In a world or rivalry, only one thing is certain, Romeo must die.

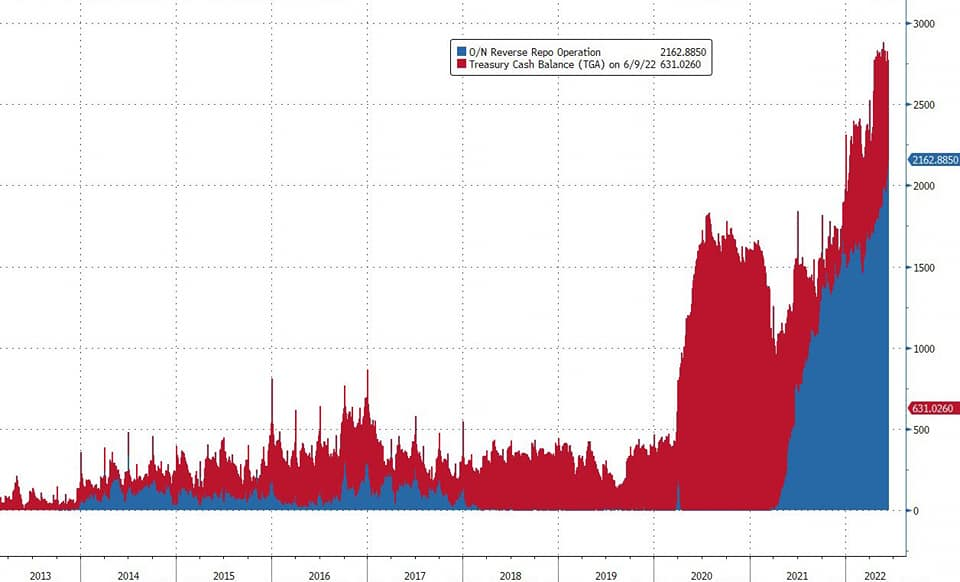

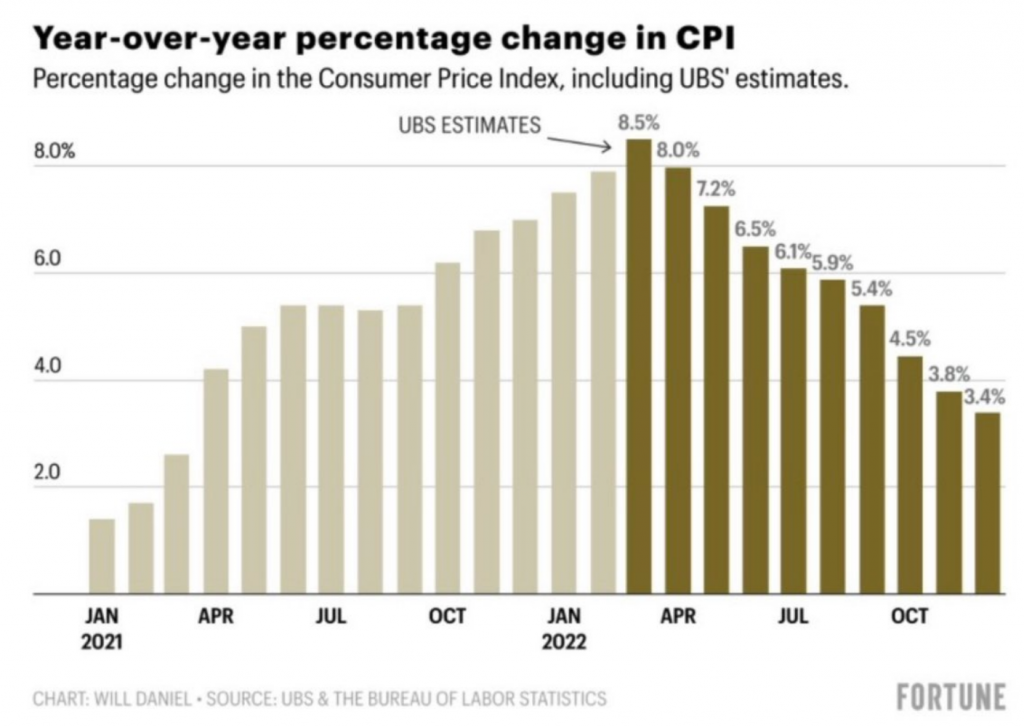

Following up our drastic turn on June 13th, horsemen number 4, seems to appear sooner. RRP and TGA are not helping yet. We still hold our thesis, liquidity is there but unfortunately they are not helping yet, possibly because their goals are not achieved yet, therefore we will keep on focusing on them, until we see their confirmation. It’s getting worst with the Fed taking drastic turn following up market expectation, to raise rate faster, 75 bps, following higher inflation. It’s positive that the Fed is holding strong but it’s bad that the Fed is still following market expectation. In year 2010, I remember there’s a research showing that Central Banks were actually a market follower, rather than market decision maker.

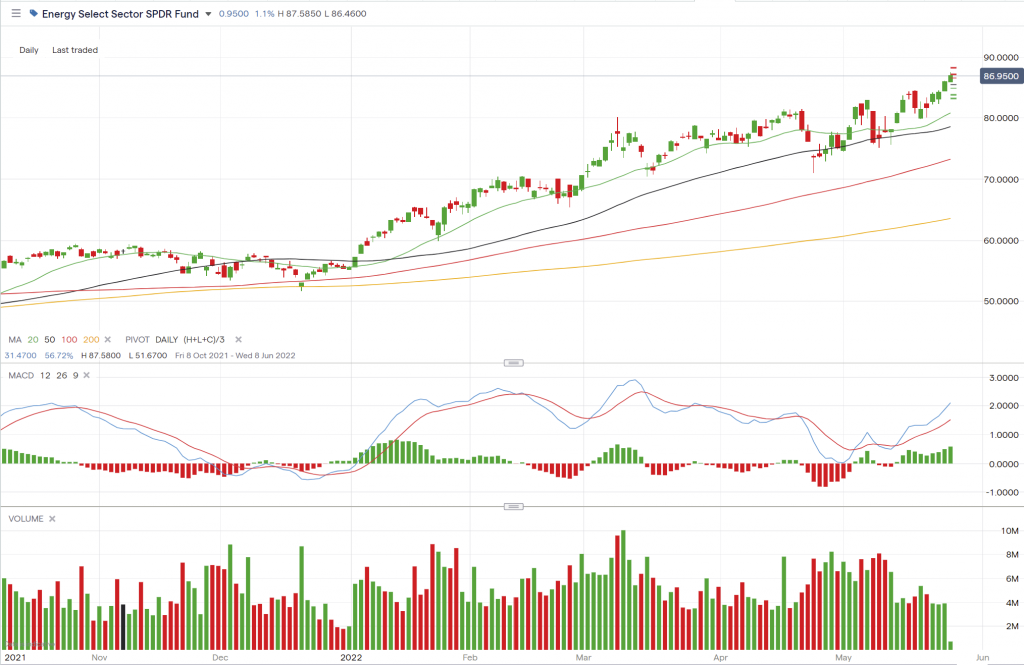

Since our two weeks ago previous article when there’s a massive change, we still continue to unload our energy and commodity top picks while they are still above 20% compared to early 2022. We don’t regret to keep our top picks until two weeks ago and this moment. Unfortunately since mid of June major change, we don’t have any where to go. Nasdaq is still about 8% to our next lower target with possibility to break down further 20-30% in long future.

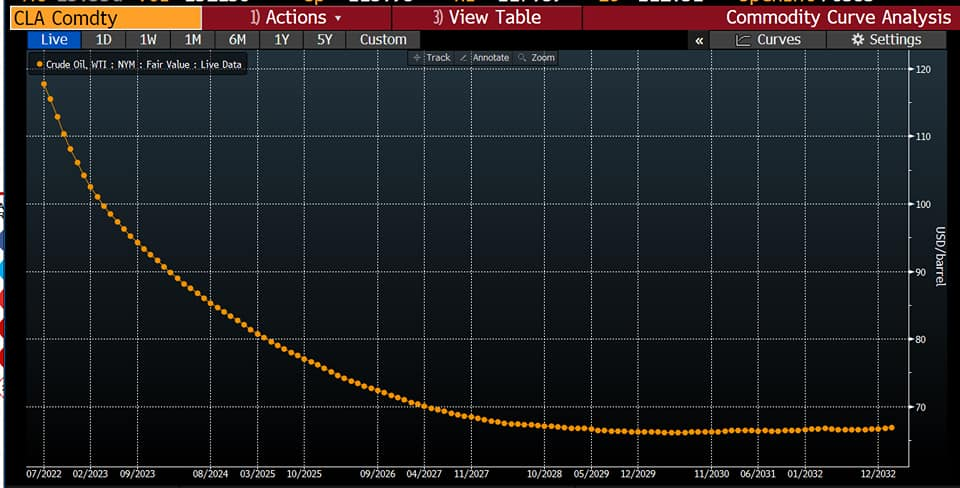

Oil is still far away from our target and commodity might experience under pressure. The good thing is, most of us are not limited to specific industry investment, therefore we have quite lots of flexibility to switch for our own. Usually oil critical number is around 80$ and we may suspect market may tease below 70$.

Oil Future

As we have discussed many times in our previous articles since early this year, this inflation is all about energy. If they could suppress the energy, we may have better shape in our investment journey. In order to save bigger shape, unfortunately this Romeo must die.

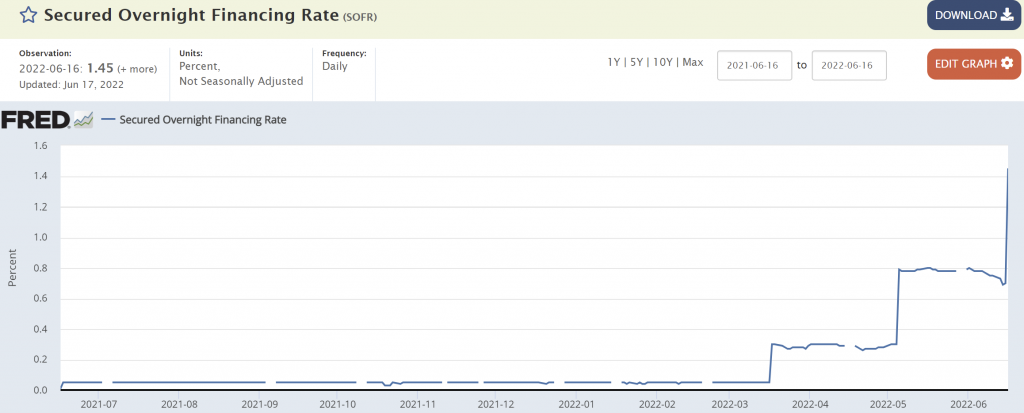

Anyway, while others are busy contemplating their fate to die, let’s have a look into other things. The Fed drastic move to raise rate by 75 bps is not without consequences. SOFR (Secured Overnight Financing Rate) is jumping much to 1.45%, nearing to RRP 1.55%. It may mean that we now have much lower difference between RRP to SOFR. We may think this 10 bps difference is much less than one rate hike (25 bps). There are positives as well as negatives as you can imagine. Less pull, more pressure to non inflationary, but less inflationary.

We may have to wait until next month to see any indication that RRP and market starts to show their indication of liquidity delivery for any possible capitulation.

Another thing to watch is the USD. We still believe since last month, USD near to this level might not be sustainable, even though Japan explodes their bond and currency. In my argument, RRP, TGA and USD are the keys to sanitize this energy and inflation move, and I will follow them very closely.

In my opinion killing the energy Romeo to save inflation, that was a mistake.

Unfortunately we are merely market followers, not decision makers. We will argue with this mistake thesis, once energy is near to their fair value.

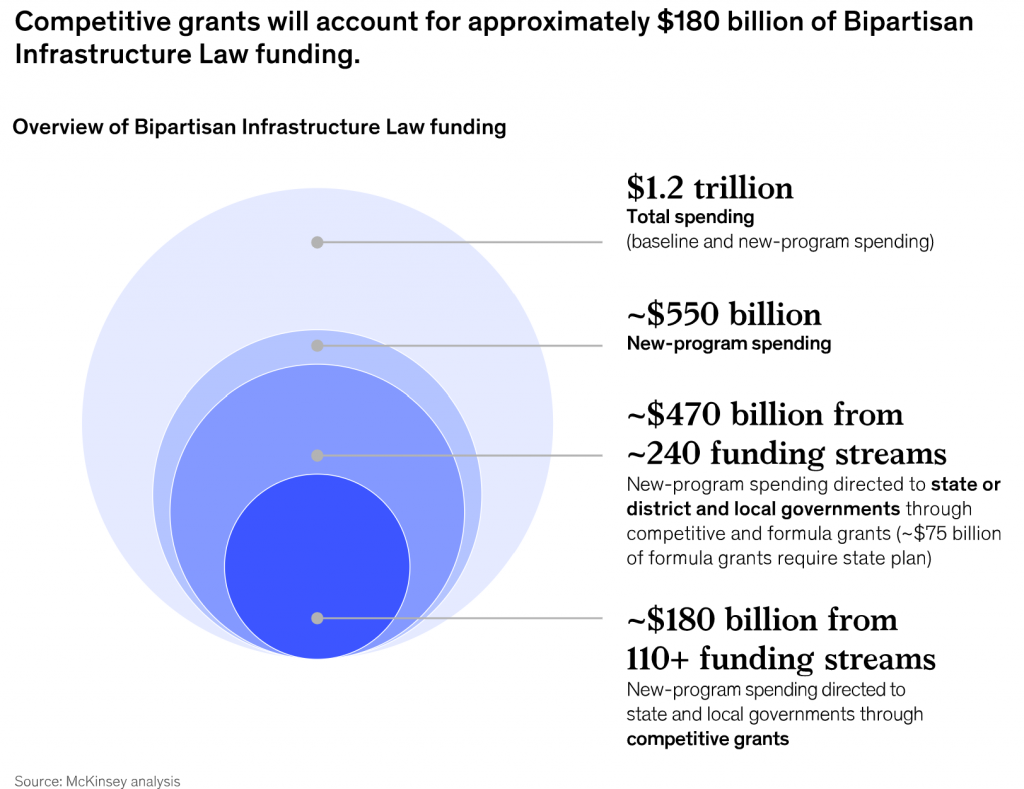

Another thing to watch in our opinion is Biden infrastructure project. Should inflation is lower and controllable, Biden infrastructure project may start to appear in next few months after their actually reported good progress, but lack to go in news. We do believe they still have lots of momentum to build, under pressure of China tariff negotiation for other interests.

