending and monetary measures. It’s worth noting that not all economists endorse these policies, with some deeming them as risky due to their potential to excessively stimulate the near term, possibly jeopardizing the long term.

I contend that the world has entered a new paradigm, and in my view, 5.5% represents a new normal. Market participants should be prepared to embrace this change and acknowledge its inevitability.

However, it’s important to recognize that this acceptance is not without repercussions, as elucidated in my second and third arguments. While major corporations continue to generate substantial profits, the same cannot be said for smaller enterprises and the average individual. Unless wage growth experiences a substantial acceleration, we may continue to face challenges in the market. We must closely monitor whether individuals can sustain their spending, if major company revenues will continue to surge, or essentially, if key economic indicators will remain robust.

I understand that some advocate for a focus on the average economy. Yet, in my perspective, policy tends to lean towards the larger economic landscape rather than the average. If these significant economic indicators were to falter — for instance, if major corporations were to significantly reduce employment — the new ecosystems might face difficulties. However, as we have observed, the major economic metrics remain solid. Therefore, in my view, policymakers will stay the course, using front-end deficit measures.

Given the stability in economic metrics, I don’t see any reason for policymakers to alter their approach until long-term yields reach a 5.5% growth (which has not yet been achieved). I believe they will remain steadfast in their strategy and avoid making significant disruptions to the long term until this 5.5% objective is met.

I maintain my thesis that a 5.5% front-end Fed rate represents the peak or upper limit for the Fed rate. As of August 2023, this remains my peak rate thesis. My argument is straightforward and is rooted in the observed debt growth. Raising the rate beyond 5.5% would likely lead to a stagnation in the economy and a contraction in liquidity, thereby tightening the market. Conversely, reducing the rate below 5.5% would likely only spur inflation, which has been trending upwards over the past half of the cycle. The longer policymakers adhere to a 5.5% rate in the front end, through the use of fiscal deficit, the more entrenched it will become in the long end.

There is a discussion surrounding the potential limitations of fiscal deficit supply. If over the next 4-5 years we do not observe any improvement in market resilience, we may unfortunately face a significant new challenge where increasing long-term yields could escalate beyond control. My contention is that supply allocation should no longer disproportionately favor short durations and must begin to exert pressure on longer durations. In this scenario, Treasury buybacks (which would be implemented gradually starting in 2024) could emerge as a dominant policy to prevent an uncontrolled surge in long-term yields, which the global economy may not be able to sustain. We’ll deal with this later.

To avert such a situation, as I argued in my articles over the past two months, cooperation with other countries, particularly China, should improve. I still believe that China has not yet substantially reduced its holdings of US Treasuries. There will be debates regarding duration and potential reallocation, possibly involving Europe.

In contrast to some other economists who may anticipate a cooling down of inflation, I adhere to my thesis that we will start to witness a resurgence of inflation, and it will likely persist at elevated levels. This is why I have begun to reacquire quite significant amount of leveraged commodities. In the next few years, I anticipate a potential (restrictive) cycle in commodity growth. I cannot predict whether there will be a definite recession next year. We should closely monitor the global market’s resilience during this period.

Given the considerations above, and in light of the increased yields’ impact on resilience, we have decided to re-enter the market, albeit without employing much leverage. In previous years, we consistently maintained leverage ranging from 200% to 300%. However, for this half of the cycle, we are beginning to allocate a portion of our previous leverage into fixed incomes (though not yet long-term bonds), and we have not yet introduced significant leverage. If long-term yields were to surge above the 5.5% trend, I may then reallocate fixed incomes into long-term bonds. I believe it is a prudent decision to introduce fixed income into my portfolio, which has primarily consisted of high-risk assets with high leverage in the past 3-4 years, lacking lower-risk assets.

Please note that all ideas expressed in this blog and website are solely my personal opinions and should not be considered as financial advice.