Based on an unbelievable true story, America achieves remarkable economic growth during a period of global tightening of the US dollar. This favourable situation/story should be safeguarded at any expense, while also ensuring a smooth landing for intelligent financial investments.

We have welcomed over 80% of fund allocation to America since the beginning of the year, based on our thesis. Our belief was that America would achieve exceptional success with a peak in interest rates, causing global currency to tighten and creating a strong demand for USD to fuel economic growth. This thesis is based one of our foundational money principles.

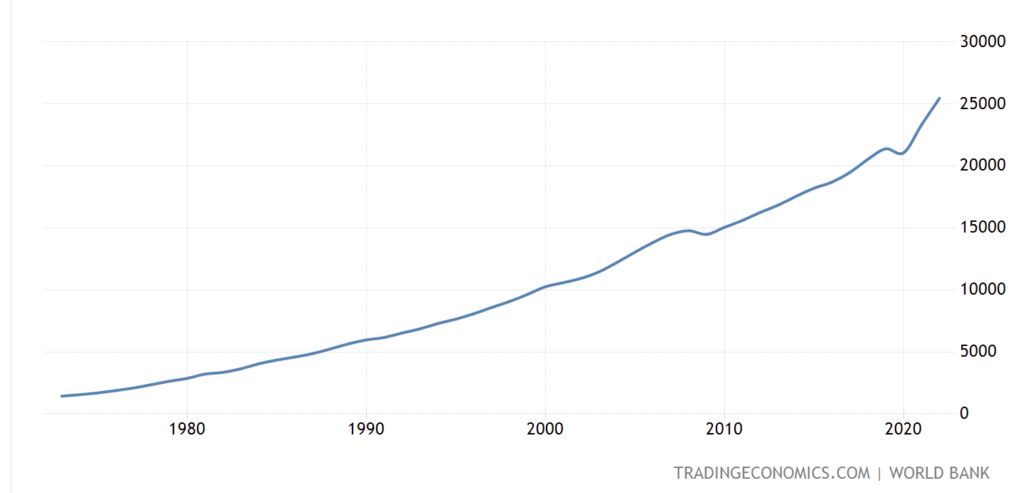

Firstly, let’s examine the growth of GDP. The US GDP is currently expanding at an unprecedented rate. According to our theory, this is a highly valuable asset that must be safeguarded at any expense, disregarding any other conflicting economic indicators. This is especially crucial considering the presence of smart money that has become trapped within the US economy, which we will discuss further later on.

It is not surprising that over the past few decades, the US had experienced a shift from a predominantly industrial and manufacturing-based economy to one focused on services and finance, with a significant portion of manufacturing activities being outsourced to China. However, since 2022, there has been a substantial resurgence in manufacturing and industrial activity, particularly in sectors related to sustainable energy and artificial intelligence, such as electric vehicle (EV) manufacturing, EV infrastructure development, battery production, and computing chips. These industries have received substantial support from the US government and are showing strong growth, which should be sustained and protected at all costs.

As we have previously highlighted in our articles, these sectors have the potential to generate a new economic capacity exceeding 10 trillion US dollars.

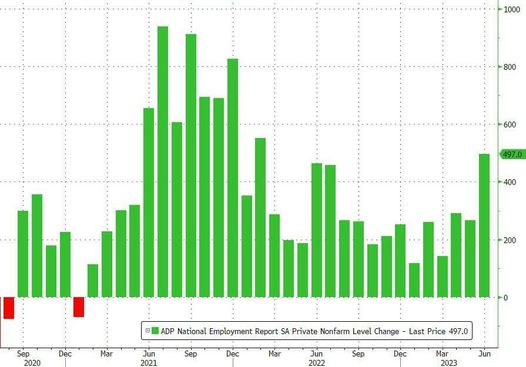

While the manufacturing and industrial sectors may not directly lead to job growth, the substantial government support they receive, particularly in terms of financial investments, has had a positive impact on job openings in other sectors. This support has helped boost employment opportunities in industries such as hospitality, finance, and services.

To ensure sufficient liquidity for economic growth in an era of low new bank loans due to high interest rates, the main source of liquidity is currently the fiscal deficit, which has reached 1 trillion dollars per year. This is one of the main reasons why we significantly increased our investment in the big QQQ portfolio by almost 10 times in January. This decision was influenced by the portfolio’s significant cash holdings in the form of treasuries, which provide substantial benefits.

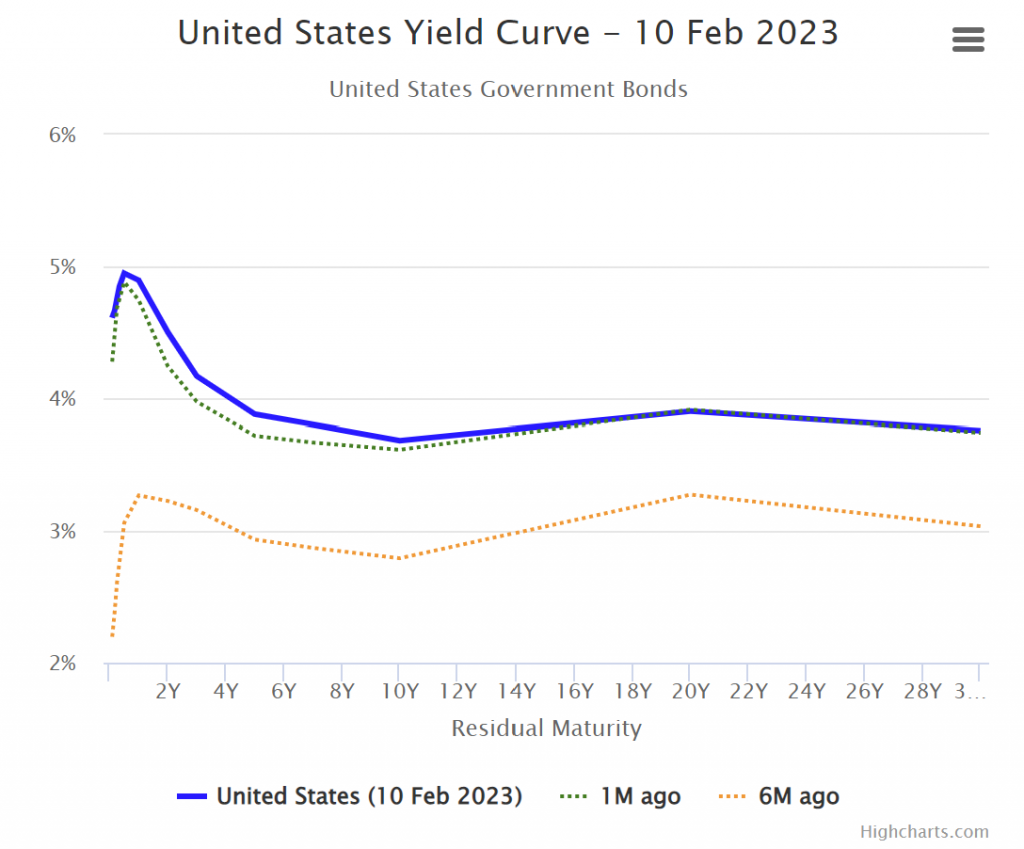

The robust growth of the US economy poses challenges for the rest of the world and its own long-term yields. The US dollar was in short supply until US leaders visited China to negotiate undisclosed additional agreements. As a result, business and mortgage rates are expected to remain elevated for an extended period. While high interest rates can have negative implications for businesses and the economy, as we previously mentioned in our article last month, it can be seen as a positive factor. The scarcity of global funds is preventing excessive concentration in long-term investments such as bonds and instead supporting short-term economic growth. This approach is necessary as allowing money to become too abundant could lead to the resurgence of inflationary pressures.

The “smart money,” represented by the RRP (Reverse Repurchase Agreement) and Bank Reserve, is currently focused on short-duration investments. I suspect that these entities will begin to transition into shorter-term debt, a phenomenon that is currently unfolding. The Treasury General Account (TGA) is essentially funded two-thirds by RRP and one-third by Bank Reserve, with less other sources of funding. This leaves the decision on the duration in the hands of the Treasury. This shift is expected to increase the price of high-risk assets, such as shares and commodities. As the economy approaches its peak growth later in the future, short-term investments are anticipated to benefit the most from anticipating the Federal Reserve’s interest rate changes.

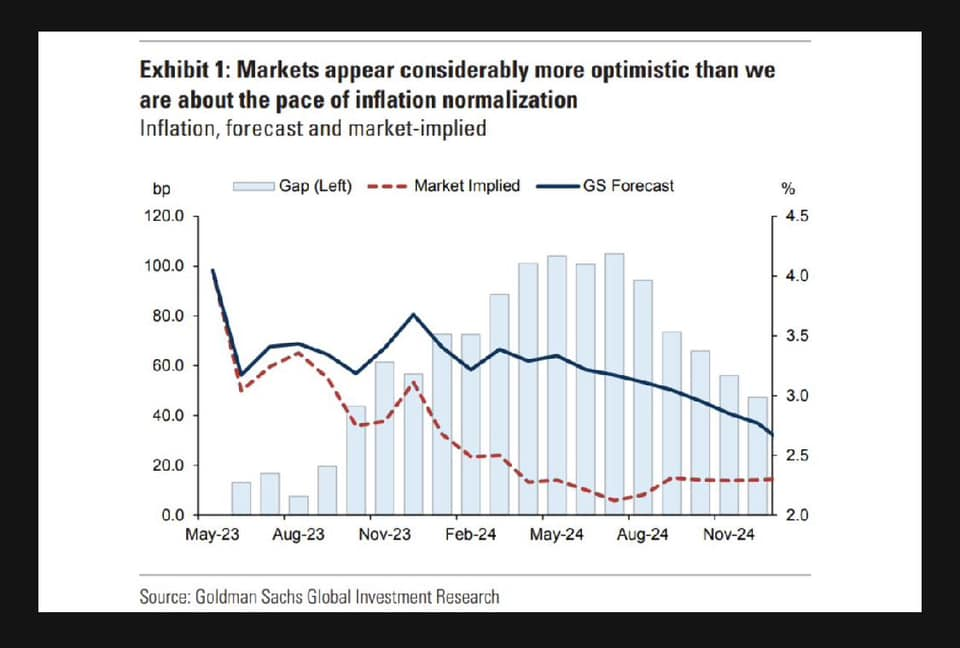

The inflation figures, particularly the Consumer Price Index (CPI) and the Producer Price Index (PPI), have experienced a significant drop. However, this decline is primarily attributed to technical factors. In early 2022, inflation numbers rose significantly due to massive support provided to the economy, as discussed earlier. Given the rapid growth at that time, it became challenging to achieve comparable year-on-year rates, resulting in a narrow window of opportunity to boost the flow of money into the economy. As mentioned previously, it is expected that inflation will remain relatively stable until early 2025. This view is also supported by the increase in the debt ceiling to around $35 trillion until approximately March 2025.

