Based on an unbelievable true story, America achieves remarkable economic growth during a period of global tightening of the US dollar. This favourable situation/story should be safeguarded at any expense, while also ensuring a smooth landing for intelligent financial investments.

We have welcomed over 80% of fund allocation to America since the beginning of the year, based on our thesis. Our belief was that America would achieve exceptional success with a peak in interest rates, causing global currency to tighten and creating a strong demand for USD to fuel economic growth. This thesis is based one of our foundational money principles.

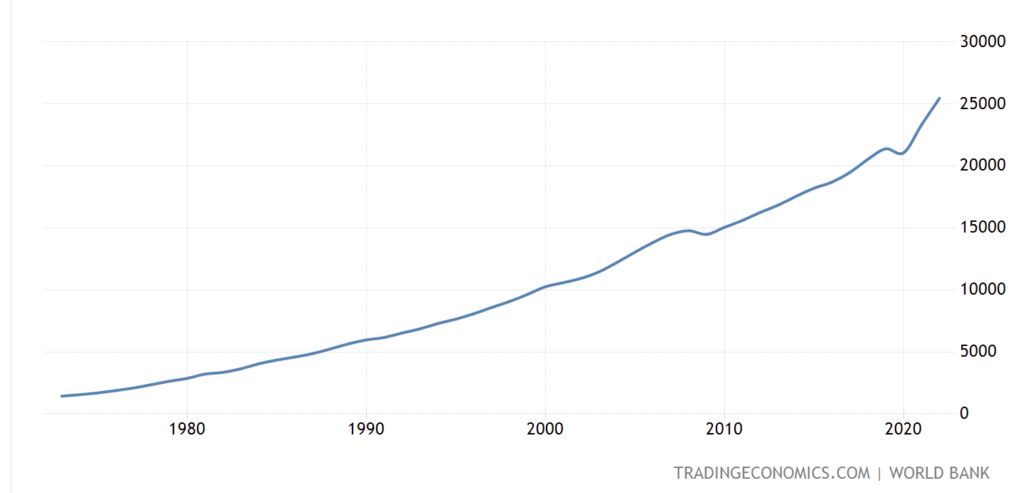

Firstly, let’s examine the growth of GDP. The US GDP is currently expanding at an unprecedented rate. According to our theory, this is a highly valuable asset that must be safeguarded at any expense, disregarding any other conflicting economic indicators. This is especially crucial considering the presence of smart money that has become trapped within the US economy, which we will discuss further later on.

It is not surprising that over the past few decades, the US had experienced a shift from a predominantly industrial and manufacturing-based economy to one focused on services and finance, with a significant portion of manufacturing activities being outsourced to China. However, since 2022, there has been a substantial resurgence in manufacturing and industrial activity, particularly in sectors related to sustainable energy and artificial intelligence, such as electric vehicle (EV) manufacturing, EV infrastructure development, battery production, and computing chips. These industries have received substantial support from the US government and are showing strong growth, which should be sustained and protected at all costs.

As we have previously highlighted in our articles, these sectors have the potential to generate a new economic capacity exceeding 10 trillion US dollars.

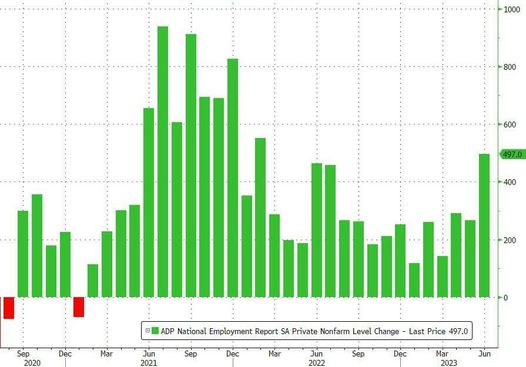

While the manufacturing and industrial sectors may not directly lead to job growth, the substantial government support they receive, particularly in terms of financial investments, has had a positive impact on job openings in other sectors. This support has helped boost employment opportunities in industries such as hospitality, finance, and services.