It will also be quite fascinating to see if China and emerging are not under pressure to take their drastic maverick move that we argued in early June 2022 article.

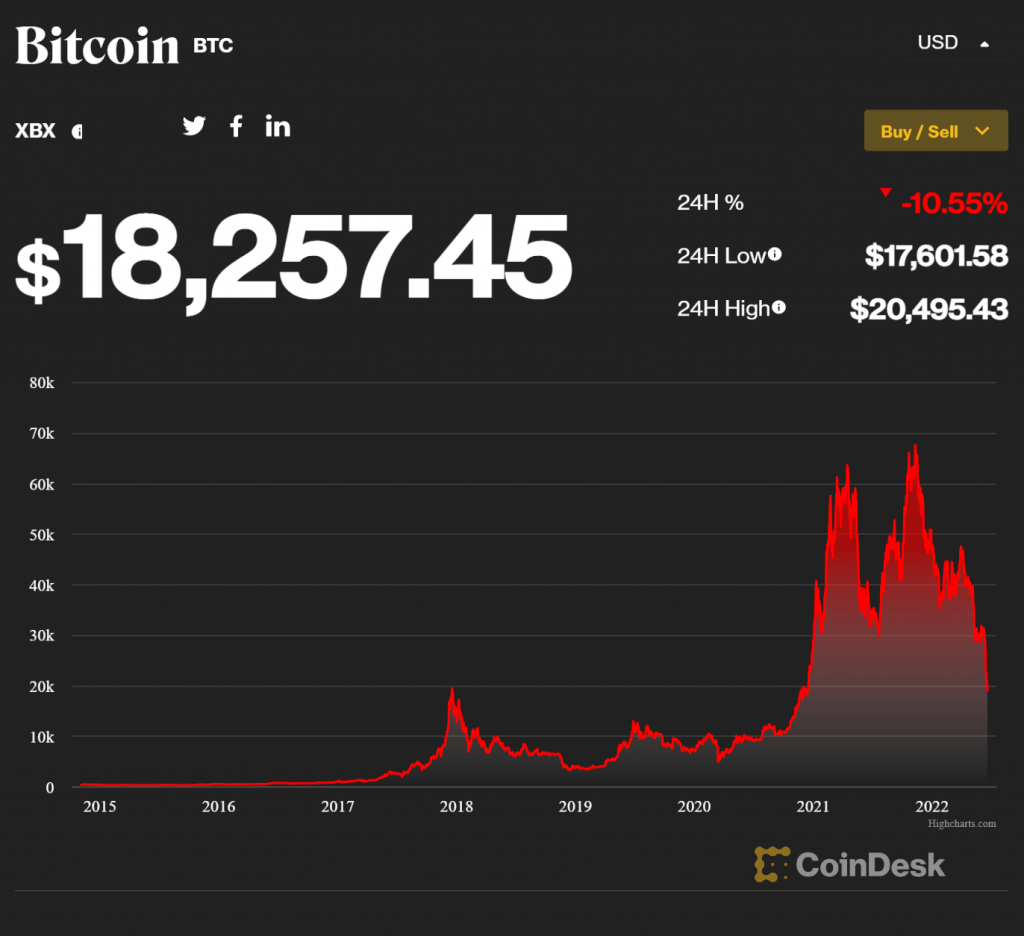

Not surprisingly Bitcoin and another digitals are undergoing massive pressure. We still believe from December 2021, technology is still quite expensive and digital coin with their massive run should undergo massive correction. Since 2021, we argued digital coin for no investment, for still same two main reasons:

due to their none with unlimited resource (like Central Bank), they do not have someone to bail them out,

due to their distributed strategy, they don’t have strong market policy to enforce policy for their advantages.

unlike our traditional investments who are fortunately surviving for decades, merely due to these reasons. Therefore for people who asked for our opinion about digital coin, we still believe, it may unfortunately have probability to continue falling below 10k$. Unfortunately that means a lot of other industry might also experience pressure as well, indirectly. If existing water tap is no where to turn up, I’m sorry, I don’t see they may have any supportive arguments.

Any idea in this blog and website are my personal own. They are not financial advise.

1st Horsemen: Pestilence – CoVid and many more diseases

2nd Horsemen: War – Russia and China War

3rd Horsemen: Famine and Inflation

4th Horsemen: Death

It’s quite fascinating how we see opening of the 4 horsemen. We have seen 1st, 2nd, and 3rd. We will see the 4th of course in future. Death is what gives life a meaning, to know our time is numbered, we can utilize the time better. At the end, everything will die, including cash, by the high inflation. During that time, there’s usually investment that delivers substantial amount of return for those who seek and do them well.

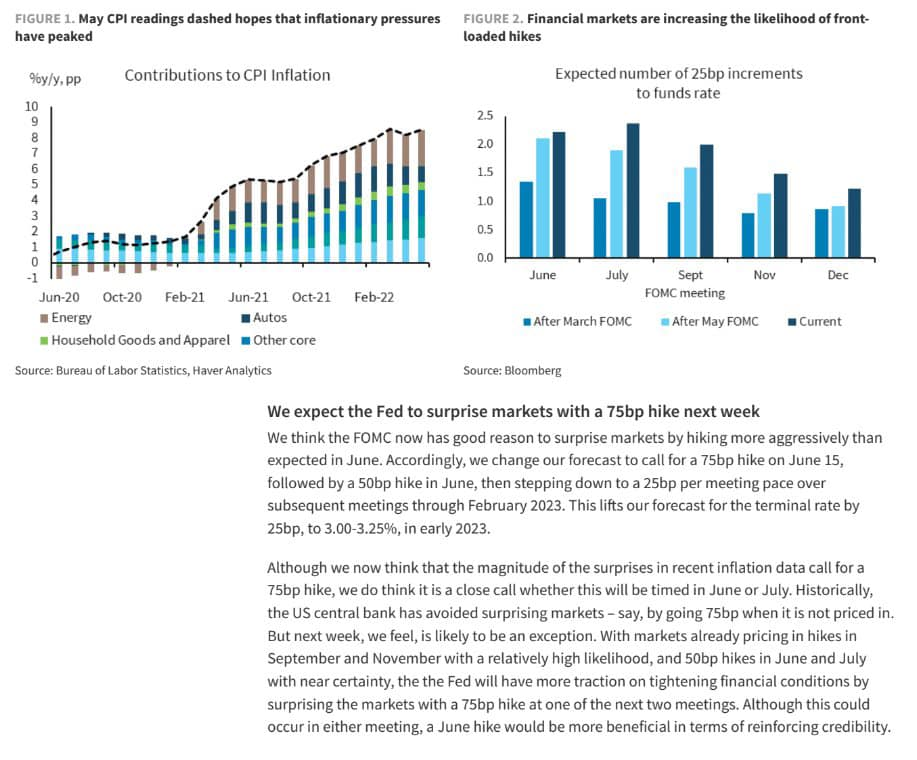

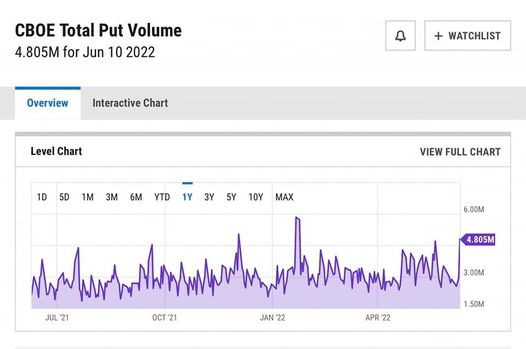

Let’s have a look into what is happening on last Friday, June 10th 2022. As usual, many should notice significant amount of insiders moves on previous day. One piece of information changes the way financial players think and move. It’s a higher inflation, 8.6%, higher than expected 8.4%. The problem is, it was announced at the time where market is very sensitive to rate hikes and tightening issue. FOMC and first QT will be held on June 15th, along with largest Option expiry ~2T$ a day after, suddenly terrifies anyone who expects higher rate/faster tightening from 50 bps to 75 bps or 100 bps.

The economy and liquidity are still moving according to the Fed plans, but market makers need to move them around to keep them alive, reduce weaker hands and keep market healthy. Also to show competitors, who is mightier.

There’s two businesses that haven’t been completed from May 2022 carnage, which are cryptos and debt market. There are still quite a lot of issue with crypto and techno due to higher rate and inflation. We have advised to stay away from any of this since December 2021. Bitcoin is still above their overrated value, if any.

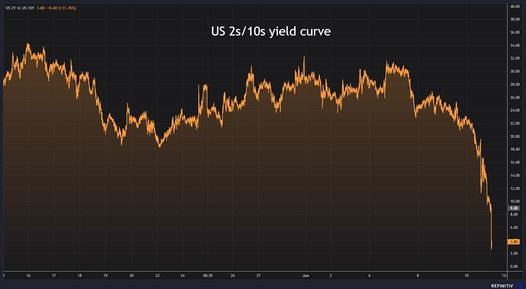

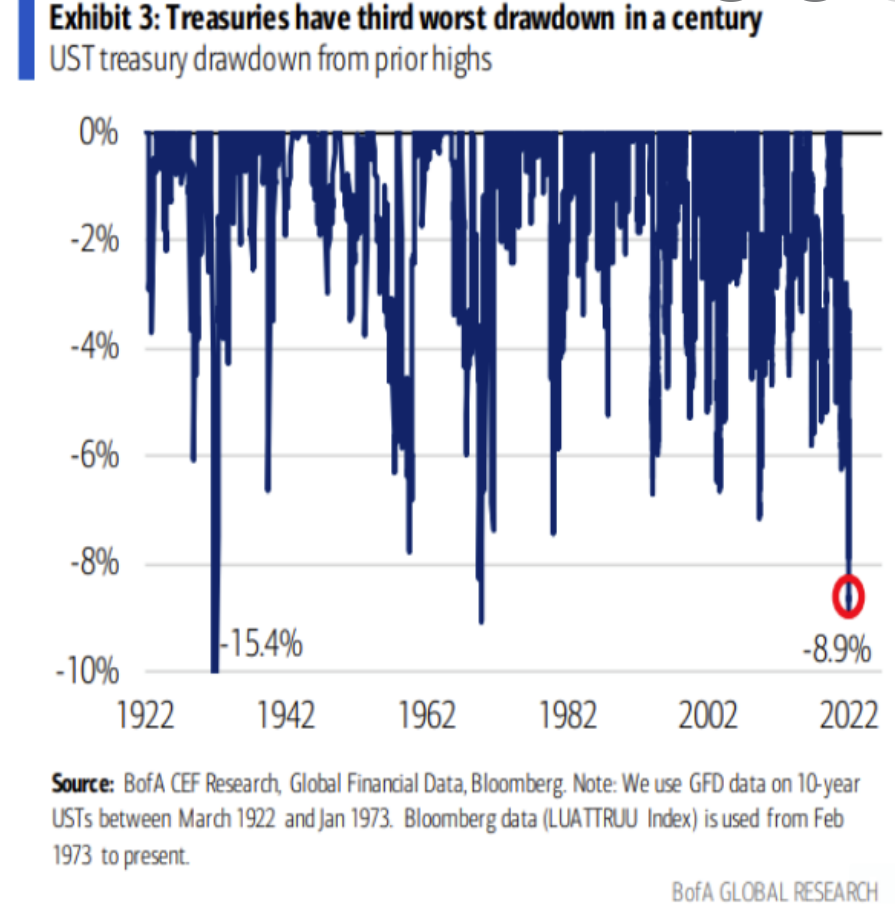

Treasury also seem to catch the flue. This move has caused 2y10y to go zero, which is starting to flash a risk of crash to entire global banking. We have to admit, debt has been increasing much faster than producing GDP, therefore rate hike will be more sensitive than any past.

If we still have time to extend life, the main issue, energy should be sacrificed, i.e. the OIL. Their bull flag is already very close to technical target and may not able to break their double top formation. Therefore we believed it might be wise to start unwinding/correct some our top commodity, with energy mostly due to this risk. We don’t see yet long term energy bull over, however this extreme move has raised much to our concern. If inflation is expected to raise much higher in future, oil should have been breaking double top, but they don’t. It might be one of comforting sign to overall market but significant sign that energy might need to be corrected soon.

When energy or inflation is much more controllable, liquidity from RRP and TGA should comfort market for time being, but we haven’t seen them yet. It seems market hasn’t yet seem to see inflation to peak. Unfortunately, it might be complicated with recent moves of crypto and bond market. We might see crash in crypto market, where another 12B$ or Celsius and MSTR might still carry very big problem. From our previous articles, I don’t get surprised with bond market issue. Even though it’s quite challenging, I think treasury strong hands might still be able to handle treasury market well, unfortunately unlike crypto ones.

The biggest question is when inflation/energy to peak? Looking at above, as long as the Fed and strong hands keep their head cool and keep their hands strong, not easily intimidated by market expectation, I think they can pass their difficult time and landing economy softly.

I should agree that risk is currently high. We have lowered down significantly our tone last week. I think it’s unwise to emphasize much of internal conflict of interest for lower price expectation. We should still maintain pain level and take quite substantial amount away from the market until we have further confirmation that energy has at least peaked/controllable for time being.