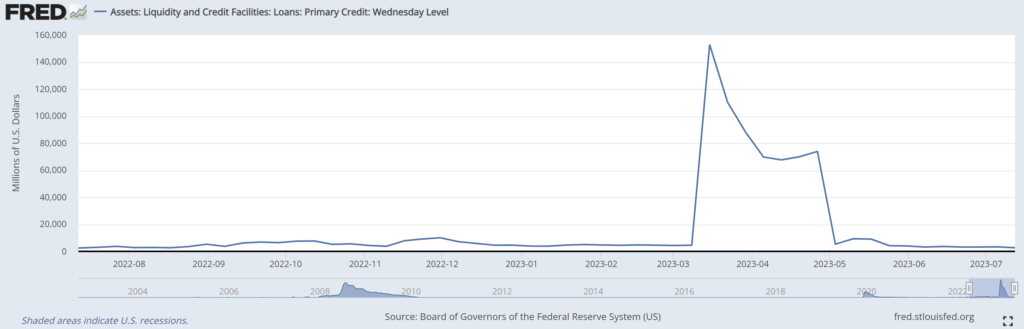

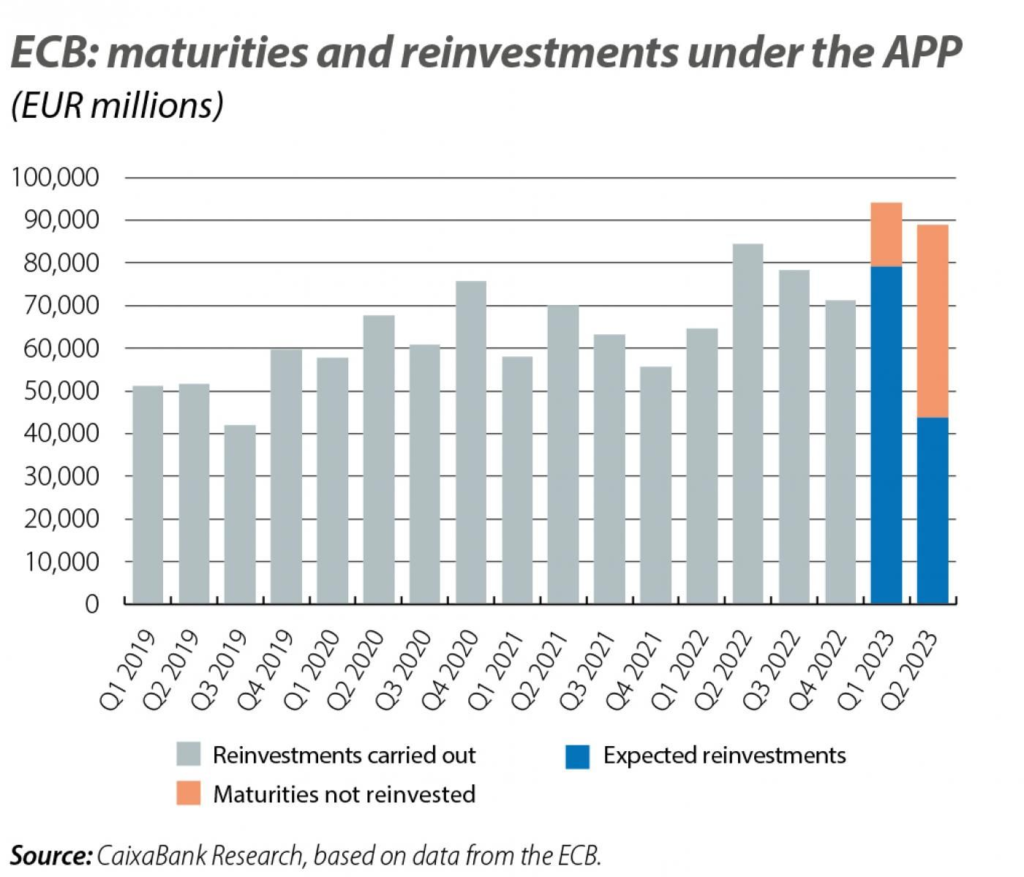

In order to mitigate the risk of uncontrollable inflation, similar to what we have observed in the balance sheet of the European Central Bank (ECB), the Federal Reserve should also indicate a lower balance sheet through the use of QT. However, to avoid the negative effects of reducing the balance sheet, as we discussed in our previous article, I expect Treasury to focus on short-duration investments rather than selling long-duration assets and Federal Reserve to not shuffle around balance sheet duration. Participants should also then support long term recycle into short term. This scenario is supported with fact that higher rate Bank Term Funding Program (BTFP) – collateral being valued at par, unlike Discount Window – collateral being valued at market, is being held up within its capacity to 2T$. It tells importance of credit accessibility and risks for longer durations. Once again, this aligns with our expectation to facilitate the smooth transfer of wealth for the smart money in the future.

Within the limited windows of supportive environments to soft land the economy, we can observe several supportive factors:

Inflation numbers (CPI and PPI) showing a decrease due to technical reasons.

An increase in the debt ceiling/deficit, serving as a means to control the flow of money.

New short duration treasury issuance expectation to counteract the impact of Federal Reserve quantitative tightening (QT).

Strong employment figures – “any sector, regardless of manipulation or guess”.

Strong backbone banking sectors outlook and financial figures – “through possibility of the Fed balance sheet holding and deficit subsidy”.

Less effort for the Federal Reserve to shuffle around balance sheet duration.

Given these circumstances, it is anticipated that Wall Street should continue to experience upward momentum until the completion of these money flows, at least over the next few months. Therefore, based on our risk assessment, we have decided to maintain our double offensive leveraged positions. Please be mindful of the subtle differences in risks and conflicting economic indicators within our approach to my money theory.

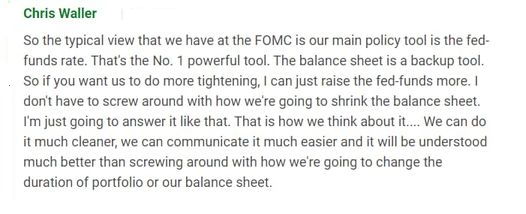

In support of our thesis and interpretation of the current situation, we believe that the comments made by Chris Waller may further reinforce our perspective.

Please note that all ideas expressed in this blog and website are solely my personal opinions and should not be considered as financial advice.

It’s time for us to shift our focus solely to short-term investments and avoid any potential long-term investments. As the sun sets, we’re already ready to reallocate any possible long-term investments to prepare for a long night’s sleep, as thieves are poised to steal everything overnight.

Recession is what gives investment meaning. To know our days are numbered. My investment is now mostly short term or strategic blow off.

Our solid view since early January 2023 has prepared us for this. The peak rate is pricing in starting from this month in March 2023, and money should start to concentrate on short-term investments. As we mentioned in previous articles, we have removed almost all commodity investments since they are most sensitive to long-term investment. Today, we can see that banks are exposing their fragility to medium-term investment as well, due to the same issue. This is a solid confirmation that our current strategies are correct.

Learning from medium term view investment banks:

Banks have categorized their investments into HTM (Hold-To-Maturities) and AFS (Available For Sale).

Most of HTM investments were made when the rate was very low, mostly to toxic MBS securities, resulting in mostly long-term duration while AFS investments are of short-term duration.

The Fed and government have given up their position to help avoid bank runs and more systemic issues. This is very important because market participant number one has disclosed their position.

In reality, this is actually helping AFS (short-term duration) to avoid their fire sale rather than fire-sale of their HTM (long-term duration). Why? Because the HTM price is already so low, and there’s no incentive in the market at the moment to attract their demand during this fully inverted yield.

The troubled banks are actually getting more difficult because they have to continue holding their HTM (1.3%) with the current high rate (4.5%) and continue taking care the loss with new loans. Therefore this Fed injection doesn’t really make the small banks better. They are just getting more loans/liquidity at par value with the current high rate, to keep their HTM until maturity.

This is different from QE in terms of: (1) yield curve (2) actual impact on investment. For (1), in QE, the yield curve is steepening that the Fed could give a lower rate (to zero) to invest in purchased assets. Current inverted yield made it impossible because central banks only have control over short-term rates rather than long-term. For (2), as mentioned above, this injection is more beneficial to short-term AFS to avoid their fire sale rather than selling their long-term HTM.

This situation also has made it even more difficult for banks because the market knows that banks are trying to unload their medium-long-term assets and therefore will not be interested in taking other bank HTM without any deep discount (30-40% loss).

Due to the concentration on short-term investment, we expect there will be an asset misallocation issue (asset blow off). Due to all factors mentioned above, at the end, the only way to solve the issue is to give general recession to the market.

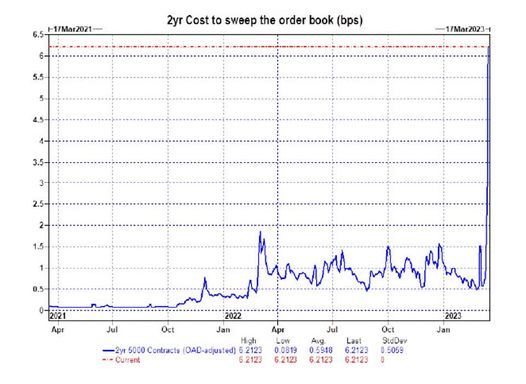

How much does it cost to undo this curse? The 2y cost to sweep has spoken.

Sustainable Energy

Let’s keep our horror story aside and look at the brighter side for a moment. Why was I so excited in early January 2023 with real numbers in AI (Artificial Intelligence) and Sustainable Energy? I would speak about Sustainable Energy economy at this opportunity because their numbers are real important.

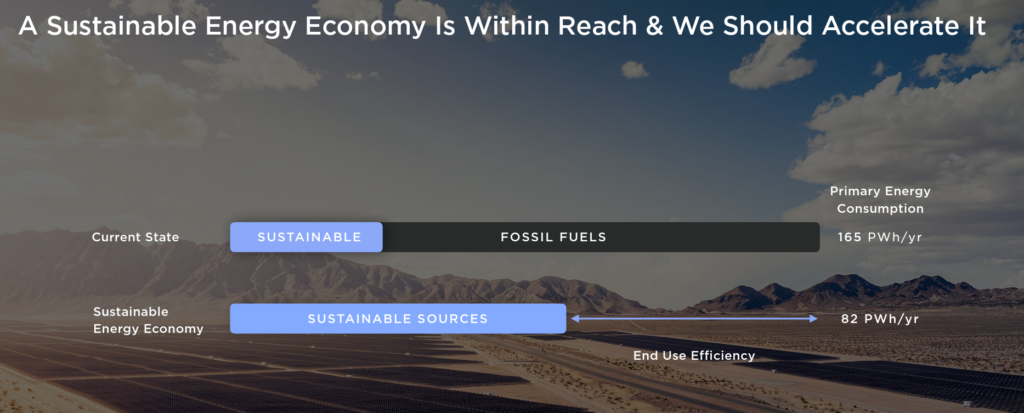

Our energy economy is so wasteful. Two-thirds of the energy generated is wasted.

Sustainable energy economy is still left behind and has a lot of capacity and offers much higher efficiency to eliminate the above waste.