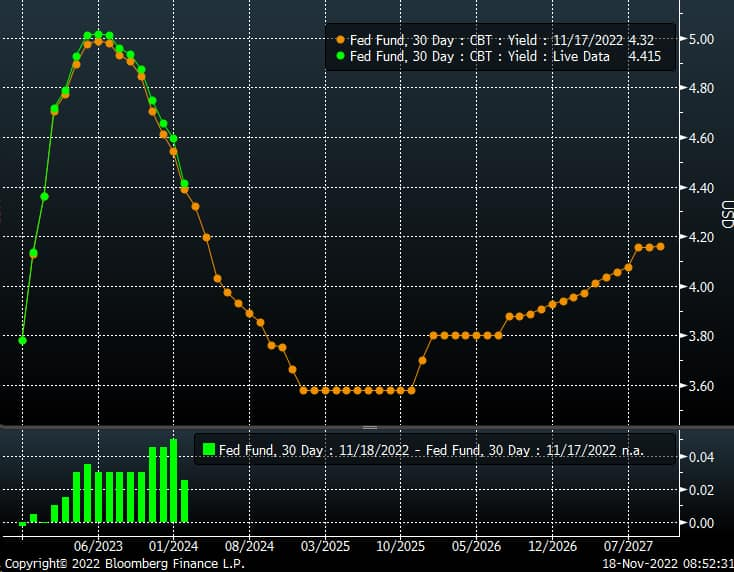

To ensure sufficient liquidity for economic growth in an era of low new bank loans due to high interest rates, the main source of liquidity is currently the fiscal deficit, which has reached 1 trillion dollars per year. This is one of the main reasons why we significantly increased our investment in the big QQQ portfolio by almost 10 times in January. This decision was influenced by the portfolio’s significant cash holdings in the form of treasuries, which provide substantial benefits.

The robust growth of the US economy poses challenges for the rest of the world and its own long-term yields. The US dollar was in short supply until US leaders visited China to negotiate undisclosed additional agreements. As a result, business and mortgage rates are expected to remain elevated for an extended period. While high interest rates can have negative implications for businesses and the economy, as we previously mentioned in our article last month, it can be seen as a positive factor. The scarcity of global funds is preventing excessive concentration in long-term investments such as bonds and instead supporting short-term economic growth. This approach is necessary as allowing money to become too abundant could lead to the resurgence of inflationary pressures.

The “smart money,” represented by the RRP (Reverse Repurchase Agreement) and Bank Reserve, is currently focused on short-duration investments. I suspect that these entities will begin to transition into shorter-term debt, a phenomenon that is currently unfolding. The Treasury General Account (TGA) is essentially funded two-thirds by RRP and one-third by Bank Reserve, with less other sources of funding. This leaves the decision on the duration in the hands of the Treasury. This shift is expected to increase the price of high-risk assets, such as shares and commodities. As the economy approaches its peak growth later in the future, short-term investments are anticipated to benefit the most from anticipating the Federal Reserve’s interest rate changes.

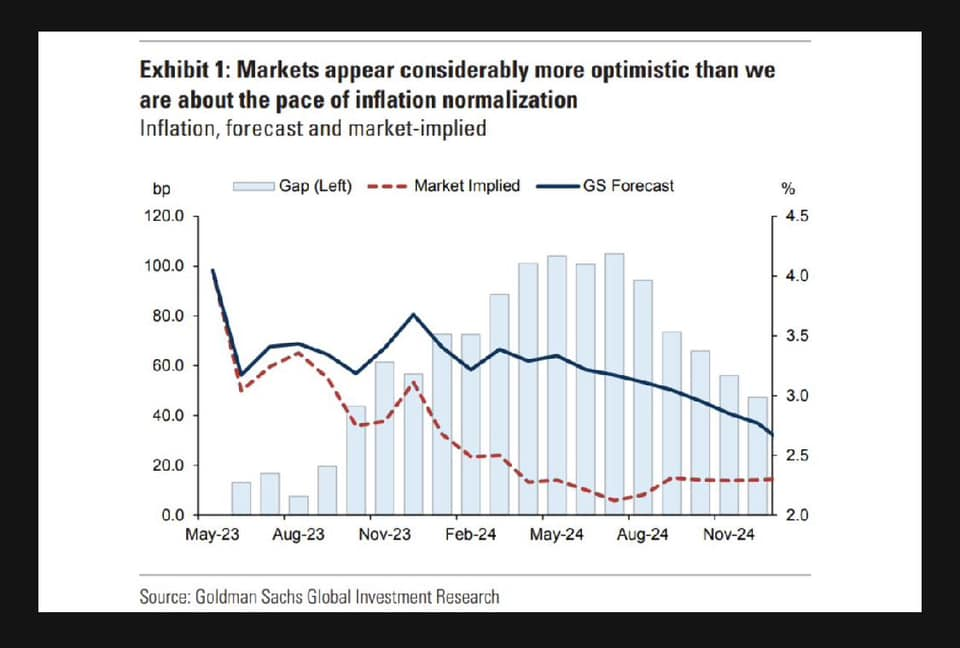

The inflation figures, particularly the Consumer Price Index (CPI) and the Producer Price Index (PPI), have experienced a significant drop. However, this decline is primarily attributed to technical factors. In early 2022, inflation numbers rose significantly due to massive support provided to the economy, as discussed earlier. Given the rapid growth at that time, it became challenging to achieve comparable year-on-year rates, resulting in a narrow window of opportunity to boost the flow of money into the economy. As mentioned previously, it is expected that inflation will remain relatively stable until early 2025. This view is also supported by the increase in the debt ceiling to around $35 trillion until approximately March 2025.