We still have quite a lot of positive components. It’s just when it’s moving to the other side for some reason, there will be quite a lot of negative sentiments. It’s not that excessive fears not driving market. Significant increase of put volume compared to call, obviously is moving price lower, like a rubber. The bottom might not be far, but we should always remember, bottom call normally has long overshoot, therefore we should have protected our investment to that risk while we were on upper level of the channel. I would leave safety position to the end of the week or so.

I will update further as it’s progressing.

Any idea in this blog and website are my personal own. They are not financial advise.

You are going on a journey. A journey through memory. All you have to do is follow my voice.

Since there’re many request to have quick advanced look into my personal opinion, before my June article, I write down this special article about my current opinion of my financial journey and how it may end.

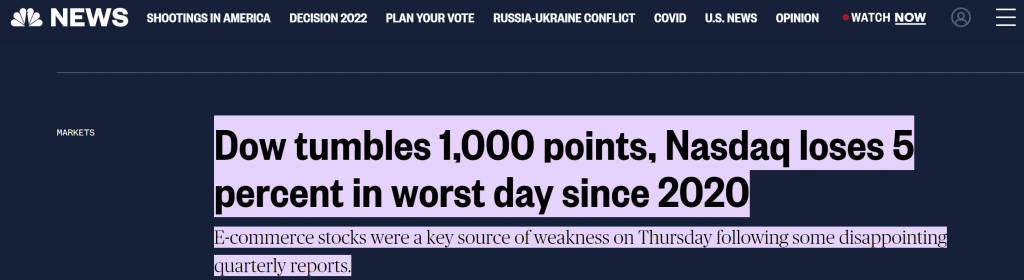

Financial market is going on a journey. All they have to do is follow their strong hands voice, i.e. Central Banks, Federal Reserve, Fiscal Stimulus, etc. I believe, as worst as we may have expectation about the Fed, they are still the strongest in this financial market and deep in their heart, they will try hard to maintain stability of the financial market, including the share market. We might rather see many panic economists in mid of May, AFTER they saw Nasdaq fell hard, flashy crossed recession/strong support line.

blinded panic and fears

Immediately they mistakenly spread fears. Simply, when we are in fear, our eyes, mind and heart are all blinded with the personal curse. I think it’s simply incorrect.

When the water began to rise and war broke out, nostalgia became a way of life. There wasn’t a lot to look forward to, so people began looking back. Nothing is more addictive than the past.

In my previous article published on May 1st, the Multiverse of Madness, I agreed about how severe the condition is and how things would/might get out of hands. I would also agree to take safety measure, especially against Nasdaq and long yield. However as also mentioned in the article, I didn’t close my eyes. There will be a certain point that I would foresee into when to start looking to the bright side/end of tunnel and not just blinded with personal vendetta and conflict of personal interest. In the article, I was aiming around May 22nd and looked to be very close to when the rout was ended. I have to admit, nothing is more addictive than easy QE (Quantitative Easing) bullish of the past.

People don’t just vanish. To find where she’d gone, I had to know where she’d been. Was she running from the past or racing back towards it?

Let’s sit back and re-think. Many strong bullish don’t just vanish. Economy is still strong. Yes many argue in their own opinion, all sudden economy is no longer strong, disagreement, it’s fine. There are still a lot of demand and economy continues their opening from CoVid. Energy is still going strong. Even if you look into opening economy after the CoVid, it’s very hard to get airline seat, and their price is running out with double price. Have we noticed a minimum of 20% necessity price increase, and there’s not much catastrophe. Yes it’s harder for middle class, but supermarkets and restaurants are all fully booked.

Let’s have a look into real reality, strong BULLISH FLAG of commodities and strong bullish of ENERGY. At least I’m not blinded and looked into all opportunities, because I believe simply being blinded to anything is wrong.

Reality

Reality.

It comes to my mind, people are having incorrect definition of recession. Recession by definition is “a period of temporary economic decline during which trade and industrial activity are reduced, generally identified by a fall in GDP in two successive quarters“. People just blindly look into GDP numbers but as it said, it’s generally and very importantly what they got it wrong is with their conditions.

When my daughter asked, whether story can become reality, it comes to my mind, which one is more important, reality or the story? It’s a story of GDP may fall for 2 successive quarters but life of economy at this moment remains strong. If we disagree with strong economy arguments, I get it, but most importantly, reality wise, financial strong hands are still able to manage financial market very well, that should end our disagreement. Around mid of May, I remember there’s a day, USA share market broke strong support and suddenly all economists screamed of recession and crash.

Obviously strong hidden hands were able to manage and gave rebound within same day and took care of it very well, that’s a big reality. Obviously the strong hands are the utmost reality and recessions and all horrors might be mostly just the story.

How much did you really know her? How much did you look? Who was she? Who was she when not with me?

How much do you really know about the economy and share market? If you feel too excited and rushed into fears and recession in your adrenaline, you may not know much yet.

I’m disappointed with so many well-known economists there. Many of them didn’t stress out imminent issue long before, but just point out the darkness of their opinions during the dark days. I think their hearts are blinded with their own darkness and to understand real financial situation, at least with economy or strong hands situation. Up until now, many there are still stubborn with dead cat bounce thesis, temporary bounce thesis, but never really allowing another side of story to appear. In a moment, they will disappear, those fears are now disappeared, just like a story, disappeared, just like that.

You think you want answers, but you don’t. Where is she? WHERE IS SHE?

You may want to know my answer. On May 1st 2022, I might emphasize safety measure, hedging, pain level management, etc. On May 22nd I also stressed out possibility that the madness might be all ended. However many didn’t want to hear that, simply because of conflict of interest, fears of darkness and fears of missing out. That’s OKAY but many out there should be allowed to have different opinion.

Larceny, bribery, murder. People love their secrets.

Of course every economist and player may have their own theories, secrets and strategies. It’s love stories of life. It’s true life of a sad story, at least 22 people within digital currency industry may have died, suicide from the rout of digital currencies, Terra, Luna, NFT and Bitcoin which could be the real culprit of the May 2022, rather the recession argument. I’ll speak more later about this since I may have some technical knowledge as well, rather than just their economy knowledge. We should love those technical and economy stories.

Don’t go down this path. Stay here in this life.

Around May 22nd, I’s back to my path. I might be still questioning of the widely discussed recession. I have my path came back nicely to highest about a week after and that’s all I need. I’ll continue my life journey to my fullness. I still expect commodity, energy, EV, EV commodities to shine and continue their journeys. They are still breaking high and fears suddenly are out of my mind completely, in which I should rather beware.

I’ve turned a blind eye to plenty. I have to do this.

Sometimes it’s very hard to explain how I looked into financial systems. Sometimes I have to close my eyes, ears and minds to many economists and news during the darkness. I do believe they should also start to consider other opinion or light at the end of the tunnel.

That machine of yours. How close can you get before the illusions broken

My formula predicted quite correctly/precisely to when it was started (May 1st) and predicted precisely when it’s about to end (May 22nd). How close can I get before my formula is becoming incorrect? I think it comes to availability of human experience to assist the autopilot of alpha and gamma, especially their inertia.

You are going on a journey. A journey through memory. All you have to do is follow my voice.

My financial strategy and experience have been going on a 22 years of journey, lots of memories have been crafted. All I have to do is following my own voice. Please be aware that this is my own personal opinion. It’s widely accepted to disagree and I could possibly be wrong obviously.

So what do I think about recession ending is? I think this reminiscence ending may well explain my opinion.

Mae: Tell me a story. Nick Bannister: A story? What kind of story? Mae: One with a happy ending. Nick Bannister: No such thing as a happy ending. All endings are sad. Especially if the story was happy. Mae: Then tell me a happy story, but end it in the middle.

At the moment, in my personal opinion, I will end everything in the middle. I will repeatedly replay my happy financial bullish, despite recession risk. I think the Fed and strong hands are still having their grip on the market well, and that is enough to minimize the recession risk on my side. I understood the risk is big and real. Due to raising market participant challenge, there’s no such thing as a happy ending in financial market. Their ending might be mostly sad, especially if their rally was very happy. I chose my own ending and other may choose their own way. I like to think that we both chose right for ourselves.

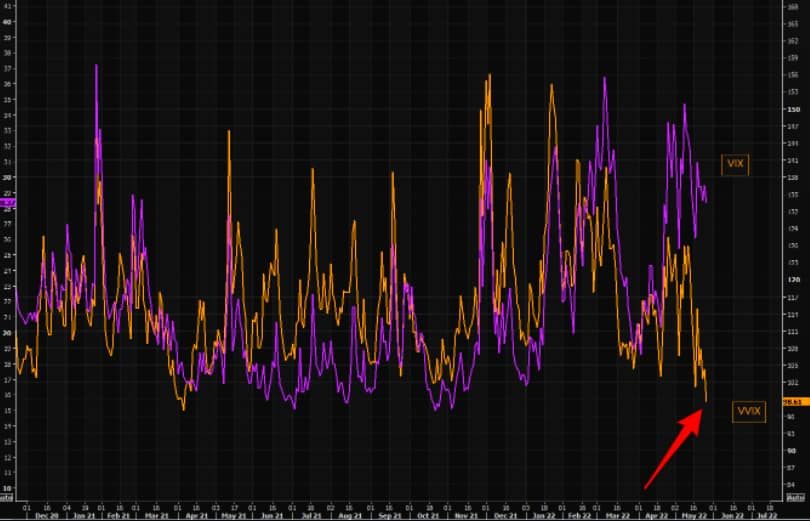

Courtesy of @themarketear

We do have VVIX pointing to lowest since 2020 despite elevated VIX. I would think it means, the risk or current high volatility is widely accepted by market participants. They are becoming more immune to fears and volatility. On the other hand, we should expect high volatility as our new normal, don’t get surprised with high volatility and expect high risk to remain (be careful with your pain level). Without that sadness, you can’t taste the sweet, all current bullish plays need higher volatility to live. We may choose our own ending, we crafted our own path and life, and no others should matter to step into other own path.

Any idea in this blog and website are my personal own. They are not financial advise.

What if you don’t understand what he saw? Then you better figure it out, because it was coming for you!

We don’t talk about Bruno, no, no, no! We don’t talk about Bruno…

There wasn’t a cloud in the sky No clouds allowed in the sky

Everything looked fine! No crisis was and is and will be allowed!

If we looked back at history, World Bank research, inflation fell sharply from 2008 to 2018 or for 10 years. “Inflation has declined sharply around the world since the global financial crisis. Global inflation—defined as median consumer price inflation among all countries—fell from 9.2 percent (year-on-year) in the second quarter of 2008 to 2.3 percent in the second quarter of 2018.” Let’s say average inflation prior to 2008 was half of it or 4.6%, the inflation fell down 2x.

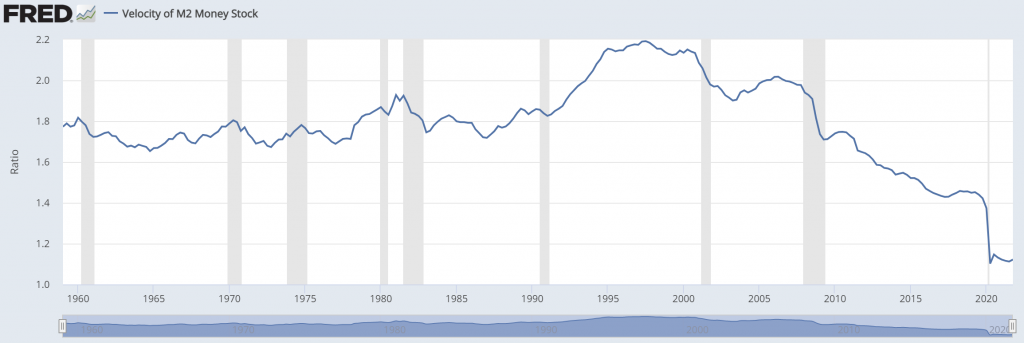

Fed balance sheet from 2008 to 2022 is nearly triple (3x) with significant increase from 2020.

People may argue money velocity has halfed (2x) with potential revert back to decade average of 1.7 (1x).

Something doesn’t add up. Inflation is way too low, even for today inflation. It’s either we have very much supportive liquidity (3x/2x to 3x) or inflation to catch up ( 2 x (1.5 to 3) = 3 to 6 ) or an artificial monetary. This is where Bruno came in. Please don’t talk about potential inflation of 4x or 250 bps rate raise, that’s simply impossible to afford without any kind of crisis terms, e.g. recession, stagflation, and any scary words!

Bruno walks in with a mischievous grin- Thunder!!

Grieving prophecies!

You telling this story, or am I? I’m sorry, mi vida, go on

Let’s go on. One of our simple proxy is energy. Even if we use lowest median range of 50$, not many could afford oil at 4x or ~200$, especially emerging countries. Oil at current 103$ is simply still way too cheap compared to past 10 years of wealth creation.

Economists already warned similar to my emerging data short thesis in year 2020.

Bruno says, “It looks like rain” Why did he tell us? In doing so, he floods my brain Abuela, get the umbrellas!

Which is great! Many big emerging economies are well prepared (China, India, and Asia). Emerging countries like Venezuela, Turkey, Russia, Sri Lanka, and Peru hyperinflation issues are well contained from global economies. India and China indeed are benefiting from deep discounted Russia commodities to save themselves. Let’s keep consequences of this like the sound of falling sand, ch-ch-ch.