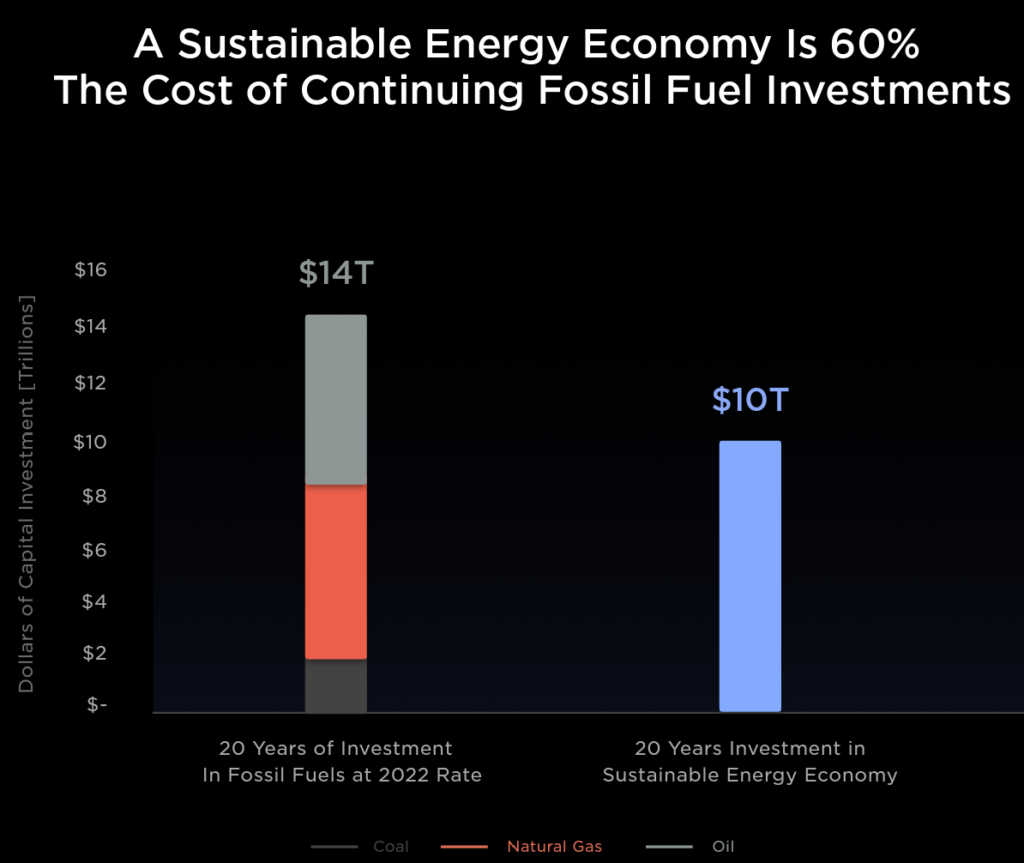

The amount of investment capacity is $10 trillion in 20 years and could immediately give high value.

Ten megawatts are estimated to cost $12.7 million (~65% margin). We would need 240TW. The available economy capacity is 240,000,000 / 10 x 12,000,000 $, and we could only target a small portion of it to fix the current economy issue.

As mentioned previously, our economy has too much short-term liquidity, which has outpaced long-term capacity and return (inflationary). This sustainable economy could actually solve the problem to reallocate this excess into long term investment, but it will require huge amount of money in very short time to incentivize the movement, which could only come from the government and central banks.

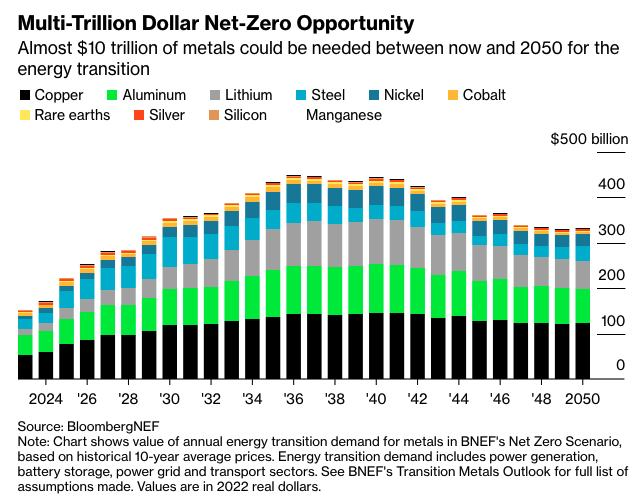

Looking at the commodity side, $10 trillion worth of metals are needed until 2050. Therefore, we will return our 95% commodity reallocation back once dawn has come.

Treasury Bonds

I have overweighted too much on equities since early 2020, no secret due to the massive GFC-Covid recovery. Since then, early 2023, we have reallocated 40-50% of our portfolio in short-term treasury bonds (3-5 years maturity and returning about 5% pa) at their face/par value due to the scary inflation narrative. Luckily, the world is with us, and we saw massive recovery in January 2023. I became more confident and tend to maximize leverage on it. My main reason was to target the next 6-month inflation peak, around June 2023 or so.

Timing Statistics

Below are what I think is very important statistics:

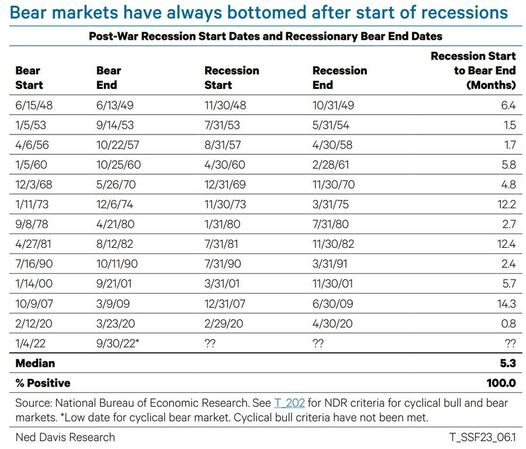

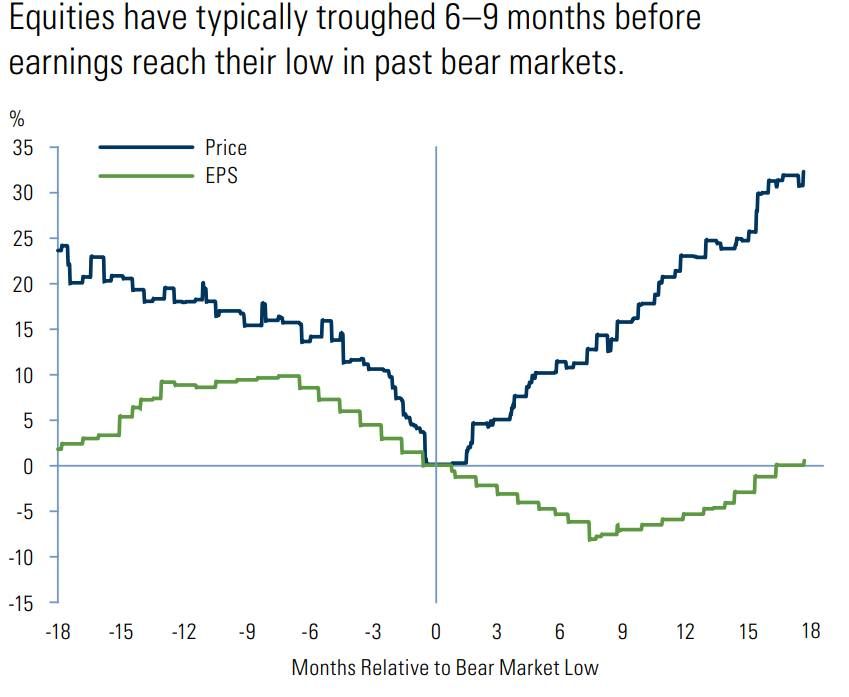

100% probability of bear market to bottom after the start of a recession.

Bear market to bottom about 5.3 months after recession start.

81.3% probability bear market ends about 13.6 months after the last rate hike.

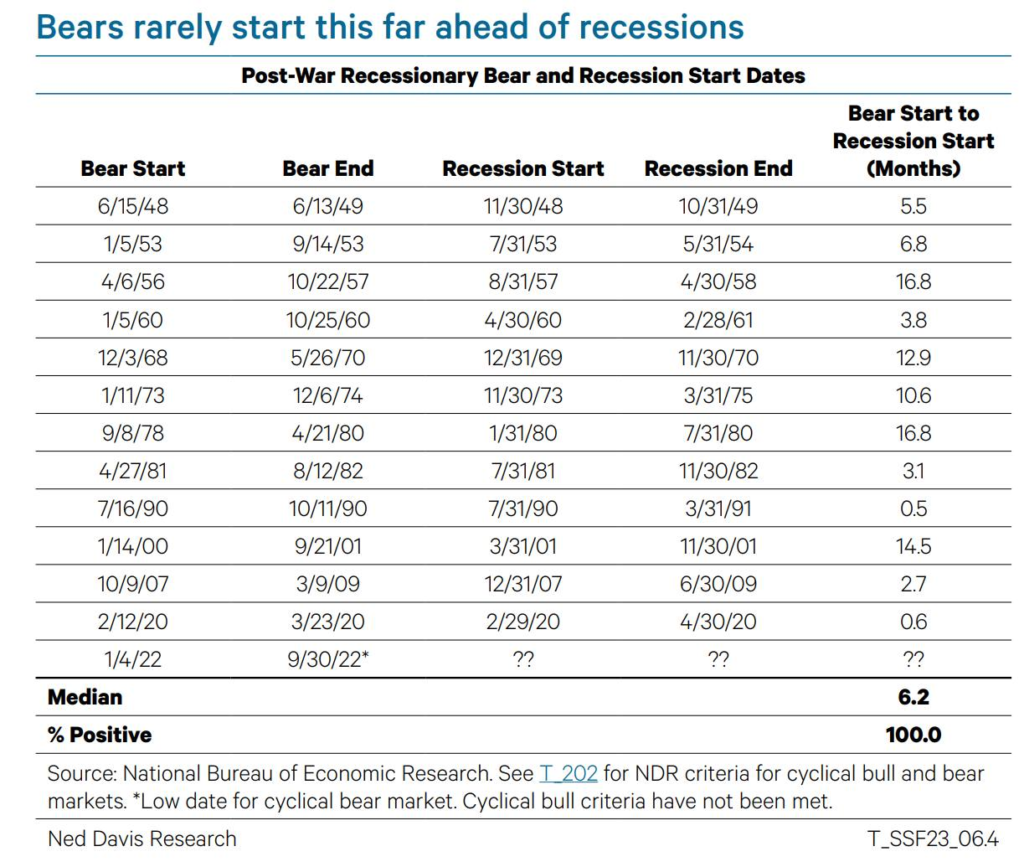

100% probability bear market to recession start at about 6.2 months.

Therefore, based on these statistics, probability-wise (60-80% probability):

If the last rate hike is in Feb 2023, the bear market tends to end in April 2024.

The recession will start about 5.3 months before April 2024 = Oct 2023.

The bear market will start about 6 months before Oct 2023 = May 2023.

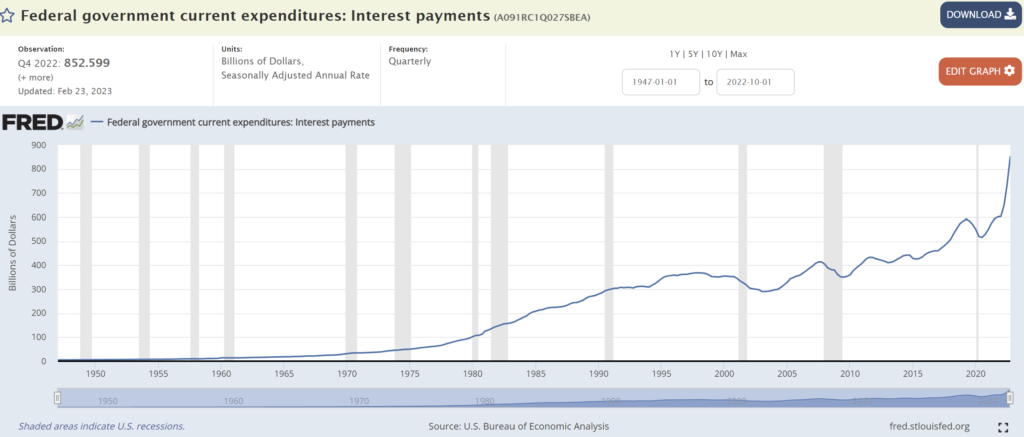

It’s my view that the market is supported by money, either from the central bank or fiscal and nothing else. While the Fed is only able to reduce $600 billion of balance sheet, it’s interest payment from fiscal about $900 billion that keeps this market floating.