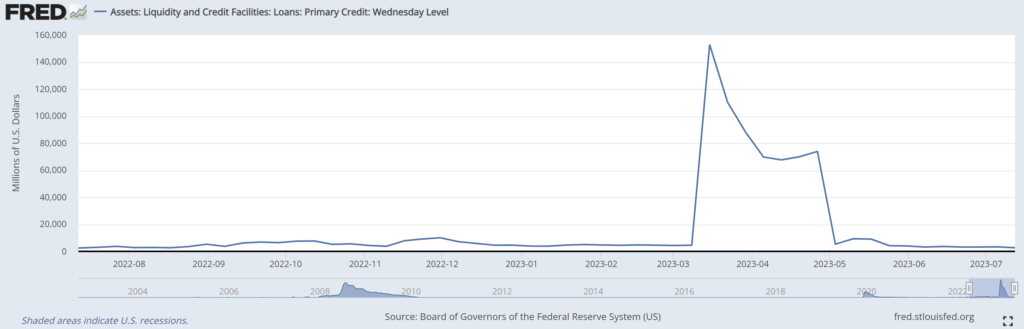

In order to mitigate the risk of uncontrollable inflation, similar to what we have observed in the balance sheet of the European Central Bank (ECB), the Federal Reserve should also indicate a lower balance sheet through the use of QT. However, to avoid the negative effects of reducing the balance sheet, as we discussed in our previous article, I expect Treasury to focus on short-duration investments rather than selling long-duration assets and Federal Reserve to not shuffle around balance sheet duration. Participants should also then support long term recycle into short term. This scenario is supported with fact that higher rate Bank Term Funding Program (BTFP) – collateral being valued at par, unlike Discount Window – collateral being valued at market, is being held up within its capacity to 2T$. It tells importance of credit accessibility and risks for longer durations. Once again, this aligns with our expectation to facilitate the smooth transfer of wealth for the smart money in the future.

Within the limited windows of supportive environments to soft land the economy, we can observe several supportive factors:

Inflation numbers (CPI and PPI) showing a decrease due to technical reasons.

An increase in the debt ceiling/deficit, serving as a means to control the flow of money.

New short duration treasury issuance expectation to counteract the impact of Federal Reserve quantitative tightening (QT).

Strong employment figures – “any sector, regardless of manipulation or guess”.

Strong backbone banking sectors outlook and financial figures – “through possibility of the Fed balance sheet holding and deficit subsidy”.

Less effort for the Federal Reserve to shuffle around balance sheet duration.

Given these circumstances, it is anticipated that Wall Street should continue to experience upward momentum until the completion of these money flows, at least over the next few months. Therefore, based on our risk assessment, we have decided to maintain our double offensive leveraged positions. Please be mindful of the subtle differences in risks and conflicting economic indicators within our approach to my money theory.

In support of our thesis and interpretation of the current situation, we believe that the comments made by Chris Waller may further reinforce our perspective.

Please note that all ideas expressed in this blog and website are solely my personal opinions and should not be considered as financial advice.

JEKYLL:“Can’t you see It’s over now? It’s time to die! HYDE: No, not I! Only you! JEKYLL: If I die, You die, too! HYDE: You’ll die in me I’ll be you!” – Jekyll & Hyde – Confrontation