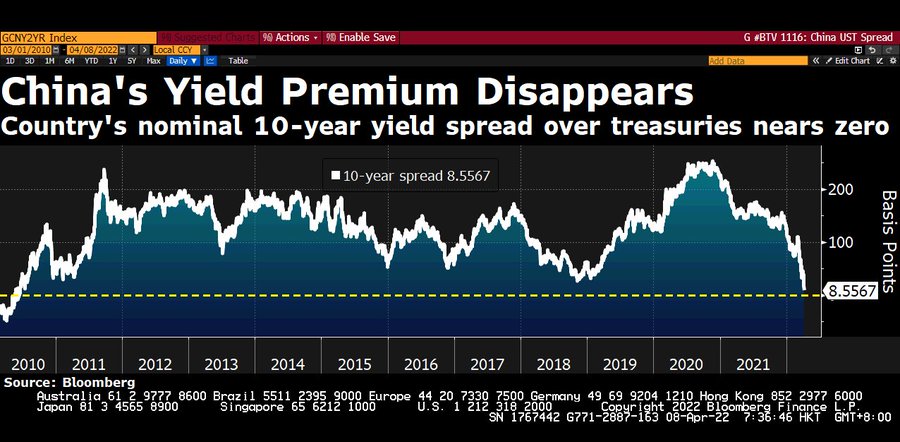

China premium disappears

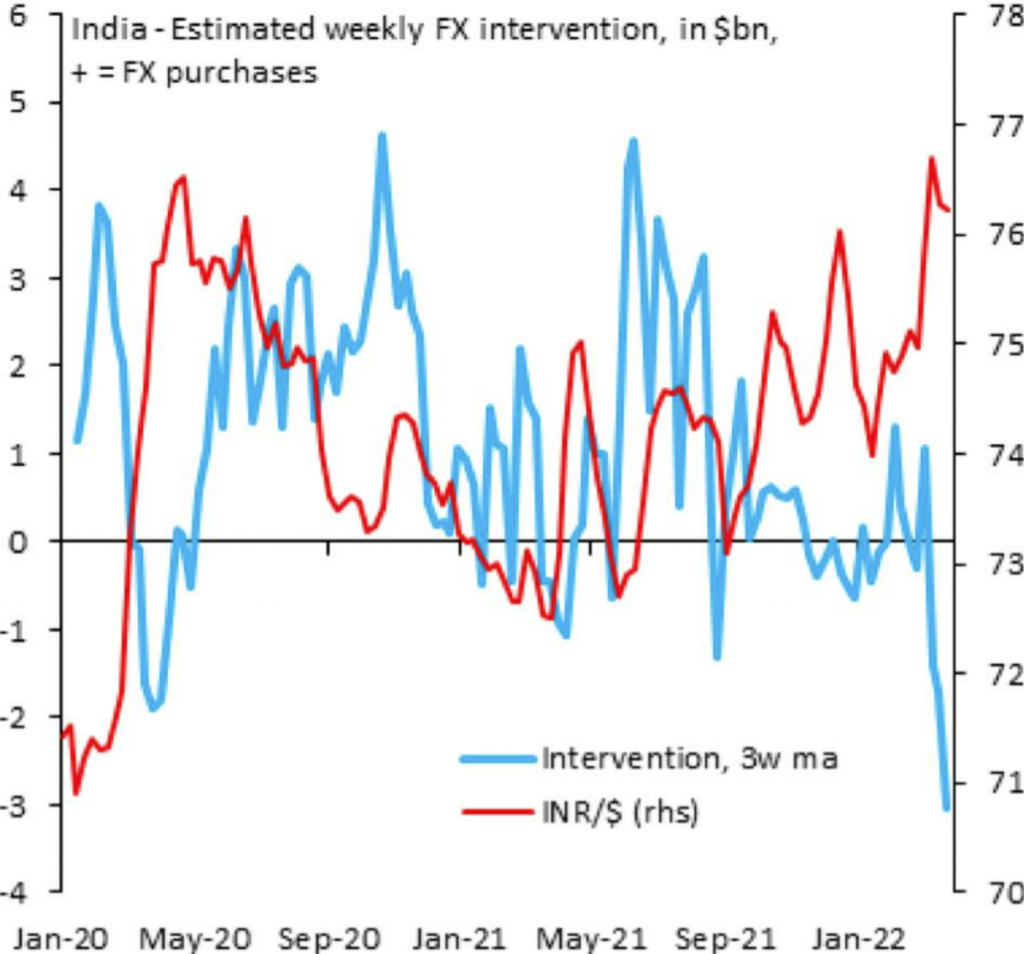

intervention

Grew to live in fear of Bruno stuttering or stumbling I could always hear him sort of muttering and mumbling I associate him with the sound of falling sand, ch-ch-ch

USA investment is near zero in SriLanka

Could it be anticipated? Yes it should, by normally raising rate following the curve. However Russia and powerful emerging market response, together with powerful US treasury refinancing interest themselves, all combined, brought into unprecedented Federal Reserve response from their already behind curve in September 2021, into much further behind curve in 2022, unless they start with an action that I will call later an artificial yield curve.

It’s a heavy lift, with a gift so humbling Always left Abuela and the family fumbling Grappling with prophecies they couldn’t understand Do you understand?

It’s powerful market response to challenge petrodollar or US reserve status that will only draw higher response from the mightiest Federal Reserve. China less interest to recycle their trades, UAE interest on holding their peg to dollar, China treats to their property and technology, are few other of things that will only drag this further down economies behind curve and delay darker prophecies few years back.

I’m fond of the Fed Guy, Joseph Wang. I mostly agree with his view but his negativity to equity. Since last year, I still believe my top picks (Energy, EV, EV materials, food, etc) will continue to be shinning stars this year. As we are already going through half year of it, I’m interested to use Joseph Wang The Great Steepening article which I think is simple yet has very strong message to tweak my strategy going forward. With recent Federal Reserve minutes to aggressively do QT (Quantitative Tightening) and rate raise at same time, I may have my own prophecies and strategy.

Courtesy of Joseph Wang, The Greatest Steepening

I think:

Foreign may continue to hold treasury at modest pace. My reasons are:

There’s less interest to park foreign reserve in USA due to event like Russia asset freeze.

Necessity and requirement to sync with greatest economies and avoid unnecessary disturbance.

Foreign has been holding most of the treasury.

With emerging countries are expected to juice their economy due to higher price, US Dollar is expected to continue to be strong, making the treasury less affordable to foreigners.

Treasury should be sold at cheaper price/discount. Therefore for sake of the USA assets interests, they should be firstly sold locally.

Federal Reserve is expected to reduce treasury holding. This should go to non Fed and unfortunately that means much less liquidity challenge to the market.

USA banks will be main driver here. In order to have this situation, we need to maintain 2y10y spread for local bankers.

Hedge fund should continue to seek higher return from yet strong economies and less interest to make loss to inflation.

He told me my fish would die The next day: dead! (No, no!) He told me I’d grow a gut! And just like he said… (no, no!) He said that all my hair would disappear, now look at my head (no, no! Hey!) Your fate is sealed when your prophecy is read!

Darkest fate might have been sealed well when their prophecies are read!

We should notice recently:

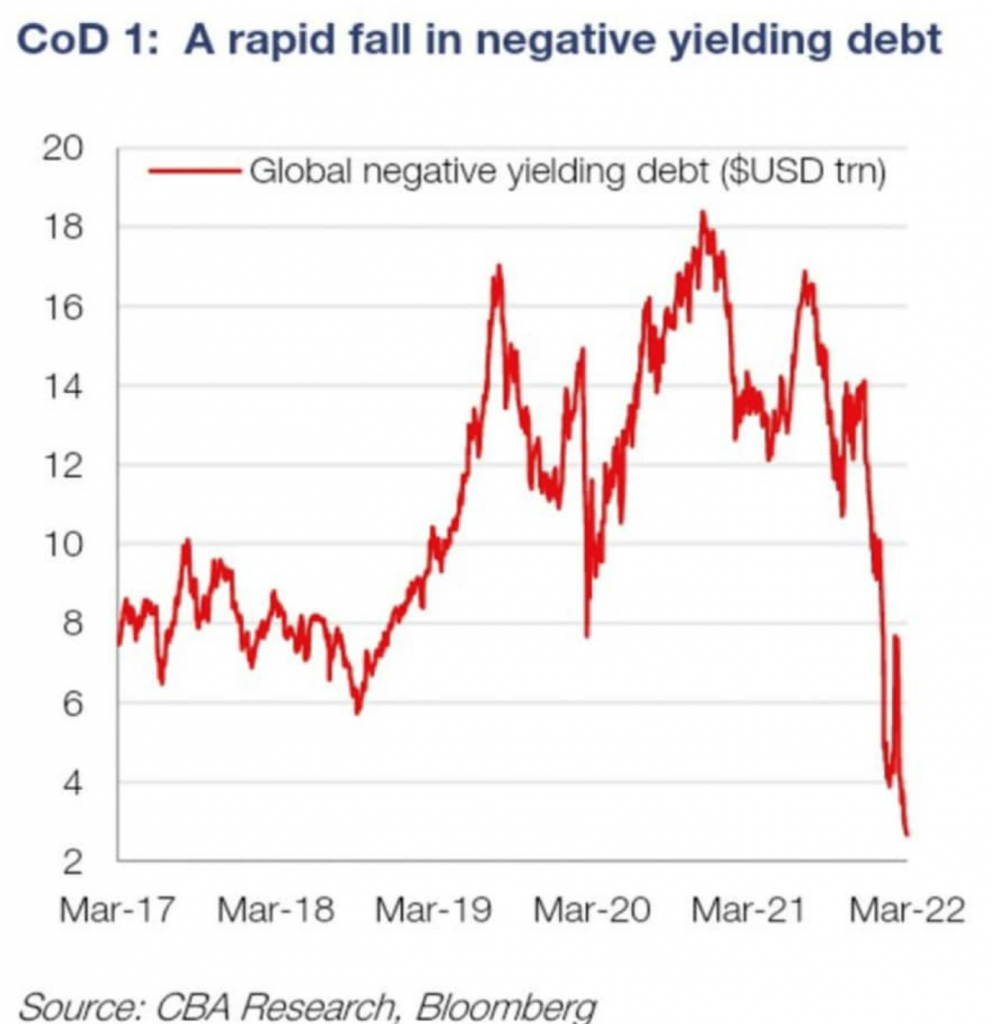

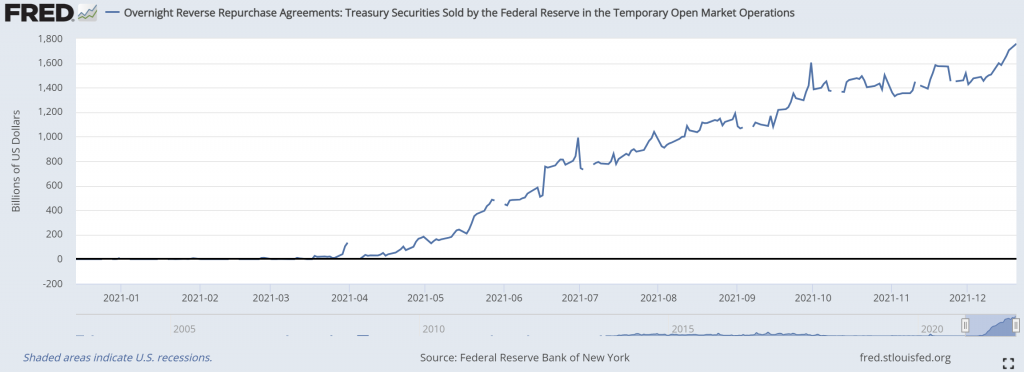

negative yield is drawn to zero, that’s about 14T$ in past 2 years.

RRP stays high at 1.6T but may be slowly withdrawn.

treasury and bond big sell-off like a dead fish!

dead fish of the century

BUT! We should notice despite the hilarious (for who don’t know historical effect of bond) bond sell-off:

Equity rebounds strongly!

GDP continues to grow.

Employment and economy numbers continue to raise.

Higher price should attract higher credit to run economies, especially in emerging economies.

Selected industry and commodities demand continue to be strong.

There is still a lot of opportunity for technology and EV (Electric Vehicle) to continue their evolution.

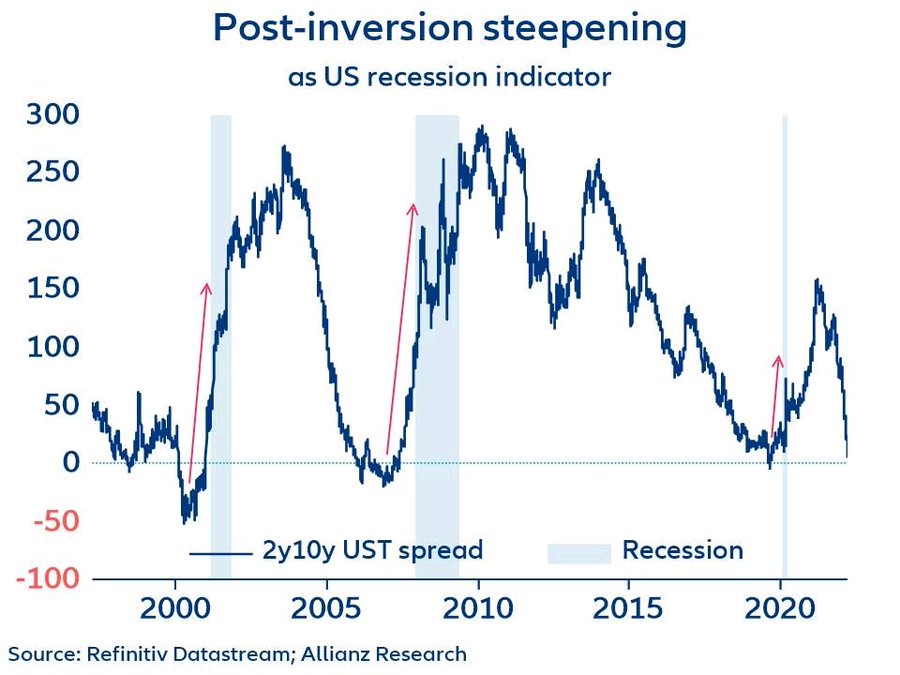

History shows recession may be seen after the steepening is back, not during lowest. This may give enough hedging strategy whether we will endure recession or banks loosing its value driven during this time.