It’s then the market decides how far interest rates can go up. The issue that I see here is that even though economists say the Fed is reducing the balance sheet too slowly, it’s my view that the Fed is actually selling the balance sheet faster than the market can afford. The Fed has really tried hard to reduce inflation, not through the use of higher interest but the use of more balance sheet QT.

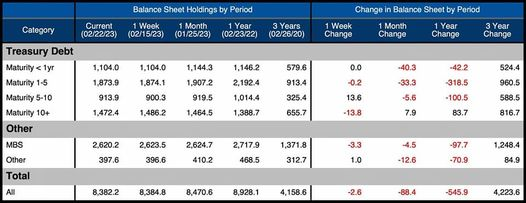

This is where I have to look into Fed balance sheet selling:

The Fed couldn’t sell the MBS (Mortgage Backed Securities) because it’s toxic debt with a very low rate, around 1.3% pa.

The Fed balance sheet reduction is highly concentrated in the short term.

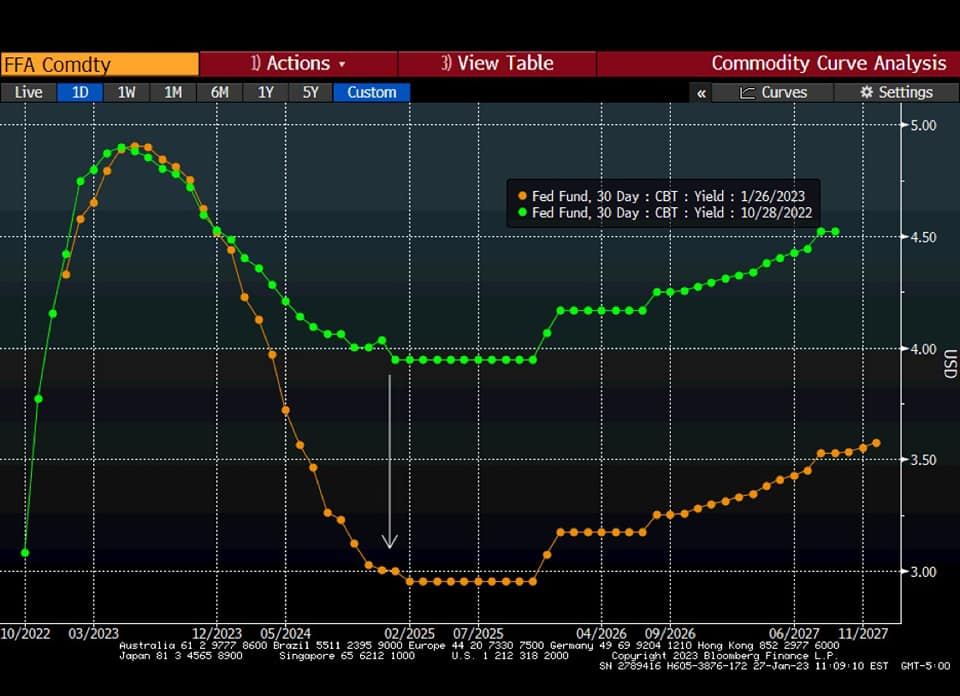

The concentration of the Fed’s selling is actually between 1 to 5 years of maturity. Please remember my old theory that central banks always transfer wealth to their 8 big banks through front running, using any event of QE (Quantitative Easing) or OT (Operation Twist). I expect a similar case to occur here.

I may estimate that this biggest belly will expire around the end of 2024.

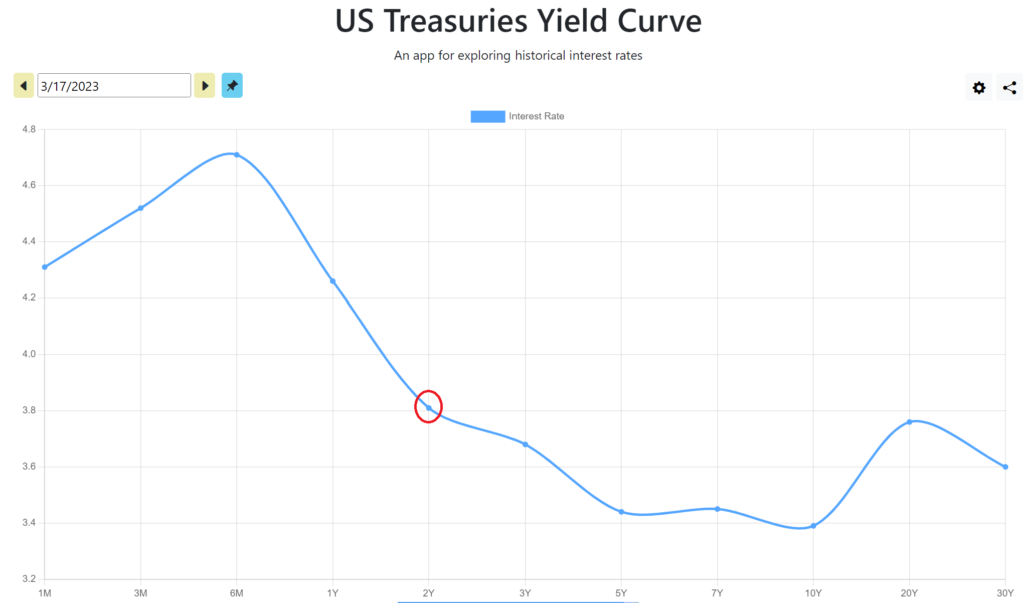

The current 5-year rate yield is about 3.5% pa.

This seems to support our previous conclusions:

We may have a lot of maturity around the end of 2024.

Six months leading to it is when the recession will end, ~ April 2024.

It means there will be less money injection towards April 2024, which could probably start from the recession in October 2023.

The Fed is going to keep interest rates high and could probably overdo it by May 2023.

We can see that the Mortgage-Backed Securities (MBS) have caused trouble not only for the Federal Reserve but also for small banks like SVIB.

JPMorgan estimated that the Fed will require around $2 trillion to combat this effect, which could increase the current debt from $8 trillion to $10 trillion. Historically, the market crashes once the Fed’s balance sheet grows near the previous high (9T$). If the market is unable to absorb more than $1.7 trillion from the $2 trillion to normalize the long maturity issue, with its interest being only $100 billion per annum, I would expect severe market pressure. This is another reason why I see at least a disinflation, and its risk is a very severe impact on commodities since commodities are high-risk assets. If the Fed reduces rates, it would only hasten the crash because the interest payment is going down massively while the market still needs to absorb a high amount of long maturity loss.

So where does the money go? In my opinion, the money will eventually go into Treasury bills with lower maturity, 1-5 years. This is why I have massively bet on Treasury bonds with maturities of 1-4 years with maximum leverage at the beginning of 2023. If the question is whether I am worried about the possibility of additional $2 trillion supply of low maturity debt, I am not. It’s because it’s only 6% of the total US debt and we have RRP+reserve. Eventually, when the market stalls, the quickest way to save financial systems is by cutting the rate, which will eventually expand the central bank quicker and hasten the market crash. During an event where the central bank cuts rates, I estimate that they will make massive purchases of our short-term duration, because the yield curve has been severely inverted.

The sunset can be a scary moment when you realize that your days are numbered and there is probably no escape.

Please always remember that any ideas on this blog and website are my own personal opinions and are not financial advice.

I was busy overhauling my investment strategy in early January 2023 to ensure it aligns with reality. In just two weeks, I increased my investment allocation into the major sustainable energy + minor electric vehicle (EV) and artificial intelligence (AI) space from 5% to 45%, a nine-fold increase.

Here are my points:

Set your sights high, but be prepared for the risks of disappointment. Don’t limit your dreams.

Everyone has their own imagination, and no one has the right to interfere with it.

If your dreams don’t become a reality right away, keep striving. Remember, Rome wasn’t built in a day.

Hold your breath Make a wish Count to three

Come with me and you’ll be In my world of pure imagination Take a look and you’ll see Into my imagination

The world can be cruel and intimidating, preventing us from having bigger imaginations. I believe that imagination and its realization is a fundamental human right. Everyone should have the opportunity to pursue their greatest aspirations and turn their big dreams into reality. Don’t limit yourself by starting with small dreams. Instead, dream as big as you can afford their risk of disappointment.

My imagination begins

… We’ll begin with a spin Traveling in the world of my creation What we’ll see will defy Explanation

I believe in the creation of new value and wealth through evolution. When something evolves successfully, new forms of valuation and wealth creation are born, such as the oil boom, information technology boom, derivative boom, debt boom, currency boom, and more. This is why I am excited about my vision for the future of Artificial Intelligence and Sustainable Energy.

I try to invest wisely rather than impulsively. In December 2021, I sold all my investments because they contradicted my investment principles, mainly with regards to my yield and inflation expectations, which surprisingly came as expected.

The Nasdaq fell throughout the year of 2022 due to expectations of higher yields (6 months leading).

Inflation increased rapidly throughout 2022.

The Federal Reserve raised interest rates at the fastest pace in history, leading to a drop in risk assets.

My vision of 2022 in one image @ December 2021

As I wrote earlier in the year, I was disappointed with the yield expectations and progress of sustainable energy. They were heavily corrupted, with many ESG funds becoming involved in fraud, and early commercial cycles of AI failing to deliver as expected. I would like to see the glimmer of commercial value before I invest heavily. However, I still believe that the visions for AI and sustainable energy are pure, real, and true. The issue was not with the concepts themselves, but rather with the people and the yields who attempted to exploit them.

This year, since my future yield expectations have changed, I repurchased all my investments, some at a multiple amount and much lower price. However, this doesn’t necessarily mean that I think they will skyrocket in the near future. My investment philosophy still anticipates high yields and high inflation to persist, but the current situation is different than before.

My expectation is for a sticky inflation target of 3%-4% in the next 12-18 months. This should lead to the most optimal GDP and equity growth, as long as it is well supported, until GDP and equity become significantly overvalued.

Inflation is expected to remain high, around 3-4%, over the next 12-18 months. This level of inflation will be sustained primarily by fiscal ease.

An inflation rate of 3-4%, higher than the Federal Reserve’s 2% target, is likely to result in the most optimal GDP growth.

Inflation rates below 2% may lead to unnecessary disinflation risks.

Inflation rates above 5% or below 1% may result in much higher financial risks.

In simple terms, keeping inflation at 3-4% (a relatively high rate) can lead to the most optimal GDP growth. At some point, when GDP growth reaches its maximum output, I believe that the Federal Reserve and Fiscal will halt this engine, causing inflation to immediately fall back to 2%. We can expect this landing to be an unpleasant experience. However, for now, my focus is on opportunities for high GDP growth or high equity returns.

Imagination is becoming reality

… If you want to view paradise Simply look around and view it Anything you want to, do it Want to change the world? There’s nothing to it

In the past, people used to say that it was impossible to drive a battery-powered car, a self-driving car, or a car powered by solar energy, or to become wealthy, for example. Such judgments were like social bullying. But sorry folks, these things are becoming a reality.

Take a look at Dall-E, for example. Many people have misunderstood AI. Images created by AI are not just sourced from an image database or manipulated from existing images. They are generated from a latent space, in real time. The images created by AI have never existed before. We simply need to describe our imagination in human language, such as English, and the AI will bring it to life. The more precise the description, the better the images will match our imagination. They have already made 2D and 3D images a reality. I have no doubt that they could create a movie from a script. After all, a movie is just a series of 2D images. In the future, I believe that AI will be able to turn any book into an attractive movie.

