In March 2024, as mentioned in the previous article, I closed my eyes and could see the kind of world that was waiting up for me. Through the dark, through the door, through where no one’s been before, but it feels like Déjà vu / home.

In 2006-2008, commodities rallied like, God, it was Crazy.

I bet all-in super high leverage in them

I lost all due to 2008 Commodity GFC

Just because of thing like the Lehman Brothers ninja

For a HUGE 100 B$

Sixteen years later, the lost-all experience and that “100 B$ Puny God commodity rally” (compared to the world we see today) is still so vivid to me.

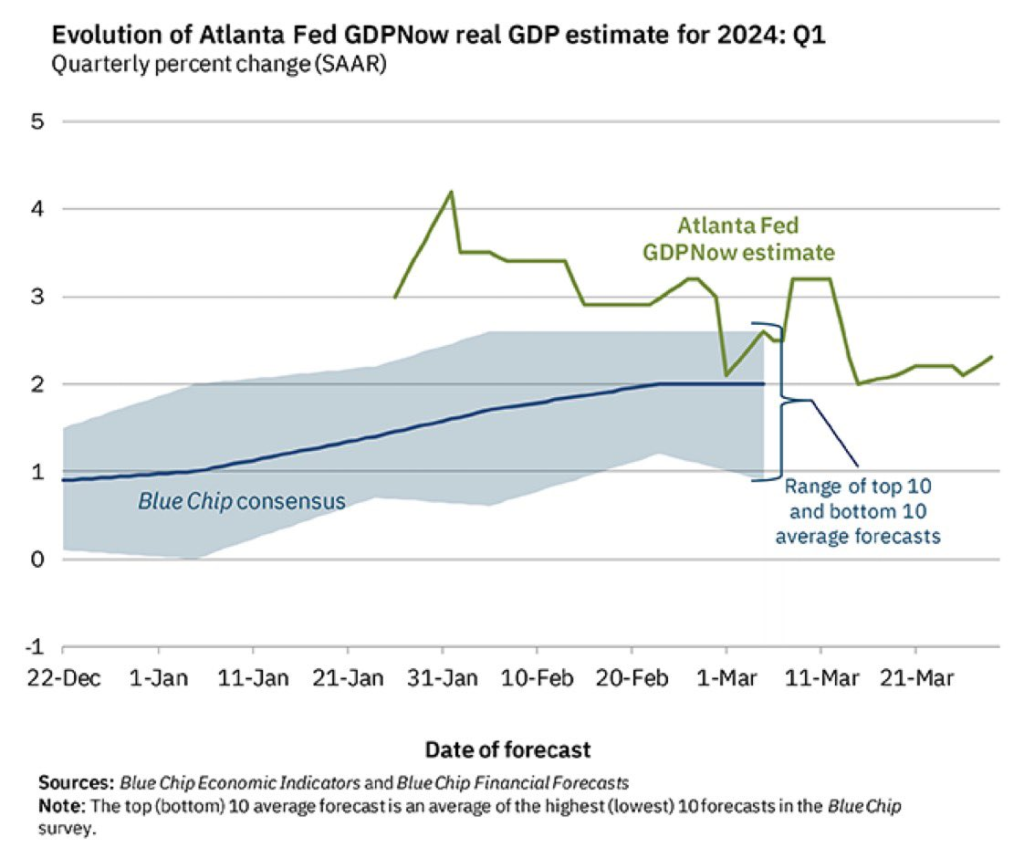

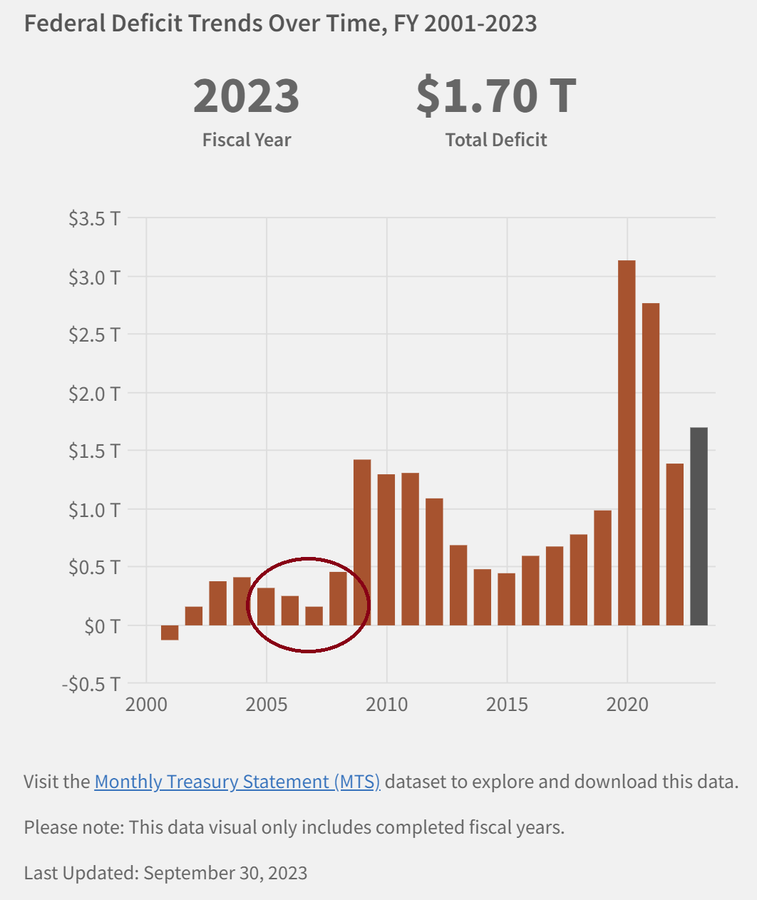

US fiscal deficit: 8-18x ?

A decade of NIRP, never seen before.

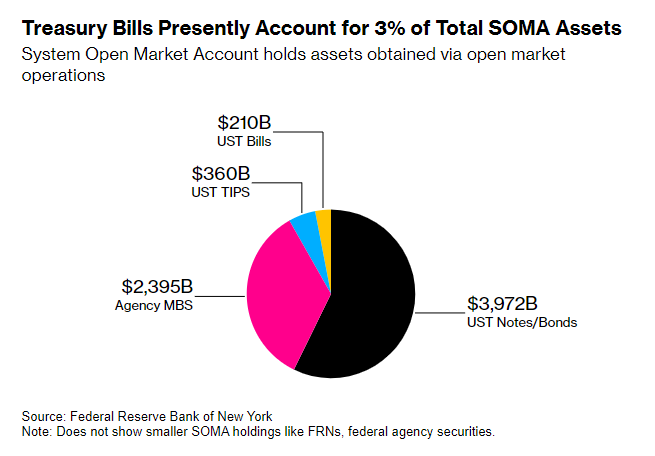

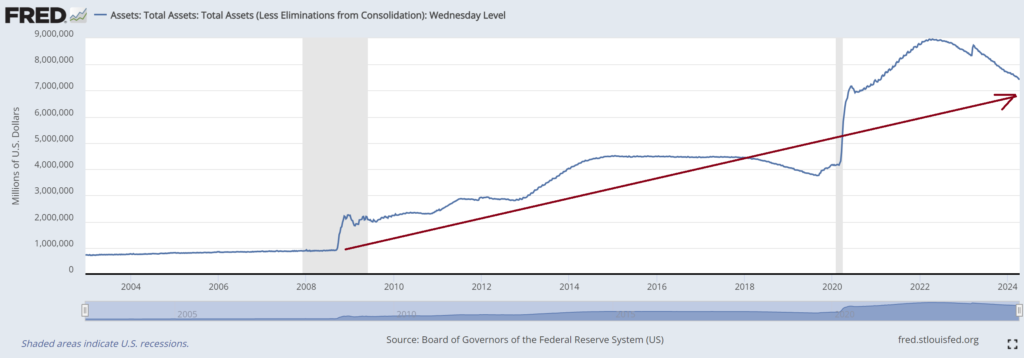

Balance Sheet: 7x ?

As explained in the previous article, why is the following happening? Unfair, but fair enough for many reasons.

Since mid of March obvious-for-me Bonds sign, I have predicted the emergence of numerous superheroes on this planet and others, coming to save the Wall Street world, both masked and unmasked. However, please don’t tell me that this world can be saved by mere talk. I don’t believe in fairy tales like Cinderella. My experiences have shaped me.

♬ They can say, they can say it all sounds crazy (my dream, my thesis and my execution)

They can say, they can say I’ve lost my mind

I don’t care, I don’t care, so call me crazy.

We can live in a world that we design ♬

Why I’m so infuriated with my dream? As my January thesis, the Fed might not be able to start cutting before ending their long end balance sheet reduction. In my thesis that time, early rate cut sounds illogical. It’s more logical not to cut rates, as it obviously makes more sense given that global expansion is occurring, and to maintain long-end broken mandates, credibility and individual powerful supremacies. Unfortunately, this dream can only survive as long as the supremacy tells so.

♬ ‘Cause every night I lie in bed

The brightest colours fill my head

A millions dream is keeping me awake

I think of what the world could be

A vision of the one I see

A millions dream is all it’s gonna take

Oh a millions dream for the world we’re gonna make ♬

But hey, everyone is entitled to their own dreams, theories, and can do whatever they want with their money or portfolio. You may be right, I may be wrong. I’ll just close my eyes to see the world I see.

♬ However big, however small

Let me be part of it all

I share my dreams with you

You may be right, I may be wrong

But say that you’ll bring me along

To the world I see

To the world I close my eyes to see

I close my eyes to see ♬

Please note that all ideas expressed in this blog and website are solely my personal opinions and should never be considered as financial advice.