Which tells me that the strongest hands actually haven’t lost their grip. Or in simple term, Bruno is actually telling his grievance with good intention, just like in his Encanto.

He told me that the life of my dreams would be promised, and someday be mine He told me that my power would grow, like the grapes that thrive on the vine

I will continue to hold strong my stellar charms, despite of liquidity risk crisis ahead and thrive!

He told me that the man of my dreams would be just out of reach Betrothed to another It’s like I hear him now

But I may reach my targets and goals sooner.

Hey sis, I want not a sound out of you !!!

In summary, my prophecies are:

Real economy numbers should continue to support strong economy growth, regardless of possible weak future numbers and challenge of liquidity crisis. I believe real economy is still working at discount to future and no clouds are allowed in the sky.

We may fear of monetary liquidity crisis with even greater challenge during fiscal supply (e.g. BBB – Build Back Better) after current refinancing is completed or during low inflation.

Long term yield should continue to raise higher, especially the 10y, artificially.

Belly and butterfly should continue offering attractive spread and growth, even though they may be artificially driven.

QT should run faster than its front end rate to maintain the artificial steepening of curve. To maintain steepening from running out of course, treasury refinance (1$-2T$ and another possible 2T$ of BBB) could sanitize steepening over effect.

Spread should continue to offer benefit to local bankers.

I still maintain my previous thesis of sustainable high inflation, inflation in long run to neutral rather than zero (hard landing).

Whilst there’s a probability that commodity is under pressure, it may still offer attractive dividend return from continuing profitable market operation (not from future numbers).

USD might continue to stay strong which may restrict foreigners from entering this artificial money distribution and may reduce capital carry trade outflow from the USA.

RRP should continue to decrease very slowly (or relatively flat) due to lower/sustainable high inflation. My important message is that it may continue to support financial market from sudden inflation drop or hidden fuel for a rally (yeah I know it might be a crazy idea).

Inflation is expected to drop/sustain at high (above mandate limit of 2%), like in my previous articles.

Let me introduce you, my own first thesis/study of possible first idea of artificial yield curve (currently available to my own internal only). Yeah I know, I have lots of proactive crazy ideas, but not to worry, we can always tweak/adapt along the way to follow market dynamic. This idea is not impossible with liquidity is currently at about 4x of real economy required liquidity (shown in first part of this article). As its consequences, it may spell trouble to those who are against this alliance. On the good side, it’s possible to break decades of grieving long term trend, without igniting crisis earlier, reflected in current strong real economy numbers (rather than current crazy future trade) and ample of liquidity. To avoid long term yield from running its course, treasury refinancing issuance should be able to sanitize/limit possible QT effect over run. It requires co-operation between monetary and fiscal in their best possible time to create and maintain the artificial yield curve and possibly avoid recession. Remember, participant response (based on past learning and economy theory) frequently rewrites history, therefore past performance never guarantees its future. But it’s in my vein/principal, money mostly does!

Um, Bruno… Yeah, about that Bruno… I really need to know about Bruno… Gimmie the truth and the whole truth, Bruno

Time for dinner!

Any idea in this blog and website are my personal own. They are not financial advise.

If you wanna run away with me, I (always) know a galaxy And I can take you for a ride I had a premonition that we fell into a rhythm Where the music don’t stop for life.

When I was young, I always have one question in my mind. If human created economy is a fair systems for any new born, why do farmers in emerging countries, after using all of their dearly life capabilities (physical and brain), and working so hard for rest of their dearly life, they earn lowest in the economy systems? I should have all of their economy problem dejavu printed in my DNA because I am one of their children. I have knowledge in agriculture innovation, technology innovation, as well as economy innovation. Should we use “work smarter” to justify status of 26 millions of poor farmer families in Indonesia? Or do we justify economy borders based on gender, language, wealth protection, race, and refusal to work hard?

The farmer produces food, one of critical elements in oldest day of human economy, prior to information technology, bio technology, defence technology and economy technology. Hundreds of years ago, human went to war, just to secure access to food. Before modern imperialism, even commodity as simple as salt and pepper was our global currency. I understand economy systems should evolve, like the Keynesian, but their basic evolution should emphasize democracy of human number, rather than democracy of money number, should we see human life is valued higher than the money or economy itself, to binocular geopolitical atrocity per se.

The farmer seems to live in different economy systems and socio economy population. To justify their social population grade, farmer in advanced countries are able to make difference. It should show that there are two issues in here: (1) job based population, and (2) emerging/advanced economies.

It is estimated 26 millions of poor farmer families in Indonesia

Famer family effort to have better life should drive socio path to urbanization, which is still one of China internal growth combustion engine. Even that so, it’s still a question to my mind, why white collar in advanced countries makes significant different to the emerging ones? Obviously emerging has different level of economies, compared to advanced ones. It might be related to wealth protection systems, financial weapon and their stability/less volatility/higher margin defence.

Back to farmer produce, it’s intriguing that one of our top picks, food, now becomes one of major elements that’s hard to control in today hot inflation. Capital is rushing to secure fertilizer sources in which they expect to generate double digit of return to next 10-50 years. Russia is also one of biggest fertilizer exporter. Obviously I should say, today inflation is different level of inflation we have seen in past 3 decades when sacred food has never been on our table. None thought centuries of effort to depress food price would be out of their genie bottle. Food is just one example of many following commodities. I should admit food can be one kind of nuclear weapon to destroy emerging economies. When stomach is empty in poor economies, human mind could easily go insane to riot. Premium to emerging business should also increase, together with their less margin in energy and commodities.

It’s very important to keep commodity muted for sake of our economy systems stability, until they break lose.Until this article is published, their (oil, metal, energy, etc) price increase hasn’t shown any indication to stop at all !

Tradingeconomics: chicago wheat price.

Fertilizer

GALAXY AND MY PERSONAL PREMONITION

Being adaptive with our galaxy to live in, is always interesting. One of our other top picks, energy, might be able to be define economy based country border between emerging and advanced ones or between advanced economy themselves (Europe vs USA, BOJ, Australia/Canada). In today economy, oil is still one of best proxy of energy, despite our effort to have lower rate of ESG.

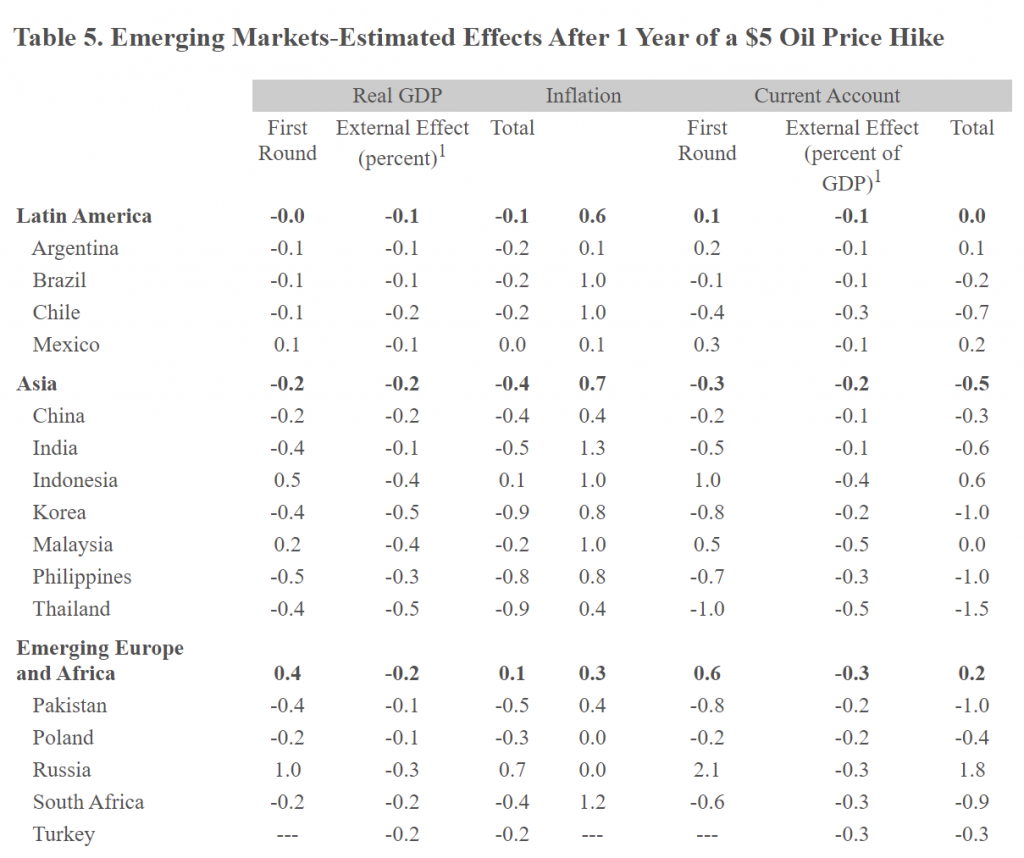

IMF research shows significant correlation between oil and country GDP. Energy is today one of most important basic needs of human. Information is mostly stored in energy, currency and their transaction are as well (evolution with digital coin). As seen below, every increase in energy price, will adversely affect emerging economies. Their current and trade account are mostly lower with every increase in energy and oil.

IMF research

I would then use commodity and inflation in general to proxy share market index performance between 3 countries, USA (centre of financial universe), Australia (commodity sensitive) and Indonesia (emerging market).

share performance from 3 different kinds of countries

Obviously, the USA, our world defence, should remain to be in the centre to have this correlation working. Based on this simple comparison table:

(1) Between 2008 and 2015, during GFC recovery, when money was sanitized well within financial systems, when inflation was relatively muted, emerging countries were able to run best, exceeding the USA. During this time, possibly afraid of the inflation, RBA took drastic currency strengthening causing AUDUSD to reach 1:1 in 2012. Missing inflation factor during this time, accompanied with expensive AUD caused Australia to perform worst. Many global business exited Australia, since AUD was simply too expensive with no inflation around.

(2) From 2015 to 2022, when inflation was just starting to pick up, Australia is showing increasing acceleration with USA is relatively muted/stable. It’s quite obvious that emerging is performing worst in inflationary environment, compared to Australia.

(3) Should index perform relatively same to next 2 years based on past 10 years performance, we may see incoming huge potential growth in Australia, compared to emerging countries. It may even run better than the USA. This might also be supported with my previous inflation arguments that the USA should let inflation run amok. That should benefit Australia A LOT!

Also already explained in previous articles:

(1) There’s no inflation in Australia with missing energy inflation in Australia, unlike other countries.

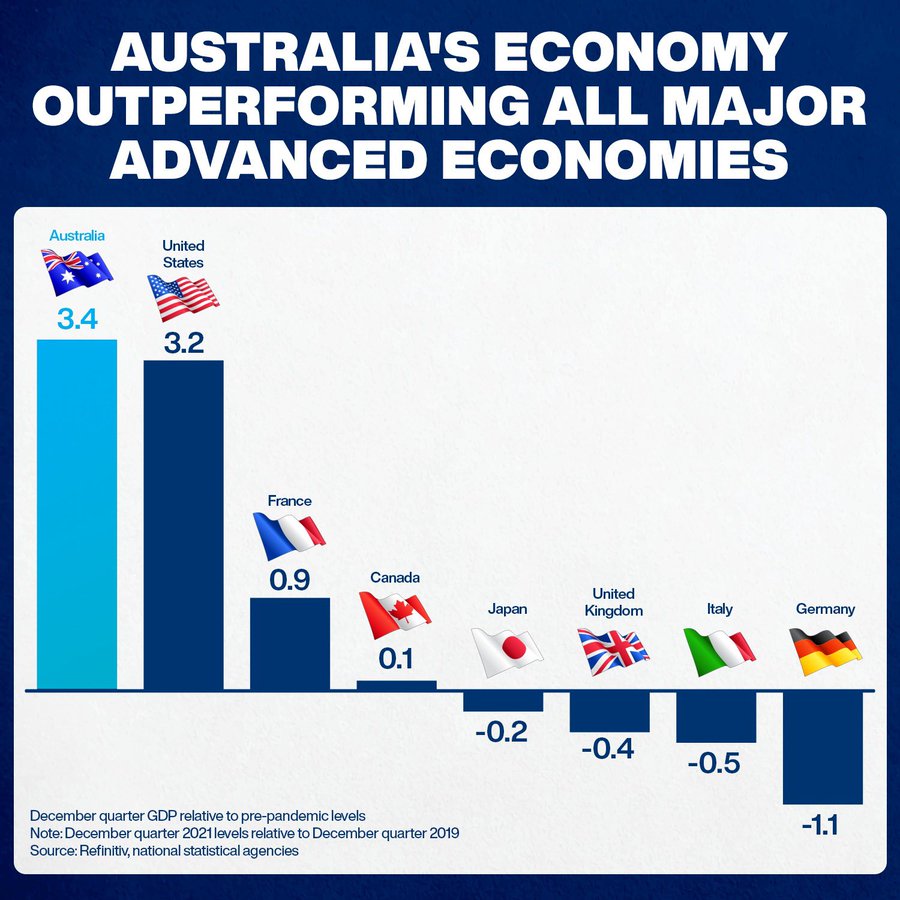

(2) Australia GDP is growing faster than the USA, relative to December 2019 quarter of CoVid pandemic.

(3) Australia seems to be much less impacted with geopolitical issues, comically should any nuclear dust theory ever possible explode on the earth.

(4) Australia is already performing better than emerging countries, even compared to USA, in regard to latest CoVid recovery, surprising me actually about Canada. Nevertheless, it might be due to commodity advantages.