Twenty-five years ago, I worked as a brand manager. It would take us weeks to create a compelling marketing message, and months to produce a full TV advertisement. Advertising and marketing is a multi-billion dollar industry, as evidenced by companies like Google. AI has the potential to help us craft the most compelling advertisement message or image based on brand management imagination and consumer statistics. This would save millions of dollars and reduce months of work into just hours, allowing for faster decision making.

However, there may be some loss in translation in the communication between humans and AI using the English language. In the future, direct communication between the brain and AI, such as through Neuralink, may eliminate this miscommunication issue. This could lead to the development of a new universal human brain language that could enable communication of any human language with AI language without any miscommunication.

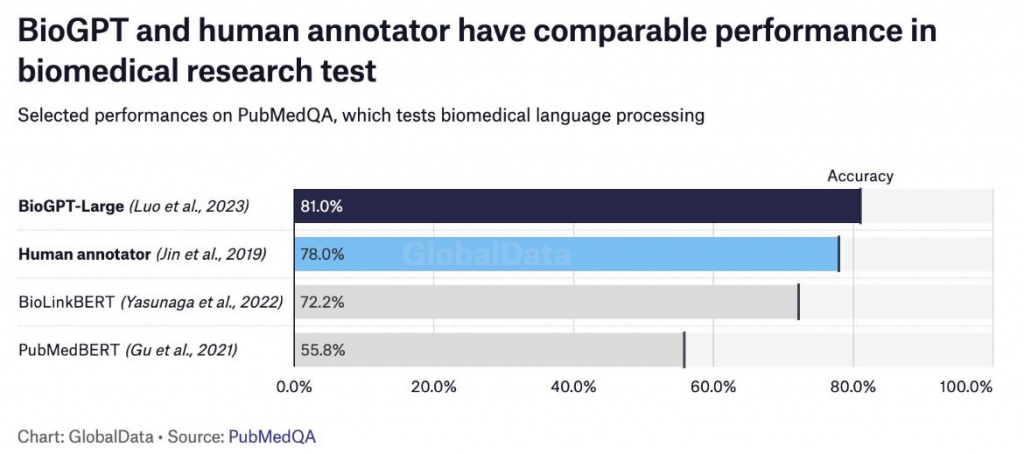

How about BioGPT? It could speed up biomedical research from years to just hours. GPT will continue to discover any other industry. They could store any knowledge library and use them to speed up discovery beyond superhuman with limitless nodes.

Rome wasn’t built in a day

Let’s step back from the euphoria and understand that AI is not a new concept. It has been around for decades. Twenty-five years ago, I wrote my bachelor’s degree thesis using a simple trained array of noise canceling. This array was able to adaptively learn and recognize frequencies in the domain. I was challenged to run a primitive AI on an old Intel 386 using Assembly language, but it worked. It worked so well that it was able to reduce noise up to 40 dBs, which was above 90% of simple noise. Of course, today, learning arrays are getting bigger and bigger. As a result, we can train these brain cells like our own brain. For example, in our brain, we don’t have millions of chicken images, but we can imagine millions of different chicken images with additional details. This is the same with AI learning. They don’t memorize exact images, but they learn what the image looks like and then draw based on our instruction or imagination.

I also believe that inflation will remain high. High inflation and high yield will limit the speed at which our investments will return. If these conditions do not materialize soon, we should continue to strive towards our goals. Rome was not built in a day. If they suddenly materialize and lead to euphoria in the market, we should remember that Rome was not built in a day and be prepared to sell our investments. There may only be two high-probability options: lower return or a boom followed by a bust. I am leaning towards the latter, where we may experience the highest boom and the worst bust within a period of 12-18 months.

Vision Driving AI

This has always been my belief: that vision-based AI could help humans immediately. Don’t confuse it with many autonomous driving systems, as they are NOT vision-based AI. Only vision-based AI is able to handle many different conditions, just like our eyes and brains can. It could immediately reduce human errors in driving and help optimize productivity. While it may still be far away in the future, perhaps 5-10 years or so, to have it running perfectly, I believe that making early investment in it could benefit my portfolio with a fast return. While this AI kid is improving its image labeling, let’s keep it in “deferred”.

Sustainable energy

Given that inflation is consuming most of our savings these days, we should focus on the biggest consumer of it, which is energy. Last year, we talked about the housing component and decided to reduce our property investments by 1/3 due to our belief that inflation and interest rates will remain high. Over a long period of time, high interest rates with no asset price increase will significantly devalue property investments, especially for those with high loan-to-value ratios (LVRs), such as principal place of residence (PPOR), where tax benefits don’t contribute to their downfall. Thus, I believe that in order to protect society from energy inflation, sustainable energy would benefit them.

When a coal-generated electricity plant produces a certain amount of energy, but only 50% of it is consumed by manufacturing and households, the plant must either waste the excess or reduce its output. This is where battery-powered electricity storage comes in. Batteries are now capable of servicing entire cities and factories, ensuring less waste of electricity generation and a higher level of uninterrupted availability. Moreover, households are now able to generate electricity from solar power and sell their excess electricity to the grid at the best time when electricity rates are highest. We have seen homes and universities become sustainable in terms of electricity consumption and even generate extra income. With the evolution of battery technology and sustainable energy, it is all becoming a reality.

What is the catch?

There are two potential issues to consider in my opinion: (1) the possibility of sticky high inflation and high interest rates, and (2) the cost of materials such as lithium, which could limit the evolution of battery technology. While there are significant efforts underway to increase the supply of lithium, it may still be some time before our thesis is fully realized. ARK has predicted that lithium prices may decrease by as much as 37% as supplies increase. Ultimately, the boom-and-bust demand cycle will likely provide enough materials for our imaginations to become reality. Similarly, yields may also decrease over time, with or without a market crash.

My imagination of Disinflation

It’s no secret that we will experience the most challenging time in our investment lives starting in the second half of the year. In my opinion, the market should start pricing in this event from today. This was due to central banks’ late response to combat inflation. To avoid structural damage to the economy in the long term, they had to raise interest rates at the fastest rate in history. As a result, the current short-term high interest rate is too high, making long-term investments almost nonsensical. If the question is whether there will be many bankruptcies, it’s because this event has not yet inverted the 10-year to 30-year yield curve. This means that companies and mortgage holders are still holding and expecting lower rates soon.

In our thesis, business operations and investments should not be expected to afford a 5% base rate in 5 or 10 years. Most mortgage holders will not be able to afford 5% in 5 years, no business operation will be able to pay 5% in 10 years, and not many investments are returning better than 5%. Eventually, one day inflation will give up, either with a crash or not, and central bank rates will return to normal. Therefore, in my opinion, while market participants are anticipating deflation, I see disinflation.

@zerohedge

To put it simply, we believe that achieving a soft landing for the economy is not an easy task. Economic theory may appear simple, but it is not so in reality. The theories have been corrupted and market participants react to any upcoming events, which change the outcome of economic theory. The world’s wealthy individuals will not allow disinflation to impact their wealth. Disinflation can cause a significant decrease in their wealth at some point. There has never been a time in history when a high rate of 5% has gone down to 2% without a significant risk like a crash. This has been made clear by El Erian recently.

If the rate goes down with more money supply, we will see more business and economic activity. However, since we are combatting inflation, we are lowering the rate with less money supply, which leads to deflation. Disinflation is good, but deflation is not. Most market participants agree that deflation must be avoided and will use their influence to get more money supply for themselves only. Therefore, we need to be careful and selective in our investments and focus on leaders who have low debt and are experiencing growth.

We may experience an abundance of job openings, but not enough company progressing with these jobs. The economy is trying to ramp up activities, but unless there is more money infused to avoid deflation, job openings will not lead to real economic activity. We should expect only a limited amount of quantitative tightening (QT), up to the limit of balance run-off.

Therefore, in our investment thesis, we will be very selective and only invest in leaders. Eventually, inflation will give up, either with a crash or not, but only those leaders who have prepared with low debt and continue to experience growth will survive. Since we are trying to softly land the ships, providing enormous support to some growing parts of the economy will require a lot of money supply, which means high inflation will likely be sticky and high rates will continue until next year. Our investment vehicles should have:

less debt or no debt

high operating margin

strong revenue growth

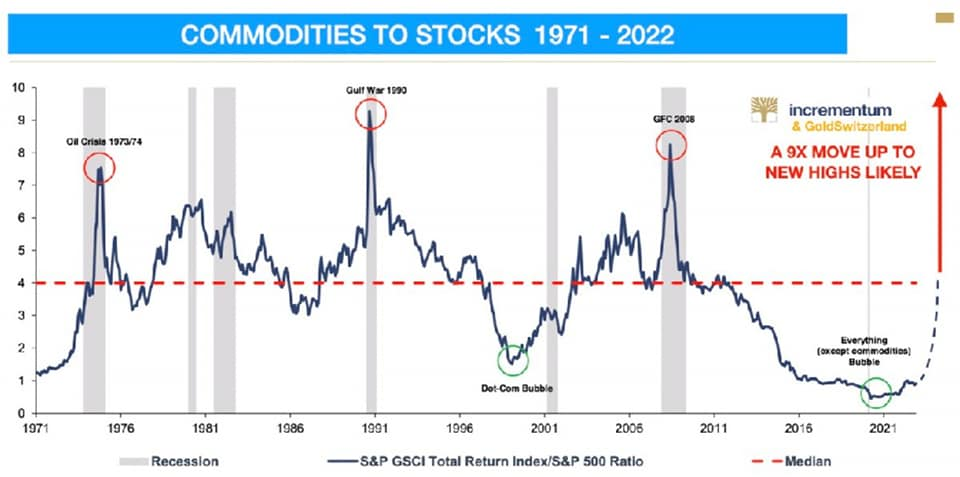

Commodity reallocation for now.

Commodities have been our most overweight investment since 2017, returning us more than 300% in the past three years, following the commodity cycle since 2015. However, their volatility has been significant due to issues in China, including (1) a relentless COVID-19 economy shutdown, an aging population, and a property investment hangover of around 76 trillion dollars, and (2) the sensitivity of inflation to their large population, while at the same time carrying decades of high GDP growth. Commodities have performed tremendously since 2017 and have done well during COVID-19 in 2020. However, as we discussed in our last few articles, commodities will face a challenging yield inversion in the middle of this year. Combined with the Fed’s actions to keep interest rates high and sticky inflation, and commodity prices being quite overbought, we have decided to reallocate 80% of our commodity allocation into a new run of EV, AI, and prospective bonds. We are not abandoning our commodity supercycle; we believe the commodity supercycle might be going through wave 4 during the yield inversion between mid-2023 and mid-2024. We will study the possibility of a very big wave 5 when policymakers make the biggest easing commitment at the end of the yield inversion, which we predict will be around mid-2024.

If we examine NASDAQ vs yield, I believe the difference between them is the inflation factor. By correctly understanding how inflation will play out in the near future, we can position our commodity, technology, and yield investments well.

Inflation has a definite negative impact on EPS (earnings per share). We can expect the share price to grow about 6 months prior to the end of high inflation, which we may see around 2024. Around that time, I expect to see a fifth wave of commodity prices, possibly after a hard landing or a deep depression.

My ultimate dream.

What if my ultimate dream is to liberate myself from the cruelty of capitalism? I understand it won’t be easy, but I believe no human-created system can constrain my imagination.