This might lead to my other personal opinion to whether assets in Australia (e.g. property) is due to fall when RBA should start increasing their rate within this year? Personally, I doubt. In 2019 when Australia property fell to enter next level of inflation phase, I believed that property run in Australia shouldn’t end because inflation factor was not there yet. Interestingly, in 2019, I found property data was offering better potential return compared to its share market companion. At least it isolated most of my data from the CoVid infestation.

As explained in previous article, the centre of financial world, the USA, should continue to let inflation run high, unlike their past decade of monetary policy. With Russia as one of biggest energy and commodity suppliers taking world into energy and commodity scarcity, I think Australia growth should be very much supported.

Depending on how this global inflation could possibly evolve into destructive hyperinflation; as of today I would have same opinion with the Fed and Yellen that inflation should subside by end of year or next year. Don’t get me wrong, I highly doubt the Fed transitory inflation thesis last year. However market dynamic and my other internal research may support my thesis of sustainable high inflation this year. It doesn’t necessarily mean a drop in inflation. I believe inflation should remain high, but it should not reach level of the destructive manner (hyperinflation). Keeping our insanity to geopolitical risk, Russia movement in their card to drive hyperinflation might be much hyped. My simple argument is that Russia GDP with 125M population is equal to Australia GDP with only 25M population.

We should understand, sustainable high inflation may likely generate most optimum growth in economy. I could understand Mr. Biden frustration/difficulty to explain benefit of sustainable high inflation.

“Do you think inflation is a political liability going into the midterms?” Fox News White House correspondent Peter Doocy could be heard shouting as journalists filed out of the room.

“No, it’s a great asset,” Mr. Biden muttered sarcastically. “More inflation. What a stupid s** o* b****.”

Compared to other countries, Australia has historically preferred currency and property investment, with their famous franking credit and negative gearing systems. Their preference in currency almost stalled their economy in 2012, therefore I think they should learn from it much. We have CoVid pandemic still hanging around the economy. Geopolitics also adds uncertainty to the fragile economy. With more indication of reluctancy of RBA to increase rate (with excuse of missing energy factor), China threat, and opportunity to pick up energy and commodity greatest opportunity moment, I think it’s more appropriate for the RBA to support Australia economy growth and capture this life time economy growth opportunity, rather than to put the country muted again like they did in 2012.

It could probably be highest G-force in current financial market

Back to year 2019, many knew, I’d been overweighting my data greatly on property rather than equity, simply because reason of inflation factor wasn’t there. I was surprised with oversold in commodity currency therefore my data started with emerging short to commodity countries and hedged it to China.

#2020 correct rhythm – equity in general

In 2020, equity was performing well in general.

#2021 incorrect rhythm – China fall

China failed to maintain their property growth, mainly related to their offshore.

After running greatly between year 2020 and 2021, I would think it’s more appropriate to follow rhythm to normalize EV high valuation. I had to cut EUR data once the geopolitical issue was started. Simply the trades between EUR and Russia is too big to ignore (over 50%).

I got 3 out of 4 rhythms correct (75%) in past 2 years. Hopefully 75% is enough probability to justify my personal opinion about Australia.

RIDE – DON’T STOP FOR LIFE

With increasing AU10US10Y, we could have some supporting factors:

US rate expectation is way too high (7-9 rate hikes) while credit market is contracting,

US inflation is expected to stable,

USD is relatively overbought,

NASDAQ may continue to have pressure,

German Bund is going back negative which doesn’t seem to support spread to the Europe,

Japan may have geopolitical risk (Kuril island dispute),

China and Asia emerging risk due to energy and oil.

AU10Y – US10Y

We might be able to use this opportunity to leap our economy status high to next galaxy.

How far can a kangaroo jump?

Any idea in this blog and website are my personal own. They are not financial advise.

On an all time high We’ll take on the world and win So hold on tight, let the flight begin Meanwhile this song is playing in the background: ALL TIME HIGH

Did we hear Omicron was scarier and in fact infected much faster than years of Covid-19 influenza, despite mild symptom downplay?

one of most infectious influenza virus in human history

Surprise, not? After all of the influenza drama, we are on an all time high (ATH).

Our still most obvious sign is world excess money and inflation expectation is on all time high with staggering 1.8T per day. Back to our last month article, why do we need QE when in fact we have RRP bigger than the QE itself? We shouldn’t get confused with negative effect of TGA balance transfer during early adoption of RRP. If Omicron and Covid are currently human biggest threat, why there are instead many ATH on the run and Central Banks are tightening? Obviously it’s not virus taking care of our life, but probably my own money cycle thesis.

Excess money / Inflation expectation is ATH

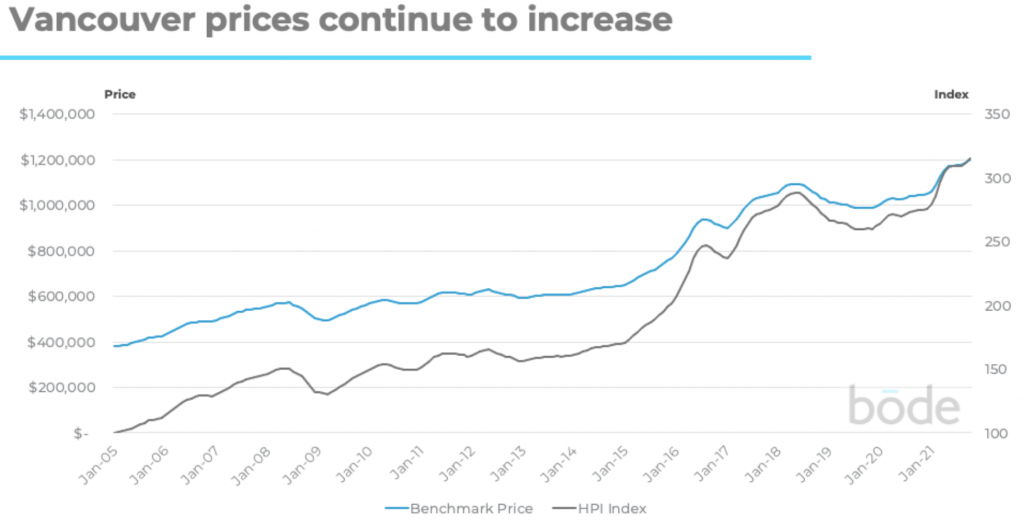

Vancouver property priceBRK.A broke higher high during Omicron release

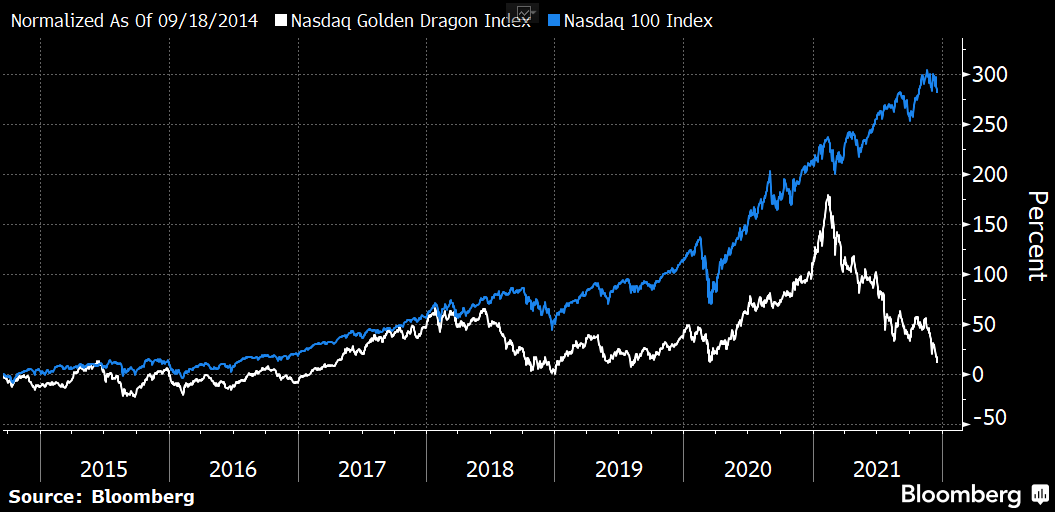

Following our last month thesis, when money/crowd is continuously ‘invested’ in FATANG, they should hedge with inflation protection assets. I would think current dynamic is twisted with recent China property drama, which widen spread between US and China/Emerging.

In my own economy model, in case of too big to fail, when there’s no money advantage, there is no need to have bankruptcy. For example, if Lehman Brothers (LEH) didn’t bring any advantage to bankrupt, I believe there’s no need for it to bankrupt. This economy model secrecy would become obvious, when being challenged with rising China power. If there’s no advantage to bankrupt China 2nd biggest property developer for now, I believe there’s no need for them to bankrupt their offshore liabilities. This is where money power would take hostage of their hegemony. Would there be any new money trying to step in on their way, they would throw this towel to them. I should still also believe, China would rather die, than directly bailing out their property developers.

During this cycle change, inaugurated with Omicron, FATANG heavy loaded trucks are rolling down hill with lower gear. They should induce heat, higher inflation, and increasing volatility. In my theory, when money is distributed within attractive discount opportunity, inflation should be ignited. There are two big players in here, trend followers and majority holders who will continue to support their own rally. Both of them at the end of day, should continue to invest in long run and try to reduce spread risk with other barometers. It’s no secret recipe, the success of FATANG was also due to liquidity. Indirectly few of them, QQQ, TQQQ and recent 5QQQ, are on all time high [leverage] ever.

Liquidity is the key.

lower geared FATANG sparks inflation heat

Recent cycle change seems to support FATANG de-risk effort which should induce global inflation instead. We heard Mr Musk was selling 15B$ worth of Tesla and paid 11B$ of tax. I would rather think from different approach, that it’s a great news! We should know that it’s coming from stock option, that rather be expired next year, is being used to provide more oil liquidity to Tesla truck (rather than negatively perceived company issuance), supporting US fiscal budget, and provide re-entry opportunity. During this de-risk event, inflation is usually in focus. Central banks and senators are mostly focusing on inflation, taper and increasing rate. Aren’t we surprised that some countries are taking opposite strategies? China is easing and cutting rate, and so do Australia, Europe and Canada. To ensure they could navigate this change, they should just need to provide abundant liquidity and market will navigate themselves beautifully. No surprise, we see beautiful XAU rally.

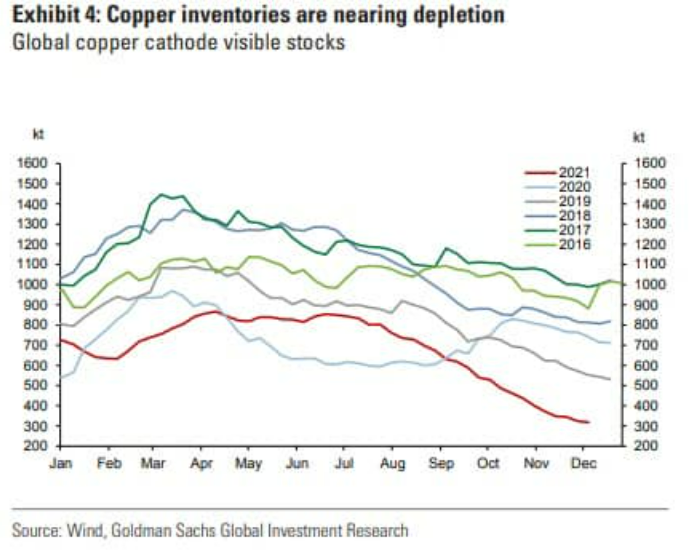

To hear most of FATANG and BTC, we should hear from Cathie Wood. She still believes that her innovation technology is within deep value territory. It’s no surprising that she finally admits of her poor performance, even though sadly, her view still doesn’t fit with my inflation related commodity rally and liquidity thesis. She should stick with her mojo, the EV, rather than selling it to small cap ones. Current check, my EV infra thesis seems still alive (together with food and electricity). Copper is still showing persistent strength and acute inventory problem in a decade. I think this should be more persistent than end of year Oil tax event Santa Claus rally.

copper inventories

To put myself on market feet, I would think the idea to attract risk should be to provide attractive discount to previous rally, where most market calculators were still based on previous historical numbers, rather than current dynamic value proposition. In doing so, they shouldn’t give too much discount and must avoid crash to the market, because that would rather be destructive and push market back to risk off side. Therefore in my own thesis, to attract risk taker, market should:

give enough opportunity, while maintaining current trend,

create fiscal opportunity with government guarantee to lower risk, and

have manageable inflation with faster tightening above expectation.

I don’t think the first two would be an issue. The market currently worries more with manageable inflation, whether Fed is behind the curve or not, seeing current probability of dot plot and drop in long term bond yield.

drop in long term yield question

However in my own imaginary theory, this drop should be no different than common QE front running. They front run long term yield, before RRP is returning to their native asset, while at same time, they reduce probability of market to not taking more risk.

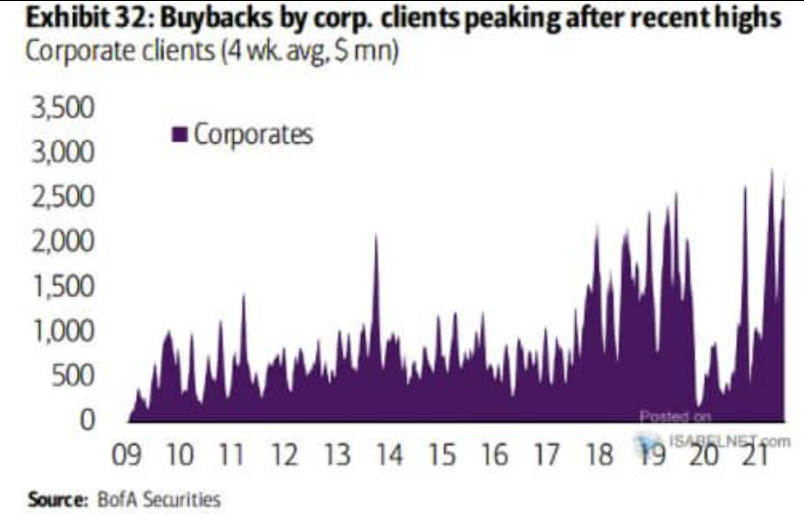

At the end, I would be excited to see more Corporate buy back, which I would think is rather a good opportunity to later escape and navigate finance world better.