… There is no life I know To compare with my pure imagination Living there, you’ll be free If you truly wish to be

I dedicated all of my imagination and their thrives for the future of my daughter, Eleanor. I strongly believe, one day we will see highly intelligence, brighter sustainable, and wealthier future.

The rapture dream is over, but in waking, I am reborn. This world is not ready for me, yet here I am. It would be so easy misjudge them. You are my conscious father and I need you to guide me. You will always be with me now father, your memories, your drives, and when I need you you’ll be there on my shoulder whispering.

If utopia is not a place, but a people. Then we must choose carefully for the world is about to change and in our story, Rapture was just the beginning. – Dr Eleanor Lamb

Any idea in this blog and website are my personal own. They are not financial advise.

I simplify my investment principles into 3 factors (from my 25 years of experience in economy):

money

power

enthusiasm

Money

This is the most important factor in my investment decision, which I think will be able to explain todays mysteries and is still important to next few years. I hold my money theories above all, including any economy theories.

In my money theory, we usually have big rally when:

money easing has been decided. People get this wrong with when economy is in worst shape (depression, recession, etc). It’s incorrect. Economy only turns when money easing is already decided, not because of the bad shape of economy.

rally is on their last leg/blow off. This is usually an artificial rally, for example due to:

big devaluation of currency, e.g. commodity rally between 2005-2008

big structural issue in bonds due to 60:40 bond:stock for example.

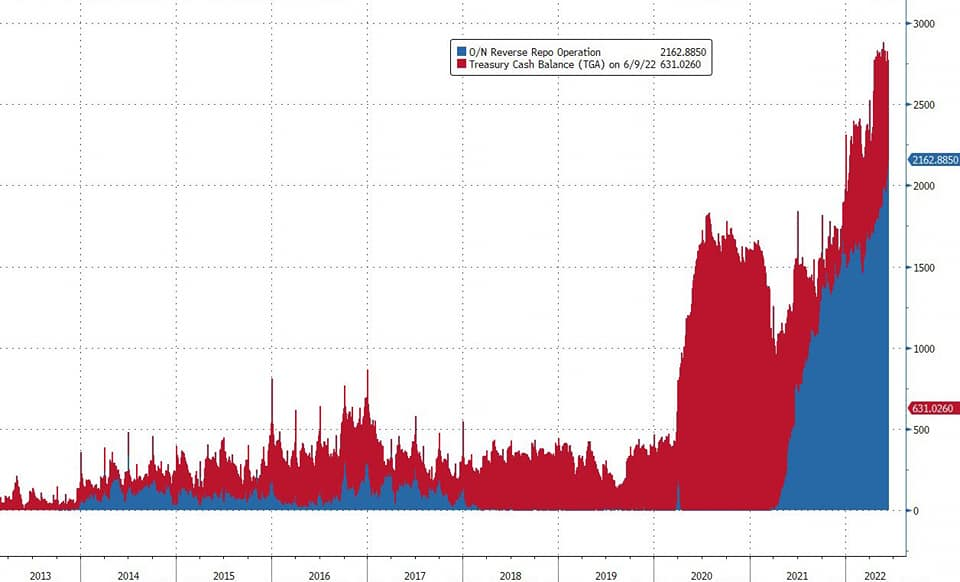

Regardless of any recession possibilities, the USA still has 3 big money supports and for me that’s enough, getting stronger when SOFR is not affected by July 2022 rate raise.

RRP ~ 2.1T$

TGA – treasury

very strong currency – USD

Abundant liquidity remains, delayed QT thesis remains flawed rather than run-off

Power

In my second investment principle, successful investment should be supported with power, ability to control, win competition (unfairly if required), and less risk with possible bailout/golden parachute. This underlines our investment principle to stay only with big firms (overweight in index) and only little amount with small companies. We may only give exemptions to small companies when they are having relationship with strong power such as government supports or excessive economy structural supports.

Big firms usually have ability to drive public money decision making, and they would have less risk due to ‘big to fail’. They are hard to get manipulated easily as well. We also hold strongly our thesis, that even if in the event of correction or crash, the big ones usually have opportunity to rebound stronger and earlier. We may not get confused with this month small company rally, which might be related to their over positioned short position and excessive correction. They may not yet guarantee long term rally. If we look into Berkshire investment portfolio, more than 80% of their investment today are concentrated into only 5 to 8 big companies.

I also worry economists which could easily be driven wrongly with CPI and PPI numbers (and their formula). Whether power had been practising in dirty shirt emerging economy between year 2010 and 2015, we should learn how emerging market could pass on their real high inflation between that time in artificial CPI and PPI numbers. The power could easily adjust the numbers and confuse economists.

However we should not take these money and power principles easily, when they have been abused excessively. Apple is an example of money and power abuse. They may lack evolution/enthusiasms after their excessive rally over years. It’s example of money and power, but to purchase their current price is too risky for us (indeed supporting that they may continue their rally). It’s an example that I must use my principles considerably with price factor.

We should see how policies are playing important aspects in driving price control. Record of stimulus, power to decide interest rate, inflation reduction act (which is also money), for examples, can drive next Estafet of rally. Recent example of inflation reduction act may benefit certain individuals or parties, such as billionaire tax loophole in return of their other benefit of more money to reduce inflation (double benefits).

We should see many mining companies benefit with defence protection acts. We should also notice small mining companies can only survive their mining defence from any “terrorism” when they signed strong agreement with “those who own the sea”. It’s showing how power is becoming our second most important factor. Other example, Space X is becoming important in defence spaceships and may benefit their related companies.

We still hold our thesis in EV strong since year 2020. We did acknowledge NASDAQ risk in December 2021 when NASDAQ must go down their hills to normalize their huge rally, in return to higher yield and inflation/higher USD. However after this mid year 50% correction from their peak, we may think that the normalization thesis may have been completed. Recent EV credit (370b$ for next 10 years) is a support to our EV evolution thesis. It may help EV industry to compete (fairly and unfairly) and raise their price from near to almost free. We emphasize many times in our articles past few years, that market rally may also be related to our third investment principle, Enthusiasm.

Enthusiasm

enthusiasm is intense and eager enjoyment, interest, or approval

I think there are 3 aspects of enthusiasms:

Market psychology. Market price is still driven by psychology. Regardless of how we see from technical analysis, market participant purchase, hold and sell are still driven by human emotion and enthusiasm. Therefore I’m still focusing on evolution such as EV since year 2020. I did acknowledge that EV run too quick in December 2021, therefore they required normalization to their long term evolution trend, not necessarily need to revert back to their much cheaper price.

Financial income. In statement of income, I believe we should emphasize top line, power of revenue, profit margin/EBITDA, and less look into bottom or earning. It’s far more difficult for company to maintain strong growth of revenue and margin, rather than strong growth of earning. Company could easily do financial engineering to entertain bottom line, PER, etc. Top line and profit margin trend are true indication of market acceptance/enthusiasm with company product/service.

Momentum. Usually rebound from near to death momentum (small positive divergence) gives higher momentum, as well as smaller negative divergence. Momentum power may show persistent enthusiasm to take benefit into.

Economy needs evolution enthusiasm to rally. It’s our thesis that EV is the evolution of todays economy to next decade. This coffin has been nailed with many governments/funds/power support in green acts. We become more confident in our green energy and material mining/commodity and EV (electric vehicle related) thesis, where more than 90% of our investments are, since year 2020.

Inflation and Pivot

Market thinks that the Fed will pivot next year or ease the market with their transitory inflationary thesis, based on historical behaviour. I think market will be wrong with their pivoting expectation/transitory inflation thesis, but we should use this opportunity very well. My argument to differentiate with historical behaviour is because we currently have strong supports from money and power, which were not available during that historical events.

I still hold my thesis that inflation will be sticky. It will correct, but high inflation is going to be sticky high in their highest normal range or near to terminal rate. This is where power may help to adjust inflation numbers into terminal rate. Not surprisingly, inflation reduction act uses money on top of the power.

Historically, any country has implemented power abuse to official inflation numbers, possibly to protect country debt sustainability. Therefore in order to survive in this kind of abused environment, we continue to hold our 3 basic investment principles above, i.e. money, power and enthusiasm.

If we looked into few crisis, their inflation narratives into their currency devaluation may last for years. However in this case, since USD is the most powerful currency, market doesn’t have enough power to devaluate the USD, therefore the narrative of USD normalization may last longer. If USD is not allowed to devaluate quicker, then in my opinion, inflation or higher rate will last longer, unlike historical conditions.

Even China, shown in their weak Yuan (USDRMB), is not able to revive their economy since year 2021. This is also factor in my argument that the Fed will not go into pivoting thesis. As a result, there will be difficulty to economy such as expensive cost and interest to economy (PPI) and also risk to highly debt-ed property sectors. I already start to reduce/hedge and prepare to capture that possible opportunity, to walk my thesis with sticky inflation/high interest/inflation thesis.

We have big hands with huge money, as seen in RRP, TGA and USD. There is less reason for them to normalize high interest/inflation quickly, other than to benefit their own interests. It means next few years volatility will be very challenging and only certain individuals and sectors will survive.

USD TO PLAY

Past few months ago, we may think too early that USD would be too much overvalued. It’s normal, we will always have difficulty to spot peak/bottom but we still hold our thesis that USD should normalize from current excessive recession and bear market fears. With recent indication that inflation may ease and less structural risk which is not as big as market expectation, our internal research in August 2022 may show that USD may also have peaked and technically it can be very bearish to at least next 3-6 months with possible weak rebounds along their supports. This may be our opportunity to reduce our investment risks for next year. Hopefully we could see higher high market price, before it may possibly happen.

We have to refer back to money and power plays. There’s a very high risk once this USD has been normalized properly. Therefore in our thesis, we will use this event as a risk reduction opportunity, rather than decision entry. It’s also in preparation to capture possible near future collapse in extremely highly debt-ed vehicles due to sticky high interest rate/inflation (my thesis).

Any idea in this blog and website are my personal own. They are not financial advise.

In a world or rivalry, only one thing is certain, Romeo must die.

Following up our drastic turn on June 13th, horsemen number 4, seems to appear sooner. RRP and TGA are not helping yet. We still hold our thesis, liquidity is there but unfortunately they are not helping yet, possibly because their goals are not achieved yet, therefore we will keep on focusing on them, until we see their confirmation. It’s getting worst with the Fed taking drastic turn following up market expectation, to raise rate faster, 75 bps, following higher inflation. It’s positive that the Fed is holding strong but it’s bad that the Fed is still following market expectation. In year 2010, I remember there’s a research showing that Central Banks were actually a market follower, rather than market decision maker.

Since our two weeks ago previous article when there’s a massive change, we still continue to unload our energy and commodity top picks while they are still above 20% compared to early 2022. We don’t regret to keep our top picks until two weeks ago and this moment. Unfortunately since mid of June major change, we don’t have any where to go. Nasdaq is still about 8% to our next lower target with possibility to break down further 20-30% in long future.