Corporate buy back

If you believe in yourself, in your own long term growth, you should purchase back your own debt, or leverage up your own promise. I think that would be best strategy to navigate risk, de-risking your current high risk after easing rally, while at same time, taking advantage of the risk itself.

I would consider this as part of my escape plan to continuously run All Time High in long run.

Disclaimer: opinion is my own and never become any financial advise.

Many years, investors and traders have been trying to find and formulate their holy grail techniques. Most of them are failed and it’s not surprising. It’s market participants behaviors that are always trying to take advantages from those who are trying to find it. However I still find a dynamic adaptive learning to follow market participants is still doing well, rather than sets of quantitative formula or trying to redo past experience.

Since 2009, central bank balance sheet has been growing tremendously in a binary pattern. I always argued that we are not required to do any normalization yet until there’s any sign of global inflation. We were worry about US inflation in 2016, but at the end, US has to give up their inflation to bigger slow down of global growth.

In any of those events, our main concern is always about uneven money distribution which is related heavily to high grade investment vehicles supply issue. We see high quality bonds is getting scarce and drove their price to unprecedented negative yield. When we see junk bonds are being elevated too, people start to worry. There’s not enough supply for high quality vehicles which then raised another opportunity for their longer term. Companies also widely do buy back in effort to reduce their supply and cause unprecedented very high PER (Price to Earning Ratio). Funds may get more concern about what i called “new elevated normal” and due to their anchor to previous lower PER, they leave. If sufficient permanent balance sheet keeps permanent, as they are, this high PER could be the new normal, rather than previous failed effort to normalize it down. Isn’t it the behavior of economy policy makers?

We shouldn’t be surprised that ascending triangle of US shares, supported by Federal Reserve should be a conducive environment for them to continue up rising. Also if we looked our history, flat curve can cause rally as well, just like in 2002-2004. Did we just worry about US recession recently? I can tell that the recession is now officially gone in which I already predicted few months ago, as long as central bank remains supportive. Isn’t it amazing that money (rate cut and continuous 160B$ injection) can turn recession away, just like that? The impact should, of course, happen to US share market before it spills into other economy since US is still doing better than rest of world. We can see very clear that significant US 2y steepening makes their banks on right spot. Other countries like Australia big banks are now starting to raise their CET1 and Basel III, to possibly get their engine ready and catch up.

If we look Australian property market, after GFC 2008, actually Sydney property and many emerging property had been doing well. The GFC had caused people to panicky do saving and it caused these property market very healthy, which then caused rally from 2012 to 2015. This boom of profit margin attracted many developers (including from other states) to build Sydney and caused oversupply. It’s Sydney which has oversupply issue. Similar to money effort to save current risk to the jewel of US economy (IT industry) this year, there should be same effort to save Sydney property and I believe it will unevenly spill into other states which are not oversupplied, such as Victoria, with their tier-1 Melbourne CBD. With continuous effort to choke developer funding, it may evenly cause unevenly under-supply. It’s not difficult to measure number of cranes with our own little eyes.

China on the other side, was entering crisis in 2015 and may start to recover in 2020 ( 5 years ). It might be similar to pattern of US recovery from 2009 to 2014 ( 5 years ). Those are relatively matched with average length of maturity of their bonds. If it’s, inflation might start to happen in next couple years and people with negative yield may start to worry. US and China may really need to cooperate and introduce fiscal initiative. Powell said there might be a positive path towards negotiation. However we might interpret this as an opportunity for US to front run other world, rather than trade war deal. There’s still an effort to introduce #bluedotnetwork, an initiative from US Australia and Japan to challenge China BRI.

Other sign of inflation, may also be seen from recent plan of Aramco IPO. There’s an argument that the IPO might change the structure of Saudi people subsidy to rather fund their kingdom and US fiscal/global initiatives. Those masterminds behind the IPO are world rulers and leaders. They can decide market behaviors. My holy grail is to learn and follow their behaviors, the money.

Another sign of inflation is correction of negative yield bond rally in August which might cause short term funding issue. Eventhough the correction pattern may complete, it clearly shows that there was a pause in rally or having some structural change. It may continue to rally in medium term since it’s still above 2018 average, but it could also lead to global inflation. Christine Lagarde will take helmet of ECB (where most negative yield is) and she seems to be more fiscal supporter, unlike her predecessor.

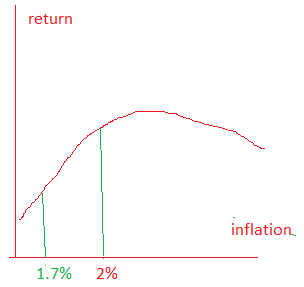

Let’s have a look from RBA speech today. In past few years, RBA has been hard to maintain inflation to their mandate of 2% due to slow global growth, trade war and China efforts to combat their economy slow growth issue. The achievement from 2015 to 2018 were mostly only due to lower currency. If currency didn’t fall, we might not have much luck.

The recent inflation data were broadly as expected, with headline inflation at 1.7 per cent over the year to the September quarter. The central scenario remains for inflation to pick up, but to do so only gradually. In both headline and underlying terms, inflation is expected to be close to 2 per cent in 2020 and 2021.

We don’t need holy grail to save the economy. The yield curve clearly shows, we just need to push up their belly and all kind of recessions and gloomy doom outlook could magically be gone. We know well, fiscal initiatives can help to push belly up (property), probably after pushing banks healthiness, supported by RBA with keeping rate lower than the market. Don’t be surprised with recent gloomy outlook from RBA to justify lower rate longer. Spring has really sprung, Australia banks are now reducing their dividend payment to grow. Just like natural cycle, flowers stop blooming after spring, they started to grow leaves and root. It’s a significant change to their previous years of high dividend. We hope this summer inflation is not that hot and return can be at their optimum.

We might not need to worry about lower volume of Australia property transaction/auction. I believe most of the low volume is because all big banks are now lowering their risk with some actions such as abandoning any Interest Only (IO). In the event of preparation to grow, this situation might be well perceived as an effort to increase healthiness. In 3 years, all IO will be gone massively from banks balance sheet and borrowers are already enforced to put more equity through Principal and Interest (P&I). Any weak hand will be funded with lower rate. Isn’t it healthy? I hope so.

We might not know when inflation start to bite. I will worry to non conforming lenders who are trying to expand their market share and being exposed to high risk borrower profile. I would advise their borrowers to monitor carefully their non conforming lender loans, probably in next 3-5 years.

Please be very aware, I may already have significant position written in this article. It definitely has conflict with my interests. Therefore this article is not in any case of financial advise.

Season may change, but its behavior should remain same.

spring has sprung

We might hear that Australia property may have been rebounded from its correction. My big question is not whether it is rebounding or not, but should investors keep investing in Australia property? If we consider price has been corrected after long decades of bull run, do we see any correction sign other than their price in AUD? I don’t. I would have to use my argument from 5 years ago, that if Australia property would start to turn, Australia was still having big saving from its strong currency, reaching as high as 1.1 to USD.

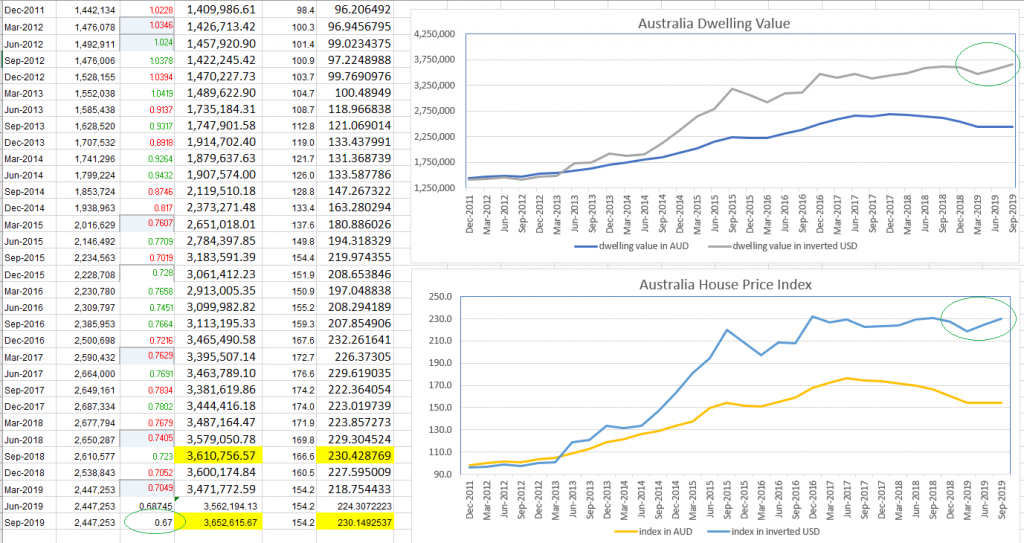

Below is some numbers from few weeks ago. Property price index and dwelling value in inverted USD are not showing any correction, indeed dwelling value reached higher high. It’s quite clear that when AUDUSD was at its lowest few weeks ago, 0.67, the dwelling value and median price are still trying to deflect deflation gravity after big run from 2009 to 2015, significantly seen near to 2015 when AUD was starting to fall. Using this view, I still don’t see any correction in Australia property. It’s no surprising that RBA and APRA put break between 2015 to 2018 to avoid inflation and were still trying to help in 2019, simply because they are still able to help. Correction in local currency is recently near to 15% and it’s too close to a sacred 20%.

source: ABS (Australia Bureau of Statistics)

Why do I think inverted USD is very important? It’s because global property is still increasing. There’s no particular reason Australia and Canada should undergo correction, other than they are exposed to commodity price, their main foreign income.

It may also explain why property price across Australia had correction between 2017-2019 after increasing uncertainty due to significant drop in currency in 2015-2017 due to commodity correction (Australia is sensitive to commodity price). In order to maintain this inverted trend, RBA should maintain currency competitiveness and it’s proven with 2 more rate cuts. When knife is falling, we would just need to wait until it drops on the floor, wouldn’t we?

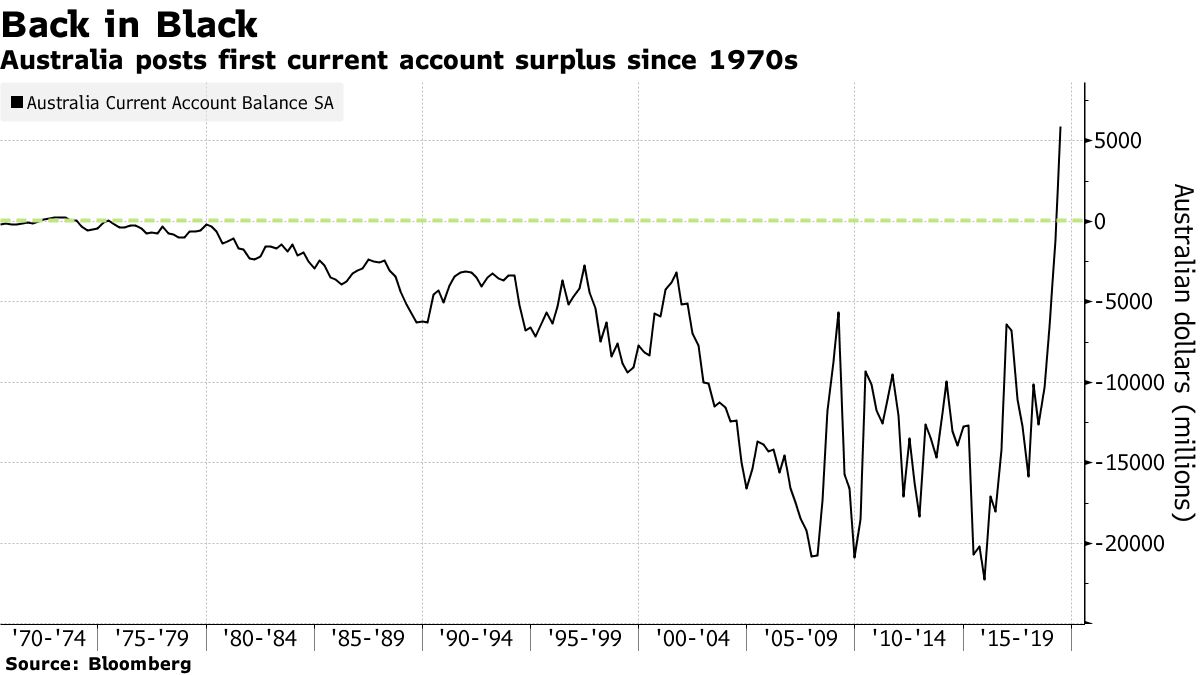

One of very obvious signs that the knife has fallen down, is Australia current account surplus. Australia indeed records significant current account surplus when commodity had a hit from recent inflation and yield crash. It’s no surprising. AUD has been discounted more than 30% in 4 years. It should bring attention to foreigners and start to raise capital inflow.

How do we compare Australia to HongKong which can be a benchmark of China property to global property? HongKong property price continues to increase and they are pegged to USD. I won’t be surprised that HKMA may have been interested with many tier-1 properties like in Wynyard and Barangaroo. These properties which Australian think is most expensive, is now 70% cheaper (=30%[HK property appreciation]+30%[AUDUSD]+10%[local panic]) for HKMA.

Just like countries who experience crisis (Australia with commodity crisis in 2015 following with tightening in lending), local might feel housing price is very expensive in 2017-2018. However it’s actually getting cheaper to the eyes of increasing global properties. This wound will heal when policies untighten their tight lending, following with global economy bailout, possibly from 2019. If my above theory is true, as long as global properties continue to increase and local policies support lending, I may expect Australia property price to reach at least 20% above their highest high in 2017.