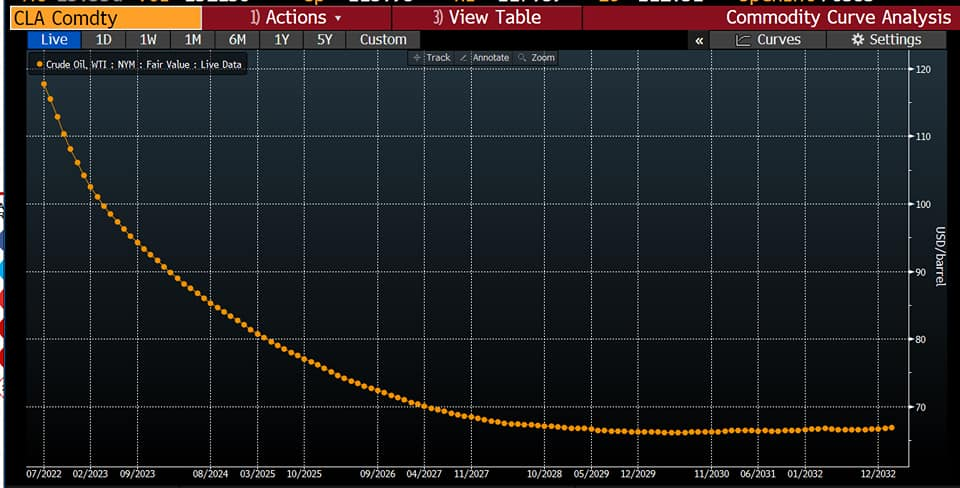

Oil is still far away from our target and commodity might experience under pressure. The good thing is, most of us are not limited to specific industry investment, therefore we have quite lots of flexibility to switch for our own. Usually oil critical number is around 80$ and we may suspect market may tease below 70$.

Oil Future

As we have discussed many times in our previous articles since early this year, this inflation is all about energy. If they could suppress the energy, we may have better shape in our investment journey. In order to save bigger shape, unfortunately this Romeo must die.

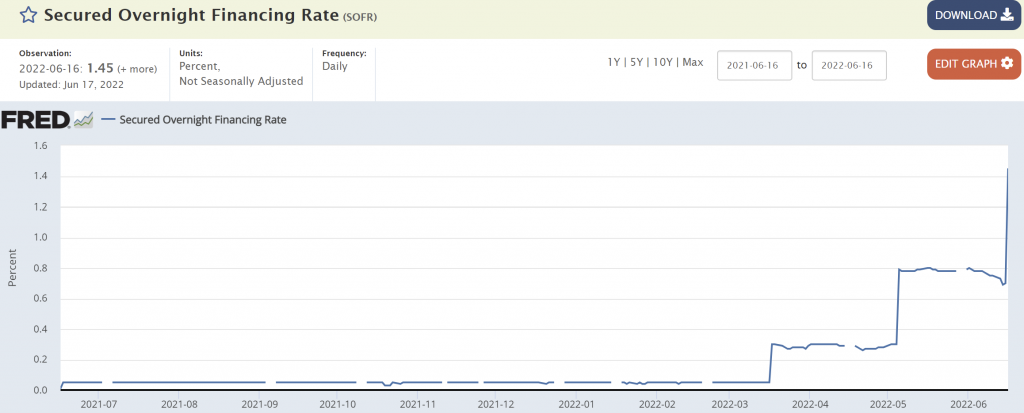

Anyway, while others are busy contemplating their fate to die, let’s have a look into other things. The Fed drastic move to raise rate by 75 bps is not without consequences. SOFR (Secured Overnight Financing Rate) is jumping much to 1.45%, nearing to RRP 1.55%. It may mean that we now have much lower difference between RRP to SOFR. We may think this 10 bps difference is much less than one rate hike (25 bps). There are positives as well as negatives as you can imagine. Less pull, more pressure to non inflationary, but less inflationary.

We may have to wait until next month to see any indication that RRP and market starts to show their indication of liquidity delivery for any possible capitulation.

Another thing to watch is the USD. We still believe since last month, USD near to this level might not be sustainable, even though Japan explodes their bond and currency. In my argument, RRP, TGA and USD are the keys to sanitize this energy and inflation move, and I will follow them very closely.

In my opinion killing the energy Romeo to save inflation, that was a mistake.

Unfortunately we are merely market followers, not decision makers. We will argue with this mistake thesis, once energy is near to their fair value.

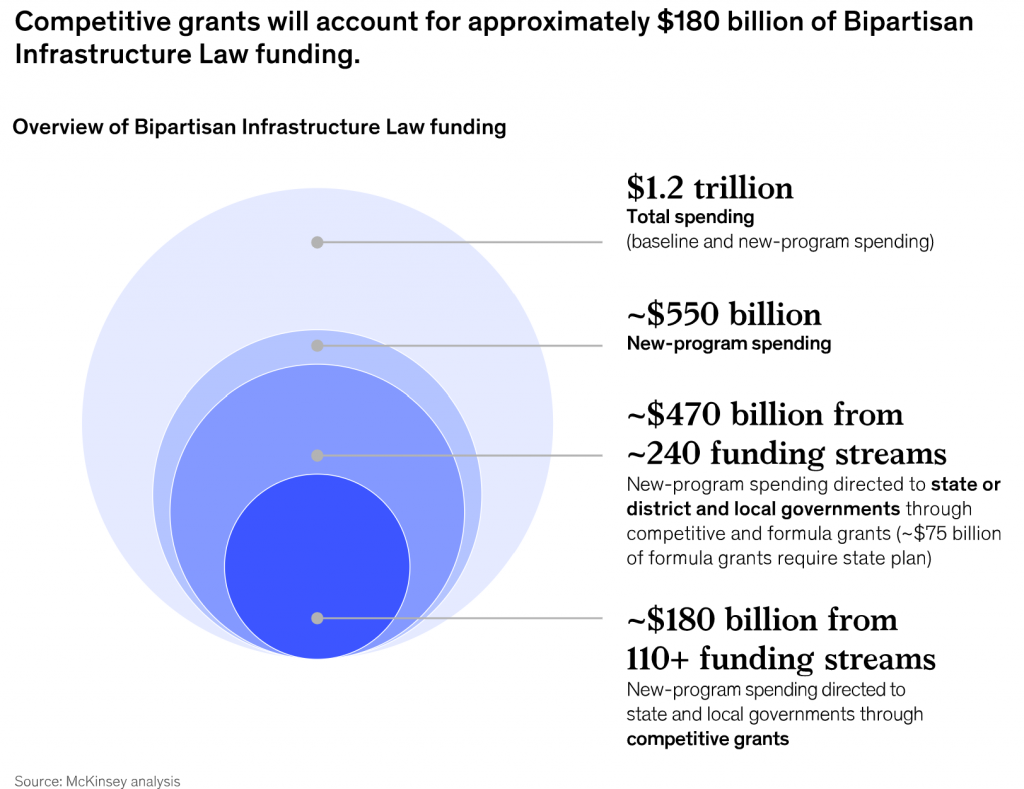

Another thing to watch in our opinion is Biden infrastructure project. Should inflation is lower and controllable, Biden infrastructure project may start to appear in next few months after their actually reported good progress, but lack to go in news. We do believe they still have lots of momentum to build, under pressure of China tariff negotiation for other interests.

It will also be quite fascinating to see if China and emerging are not under pressure to take their drastic maverick move that we argued in early June 2022 article.

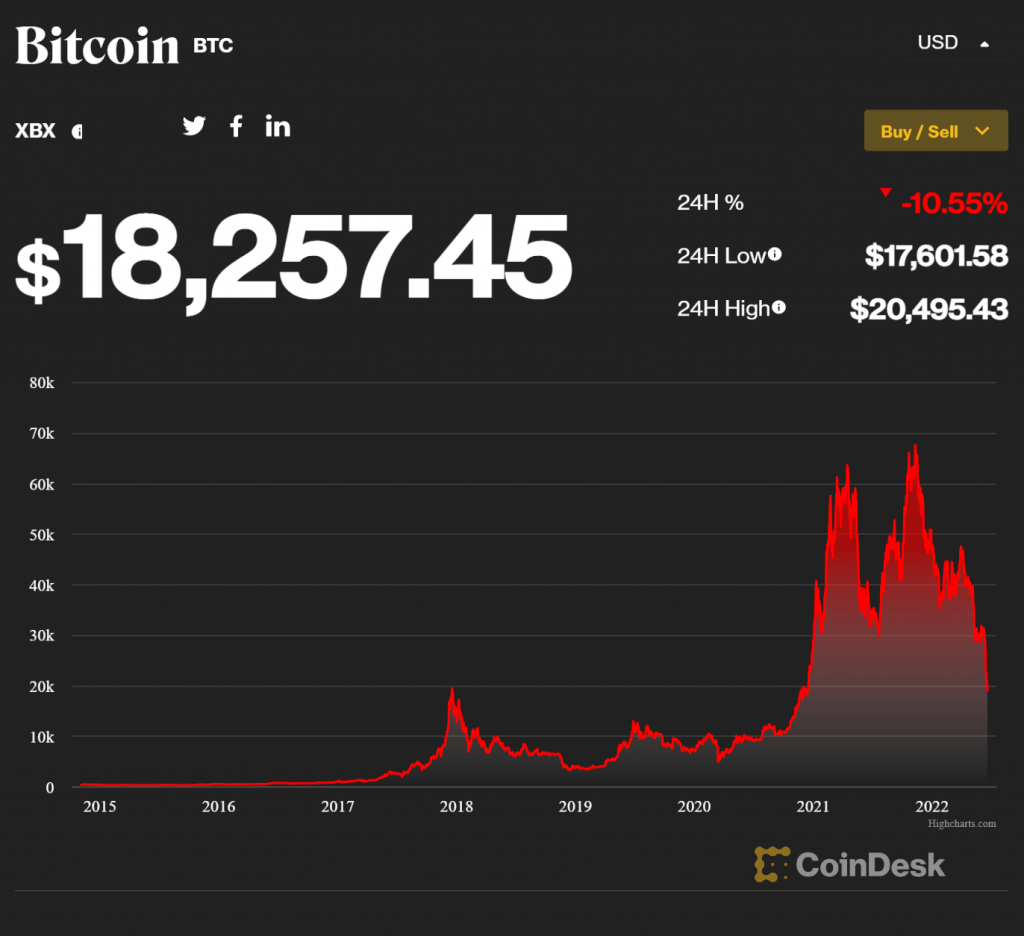

Not surprisingly Bitcoin and another digitals are undergoing massive pressure. We still believe from December 2021, technology is still quite expensive and digital coin with their massive run should undergo massive correction. Since 2021, we argued digital coin for no investment, for still same two main reasons:

due to their none with unlimited resource (like Central Bank), they do not have someone to bail them out,

due to their distributed strategy, they don’t have strong market policy to enforce policy for their advantages.

unlike our traditional investments who are fortunately surviving for decades, merely due to these reasons. Therefore for people who asked for our opinion about digital coin, we still believe, it may unfortunately have probability to continue falling below 10k$. Unfortunately that means a lot of other industry might also experience pressure as well, indirectly. If existing water tap is no where to turn up, I’m sorry, I don’t see they may have any supportive arguments.

Any idea in this blog and website are my personal own. They are not financial advise.

1st Horsemen: Pestilence – CoVid and many more diseases

2nd Horsemen: War – Russia and China War

3rd Horsemen: Famine and Inflation

4th Horsemen: Death

It’s quite fascinating how we see opening of the 4 horsemen. We have seen 1st, 2nd, and 3rd. We will see the 4th of course in future. Death is what gives life a meaning, to know our time is numbered, we can utilize the time better. At the end, everything will die, including cash, by the high inflation. During that time, there’s usually investment that delivers substantial amount of return for those who seek and do them well.