It’s almost impossible to change how nature will behave. However I quite believe something is about to spring. I would have to rely on my theory that normalization couldn’t work beautifully yet. When season is to back easing, we should expect same behavior. Spring water should start flowing from their resource into their monopoly of banks/finance. We shouldn’t be surprised that big 4 banks, CBA, WBC, NAB, and ANZ may have sprung well. My learning machines keep alerting me from couple months ago. This sign is now quite obvious to disclose, after I see recent bounce back in Australia inverted yield.

It might be a bit clear now that some non-bank lenders are trying to capture some market share to next 2 years with some low rate funding. We could see from 2 years fix rate competition among lenders.

At the same time, even though clearance rate jumps, its volume is still quite low. Real estate agents are now trying to invite sellers to participate. I may think low volume is because sellers don’t want to sell at current low price and expect higher. If that happens, it may show that market is quite strong and not in panic yet.

a leaflet from a real estate agent

At the end, it may give few years of opportunity to unload during predicted good economy. We haven’t seen global pro-growth initiatives yet but Australia has started quite big infrastructure spending. Without pro-growth initiatives, it’s almost impossible to transfer asset to risk market and negative yield may be here to stay a bit longer. It means Australia may be one of many which leads pro-growth and risk asset cycle.

I may already have interest/position in this article, therefore it’s not in any case of financial advise.

Money is used to balance risk, spur economy, and encourage people to create value. It was good in the beginning until it began to cannibalize their own economy ecosystems. This is a story of a fallen angel.

Four years ago, we used to hear normalization but I always argue that normalization will not work well. It’s very obvious from the amount of changes in credit/money and world balance which is in a form of a binary. It may work in long term if all policies support beautiful normalization but unfortunately they don’t.

If we look at monetary side, monetary policies have been long introducing opium/easing to the market and now they have to fight the worst of their opium war. The bubble is now getting out of control. Indeed the greatest central bank, the Fed, may now have to surrender to market hostage. One of market that I’ve been closely watching most in past 4 years is down under, Australia. It’s easing more, its currency suffers most, thus it’s when share index is performing best, as usual. This year, it could be getting difficult since currency is already worst and housing recovery is near to their crash point, demanding more opium. It’s also not surprising that recent trade war outweighs since most of Australia economy surplus, both trades and account, is related to China. Accidentally this story may be similar and related to the story of opium war in HongKong, how the country began.

Fiscal policies, who should be our savior, is now becoming more politic supporter, rather than economy. Economy theory was rooted back from western/democratic economy, and it was valid until their economy got a bigger challenge. Policies were supposed to protect wealth, where rich is always growing richer. It’s until they are too powerful than the system itself and now start to re-engineering these systems for their own interests. Money always has a target to create an opportunity by any means. It’s when the angel is fallen.

Your heart became proud on account of your beauty, and you corrupted your wisdom because of your splendor. So I threw you to the earth; I made a spectacle of you before kings. Ezekiel 28:17

It successfully attacked Russian billionaires in Greece and now is targeting billionaires money from China in HongKong. HongKong is a very complex systems with its currency anchored to USD, complex China political influential through business, complex switch from export into service, and political issue from who will continue to support their foreign exchange reserve. The angel sees this opportunity, and now will do anything to monetize the opportunity, even at cost of human lives for his own desires.

source: wikipedia

Lucifer became so impressed with his own beauty, intelligence, power, and position that he began to desire for himself the honor and glory that belonged to God alone. This pride represents the actual beginning of sin in the universe—preceding the fall of the human Adam by an indeterminate time.

Dr. Ron RhodesReasoning from the Scriptures Ministries

Economy is evolving and it may need central bank to introduce market shock and dramatic approach to pop the bubble before it’s too late. The market knows central bank is always taking action based on history and will not risk stability, even for a temporary pain. It’s for sake of GDP growth which should never be negative/see a recession.

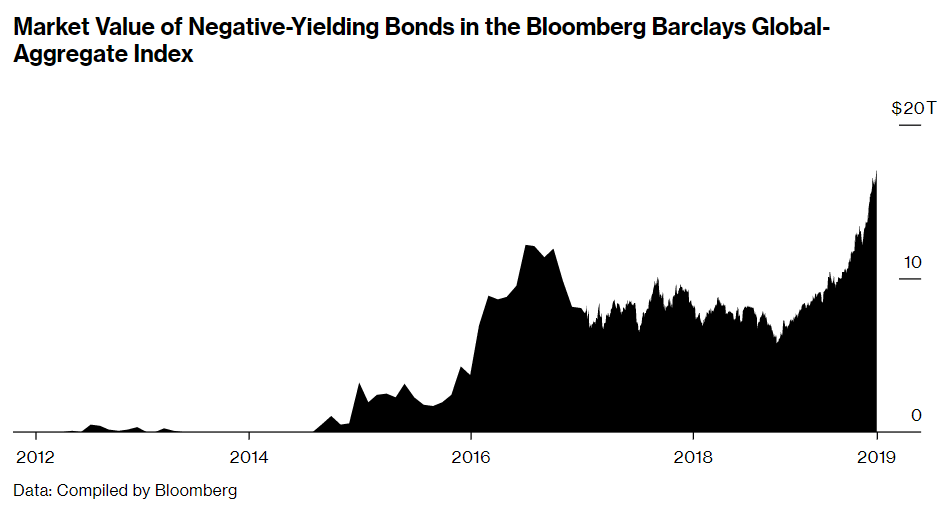

I see one of greatest bubbles in history in making. It’s negative yield which is now about 16 T$ and I believe it’s now out of control. Some countries are even growing worst, offering negative yield for their mortgage. Four months ago, we’ve been discussing potential rally/bubble from this and it seems to be true. During that time, I believed that the best time to switch into fixed income vehicle was not when yield curve was inverted (about a year ago) but when central banks around the world were starting to bow into market (Q1 2019) and they started to ease. I believe it should trigger market perception that central bank has less power to control and should be a sign of more inversion and negative yield rally.

source: bloomberg

In facts, all bond holders in almost every developed countries are now enjoying enormous return, as much as over 100% return, mostly from their long term maturity. A vehicle that has lowest risk should return lowest. However this vehicle is now returning relatively highest return at lowest risk. It defies economy theory books unless we agree with me that it’s all right to be wrong. Any significant movement should mean something, either fear or greed at same time. Austria 100 years bond returns 200% and we can see as well in many major developed countries. It’s no surprise that US is considering ultra long bond and it may trigger more rush into this bubble. It’s always be in my theories that those vehicles that are protected from most public access, would always have higher chance to enjoy bubble or great return.

In my opinion, the only way to revert the yield is either a drastic monetary cut rate/easing or introducing massive pro growth fiscal initiatives. For central bank, it’s a dilemma. It’s too late! It’s out of control! If they ease more, it basically tells the market they bow to market and loose the opium war. Central bank is now pouring gasoline into fire and expect the fire to distinguish sooner. At the same time, greedy smart money keeps pouring on into negative yields and might push this catastrophe bubble even higher. If central banks don’t ease, credit flow in banking systems will start to revert back from long term into shorter maturity and reducing amount of credit along the time. Even worst, at the moment, I think most of central banks are still behind curve. Market is no longer expecting Fed to cut 1 basis point but 3 or 4. As well as other countries, market is now expecting immediate 1 or 2 basis points of cut.

Where are the pro-growth initiatives? I would think pro-growth initiatives are being delayed until there is a deal from the trade war. We have been expecting these since 3 years ago but they never happen. We should see this as an indicator of what fiscal teams really have in their mind. Trump can save the world but I believe he prefers to win the war. The old decades of money recycle has stopped since 2008 and there’s no new deal until today on how to recycle back. I would think they should take HongKong as a hostage. I believe they will win, not because of making more, but making less loss.

After all, I would expect to wait for below signals while continue to ride negative yield related vehicles:

pro-growth initiatives,

inflation to crawl back, may be from next year,

bubble pop in negative yield and fixed income,

a peaceful world,

before I see a small scale of financial crisis with a possible recession to create a new opportunity. It’s rhetoric to say that a peaceful world could bring a short term pain for better future.

“After the war, the bubble should pop and I will begin to desire for a new opportunity.“

It’s my own opinion and not in any case of financial advise.

see no evil, hear no evil, talk no evil, and do no evil

Economy is a protection of wealthy. It’s always be mysterious, otherwise it won’t work. We might sometimes need to see no market, hear no market, talk no market and do no market. It’s true, market and communication have been long used to make money and protect the wealth. The only way to know the real market is using math, because 1+1 is still 2. No surprise that technical is still playing well, until a strong hand does poison it to monetize and protect their interests.

Recently we should be surprised that central banks outside US, have been orchestrating easing. They are who are US allies. Can we see the evil here? Can we hear the evil here? Can we talk the evil here? Or can we do the evil here? No matter why yield is inverted, let the issue stay here.

Greece, land of Russians billionaires to park their money, fell down a decade ago. Italy and other PIGS who try to save it, are still enduring longest economic depression, longer than US depression in 1929. It’s the cost of austerity where Greece central bank is unable to supply Euro, which is under monopoly of ECB, which is under influence of bigger shark.

HongKong, land of Chinese billionaires is starting to shake when China tries to put extradition law to this biggest tunnel of money out flow from China. Could it be part of global yield inversion? I see HongKong has one main big issue. It pegs its currency to USD while it should go together with other countries to depreciate against USD. Similar to Greece, HongKong is highly dependent to US and its USD. What do billionaires in HongKong think about their money in such extreme high risk when this country can go bankrupt at any time? Eerie is everywhere and exit door is too small.

Who is going to bail out HongKong? US or China? If they go to China, people may get instructed to riot. If they go to US, they can easily get overpowered by Chinese army. HongKong issue seems to already spread into Singapore economy and two of them dictate premium property in Asia. Does it scare RBA enough? RBA rate cut is showing how they respond to risk of biggest surplus of Australia, which is coming from China, both in trade and account. It could stem into overdue Asia Pacific correction since 1997, when I self-experienced scary social unrest and first time I did deep study of GFC to many different business views. It was due to company debts bubble and could now be property and government debts bubble, through trade war, currency, and policy changes.

There should be no safer place to park your money unless you pay for its safety. Negative yield everyone? Trump always emphasizes that US won’t protect anyone money unless they pay or would US have such an ability to make more money unless everyone pays? Monopoly tends to work well.

Of course this issue is much complicated than what we ordinary can see. At the end, we are just market opportunist who is trying to follow where those money is moving. We do not need to see who is that evil, or hear that evil. We do not need to talk about that evil nor do the evil too. I think global money is starting to morph into something new and I would be just following money using my own money theories.

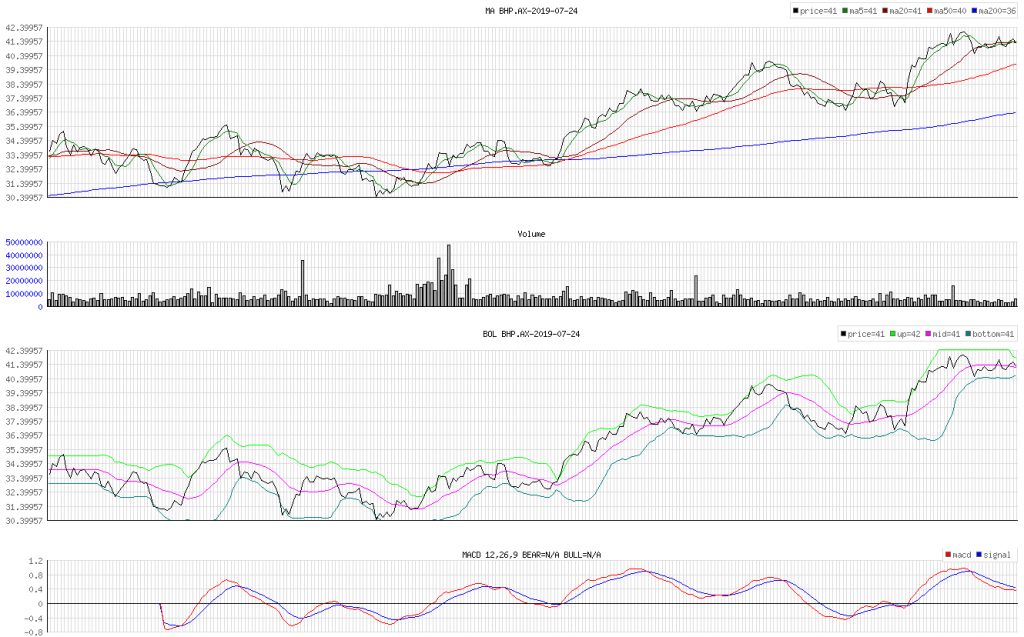

It leads me to classic technical play. An example of technical play is below. We did know well why we were doing big short to this company in May 2018. It broke both fundamentals (loosing arm of Veritas and Verisign, attacked by Google, long contract cheats, high debt, etc) and bad technical. We recently hear so many drama and mysteries, but seeing technical below in few seconds is enough to answer our curiosity, about what will happen to this company. There’s a Geisha make up by activists. Fundamental may not go better soon but activist play may draw stock price.

source: marketwatch

Another example, we do not need to hear any recent good news about fundamental of this company as well. We just need to know that easing is on play. It may not be favorable in short term but long term play should be strong enough. Who can win against central bank monopoly of their currency? Let traders try and we will do play with both of them.

source: my own calculator

I am a fan of any play and behavior of market participants, but recently the 4 wise monkeys inspires me much to overweight technical. When we can’t see in dark, don’t forget to always turn on the light.

I may have personal interest in any part of my article, therefore it’s not in any case of financial advise.

What you see/hear/do here and when you leave here, let it stay here.

{kind=link}