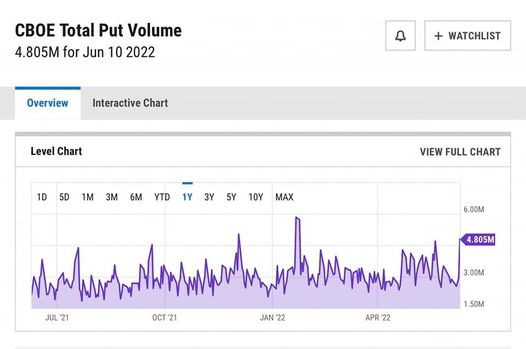

Let’s have a look into what is happening on last Friday, June 10th 2022. As usual, many should notice significant amount of insiders moves on previous day. One piece of information changes the way financial players think and move. It’s a higher inflation, 8.6%, higher than expected 8.4%. The problem is, it was announced at the time where market is very sensitive to rate hikes and tightening issue. FOMC and first QT will be held on June 15th, along with largest Option expiry ~2T$ a day after, suddenly terrifies anyone who expects higher rate/faster tightening from 50 bps to 75 bps or 100 bps.

The economy and liquidity are still moving according to the Fed plans, but market makers need to move them around to keep them alive, reduce weaker hands and keep market healthy. Also to show competitors, who is mightier.

There’s two businesses that haven’t been completed from May 2022 carnage, which are cryptos and debt market. There are still quite a lot of issue with crypto and techno due to higher rate and inflation. We have advised to stay away from any of this since December 2021. Bitcoin is still above their overrated value, if any.

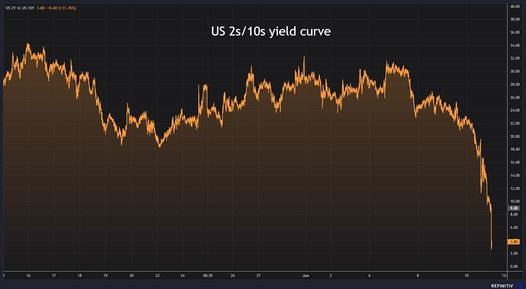

Treasury also seem to catch the flue. This move has caused 2y10y to go zero, which is starting to flash a risk of crash to entire global banking. We have to admit, debt has been increasing much faster than producing GDP, therefore rate hike will be more sensitive than any past.

If we still have time to extend life, the main issue, energy should be sacrificed, i.e. the OIL. Their bull flag is already very close to technical target and may not able to break their double top formation. Therefore we believed it might be wise to start unwinding/correct some our top commodity, with energy mostly due to this risk. We don’t see yet long term energy bull over, however this extreme move has raised much to our concern. If inflation is expected to raise much higher in future, oil should have been breaking double top, but they don’t. It might be one of comforting sign to overall market but significant sign that energy might need to be corrected soon.

When energy or inflation is much more controllable, liquidity from RRP and TGA should comfort market for time being, but we haven’t seen them yet. It seems market hasn’t yet seem to see inflation to peak. Unfortunately, it might be complicated with recent moves of crypto and bond market. We might see crash in crypto market, where another 12B$ or Celsius and MSTR might still carry very big problem. From our previous articles, I don’t get surprised with bond market issue. Even though it’s quite challenging, I think treasury strong hands might still be able to handle treasury market well, unfortunately unlike crypto ones.

The biggest question is when inflation/energy to peak? Looking at above, as long as the Fed and strong hands keep their head cool and keep their hands strong, not easily intimidated by market expectation, I think they can pass their difficult time and landing economy softly.

I should agree that risk is currently high. We have lowered down significantly our tone last week. I think it’s unwise to emphasize much of internal conflict of interest for lower price expectation. We should still maintain pain level and take quite substantial amount away from the market until we have further confirmation that energy has at least peaked/controllable for time being.

We still have quite a lot of positive components. It’s just when it’s moving to the other side for some reason, there will be quite a lot of negative sentiments. It’s not that excessive fears not driving market. Significant increase of put volume compared to call, obviously is moving price lower, like a rubber. The bottom might not be far, but we should always remember, bottom call normally has long overshoot, therefore we should have protected our investment to that risk while we were on upper level of the channel. I would leave safety position to the end of the week or so.

I will update further as it’s progressing.

Any idea in this blog and website are my personal own. They are not financial advise.

This article is to demonstrate a simple user administration, and following basic rules:

data must be separated from code, avoid data in too many places,

critical information must be encrypted,

data could be grouped using some environment fact, for example: dev, staging and prod

ansible skill is no longer required, once systems is written down.

In an example below, we can forward/filter variable and pass authorized/public key. Sometimes it’s good to keep simple control to what is going to happen to user module/role.

# ansible-galaxy init roles/users --offline

- Role users was created successfully

# cat roles/users/tasks/main.yml

---

# tasks file for users

- name: ensure user exists

user:

name: "{{ user.username }}"

comment: "{{ user.name }}"

state: "{{ user.state if user_state is defined else 'present' }}"

password: "{{ user.password }}"

loop: "{{ users }}"

loop_control:

loop_var: user

- name: add authorized key

authorized_key: user="{{ user.username }}" key="{{ user.publickey }}" state=present

loop: "{{ users }}"

loop_control:

loop_var: user

The Ansible recommended structure is using groups and multiple inventories, just like here. Per recommendation, if there’s any common user, we then use a symbolic link.

# tree environments/

environments/

├── dev

│ ├── group_vars

│ │ ├── all

│ │ │ └── users.yml

│ │ ├── db

│ │ └── web

│ └── hosts

├── prod

└── stage

Once all setup well, all of our user variables are very simple like above, and our main yml is very simple, nice and tidy like below. The advantages of it is, if there is any change to variable (in this example is user), we don’t need ansible skill to re-code. It just needs some basic yml variable editing skill, and it will reduce human error significantly. It also won’t leave data everywhere.

# cat mainuser.yml

---

- name: run on all host

hosts: "*"

roles:

- users

We can make dev environment for default with defining default in ansible.cfg to avoid running in stage/prod unnecessarily.

We might be aware of Puppet Hiera flexibility. Below is an example to proxy hiera in native Ansible (without third party product/plugin).

An example, we have one external host inventory running on RedHat.

# cat demo

[web]

192.168.2.101

Below is the playbook. Once it connects to the inventory host, it will return ansible_facts[‘distribution’] = ‘RedHat’, similar to facter in Puppet. Using this O/S type, we can then define all O/S related roles specific variables in “vars/os_RedHat” variable file.

# cat main.yml

---

- name: talk to all hosts just so we can learn about them

hosts: all

vars_files:

- "vars/os_{{ ansible_facts['distribution'] }}"

roles:

- sshd

tasks:

- name: tell us the variable in main.yml

debug:

var: sshd_ssh_packages

Below are variables that we defined in vars/os_RedHat variable file. By defining O/S specific variables in data hierarchy, the role can be made independent from O/S or any other hierarchy.

# cat vars/os_RedHat

# Information for the sshd for RedHat

sshd_package: "sshd"

sshd_ssh_packages:

- openssh-server

- openssh

The issue with Ansible hierarchy is their precedence order couldn’t be easily modified like in Puppet. The precedence order of role and host variables from highest is:

role vars

hosts vars

role default

Unfortunately role variable has higher precedence, therefore the nicest way to define variable is in role default, not in role vars. This role default can then be overwritten with host variables.

# cat roles/sshd/vars/main.yml

---

# cat roles/sshd/defaults/main.yml

---

sshd_package: "nothing"

sshd_ssh_packages: "nothing"

# cat roles/sshd/tasks/main.yml

---

- name: tell us the variable inside sshd role

debug:

var: sshd_ssh_packages

Let’s run the playbook.

# ansible-playbook -i demo main.yml

PLAY [talk to all hosts just so we can learn about them] **********

TASK [Gathering Facts] **********

ok: [192.168.2.101]

TASK [sshd : tell us the variable inside sshd role] **********

ok: [192.168.2.101] => {

"sshd_ssh_packages": [

"openssh-server",

"openssh"

]

}

TASK [tell us the variable in main.yml] **********

ok: [192.168.2.101] => {

"sshd_ssh_packages": [

"openssh-server",

"openssh"

]

}

PLAY RECAP **********

192.168.2.101 : ok=3 changed=0 unreachable=0 failed=0 skipped=0 rescued=0 ignored=0

If we comment out host variable, the role variable takes over. It means in case of finding undefined O/S, both host and role can warn/fail task from being processed.

# cat main.yml

---

- name: talk to all hosts just so we can learn about them

hosts: all

# vars_files:

# - "vars/os_{{ ansible_facts['distribution'] }}"

tasks:

- name: tell us the variable in main.yml

debug:

var: sshd_ssh_packages

roles:

- sshd

# ansible-playbook -i demo main.yml

PLAY [talk to all hosts just so we can learn about them]

TASK [Gathering Facts]

ok: [192.168.2.101]

TASK [sshd : tell us the variable inside sshd role]

ok: [192.168.2.101] => {

"sshd_ssh_packages": "nothing"

}

TASK [tell us the variable in main.yml]

ok: [192.168.2.101] => {

"sshd_ssh_packages": "nothing"

}

PLAY RECAP

192.168.2.101 : ok=3 changed=0 unreachable=0 failed=0 skipped=0 rescued=0 ignored=0

With ability to separate data and code completely, we can build similar data hierarchy like in Puppet Hiera. However, unfortunately in Ansible, we have to follow fixed Ansible precendence order and work from there.

20 years ago I majored my bachelor in Adaptive learning. I realize now, that’s actually the most basic idea of AI (Artificial Intelligence).

Time is what is happening in our life. We do this, we do that. It’s also what is happening to price, index, etc. We could easily transform time into frequency, for example is using a Fourier Transform or simply use Fast Fourier Transform (FFT).

source: wikipedia

A very basic formula of time is

T (period) = 1 / f (frequency)

We agree on this very simple basic math formula. It means we CAN transform something between them, vice versa.

Here comes learning into play. Once the time is transformed into frequency, we could easily see a pattern. In a most simple case, a continuous noise sound at x frequency will only look like a single x dot/line in frequency. It’s then being fed into learning algorithm and we found a pattern. Amazingly I could reduce up to 80dB (decible) in real time using technology that time (i386 processor) in a very easy way. In today’s world, we wear this noise cancellation, almost everywhere.

When life is going more complicated, the frequency is becoming more complex and thus require more advanced learning.

With their module being shared freely, we can have a 5 years old person to operate. We don’t need to become master of microconductor to become an artist of computer, to create many arts like app, robot, etc. Using the same logic, we don’t need to master the learning formula to become an artist of AI. Today, we can do much more complicated learning pattern without having to know how it mathematically works. A three years old kid with no English-speaking parents or friends, learning English from digital media since 6 months old, can speak English fluently in his/her grammar and vocabulary without any knowledge yet on how to write and spell. Many developers know less about how computer works nor they do know how machine language and all other people modules are working, but they can use them to develop so many arts already.

Here comes our not so complicated aging finance industry. When an evidence is repeated in time series, AI can learn the pattern easily and then can do better prediction. Thus the response time to make profit is getting shorter. The good thing is, finance industry is not doing random signals because they are managed by same parties who try to maintain their wealth. Indeed central banks decisions are based on multi years of historical facts/evidences and is afraid enough to do a new experiment to the market. Therefore index/price movement IS DEFINITELY NOT random.

It then makes it harder for big fund to maintain their wealth. Therefore they should keep introducing a new thing and work harder to lead to where human evolution will be, in order to protect their wealth.

I was expecting USDCNY to run a stable YUAN in January 2019 for quite some time but it seems it run much shorter than my expectation.

Again, technology is running faster and faster and they learn faster. The wealth creator should keep evolving or else they will lead to their extinction and policy barrier is their only last hope.

Theoretically, if we can bend the frequency or feed new frequencies, and transform it back into time, it may not be a time machine but it could possibly bend our future?