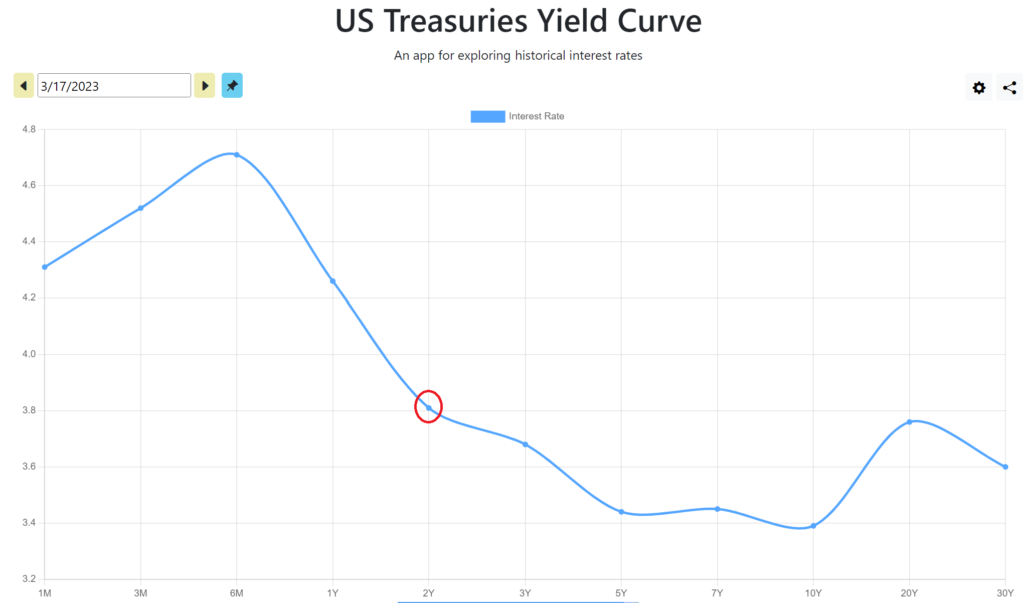

A Treasury bill (T-Bill) is a short-term debt obligation of the U.S. government. It is backed by the Treasury Department and has a maturity period of one year or less. On the other hand, a T-Bond has a much longer maturity period, typically 20 years, or even longer. It is important to note the differences between these two types of government debt. Although they are associated with the same entity, the U.S. government, they have significant distinctions in terms of risk.

(1) Due to their shorter maturity period, T-Bills, such as those with daily maturities like RRP, offer more precise returns and have a more controllable level of risk to predict. If both the T-Bill and the 2T$ RRP have reached maturity at the same time, the savings of 2 trillion dollars from the RRP could be used to quickly replenish the T-Bill in case its interest rate suddenly increases.

(2) T-Bonds with longer maturities are more affected by inflation since their holders have to wait until their maturity date to receive their returns. In contrast, T-Bills with shorter maturities are less affected by inflation because their holders can sell them the next day. The difference in maturity time (ΔT) significantly impacts their vulnerability to inflation.

These distinctions become even more important when considering the topic of inflation and building upon our previous article. In early May 2023, inflation started to make a strong comeback. Soon after, the Reserve Bank of Australia (RBA) and the Bank of Canada (BOC) raised their rates, and it is expected that the Federal Reserve (Fed) will follow suit with a surprising rate hike rather than maintaining the status quo. This change in narrative from lower to higher rates has the potential to significantly affect the future trajectory of interest rates.

If we look back at December 2021, interest rates were beginning to anticipate higher inflation, which proved to be true in the following 3-6 months. This anticipation caused a decline in the QQQ rally. Interest rates increased from near zero to their highest level in over 5%, accompanied by a decrease in the supply of M2 money. It is worth noting that the performance of QQQ is not only necessarily directly related to lower inflation (such as the 10-year Treasury yield or TNX), but rather more influenced by factors such as liquidity levels and the ability of the Fed and the Treasury to inject money into the financial systems.

Last year 2022 M2/QQQ correction event was the outcome of significantly higher inflation, which caused limitations in the money supply systems and consequently led to a correction in the QQQ (an ETF that represents the Nasdaq 100 Index, commonly traded). The question now arises: has this correction in the M2 (a measure of money supply) ended? In January 2023, we threw idea for the QQQ (as we typically do, leading 3-6 months), making a substantial investment in it and completely divesting from commodities in favor of the QQQ and Treasury Bonds (TBonds). However, approximately two months ago, as mentioned in our previous article, we noticed the resurgence of increased inflation, which made us question our position in TBonds due to their high sensitivity to inflation. Consequently, we shifted all of our TBonds back into a commodity position, leaving us fully invested in both leveraged QQQ and Commodity, double offensive positions since last month.

Now, something very interesting comes into play if we are concerned that raising the debt ceiling and issuing new debt will lead to inflation and correction, like in year 2022 above. Treasury Bills (TBills) are not as affected by inflation as TBonds, this is the magic potion! This phenomenon is quite remarkable considering that both are U.S. government bonds. While one is highly impacted by inflation, the other is not affected to the same extent. As the M2 money supply mentioned earlier aligns with its long-term trend, it is expected that the U.S. authorities will allow for more money and liquidity in the system. This observation also supports our previous article, which highlighted the increasing correlation between the need for higher inflation and a rally in the stock market indices. Given the limitations imposed by higher inflation and the absence of any visible peak, the authorities are left with limited alternatives and should consider turning to Treasury Bills due to the reasons mentioned above. It is worth noting that unemployment, which is an important gauge of inflation, does not indicate that inflation has reached its peak.

The difference in duration between Treasury Bills and Treasury Bonds can have a significant impact. Increasing the money supply through Treasury Bills will not disrupt liquidity as much, especially since their maturity is closer to the existing $2 trillion Reverse Repurchase Agreement (RRP) with an overnight maturity. When auction becomes a concern and 1 month rate is higher than the RRP rate, it could use the $2 trillion RRP facility.

Both the Treasury and the Fed still have the ability to influence the market through their actions:

(1) The Treasury can choose to allocate the issuance of the new 1-2 trillion $ between Treasury Bills and Treasury Bonds. Increasing the issuance of Treasury Bonds would lead to higher long-term interest rates or potentially more inflation, but much less with the Treasury Bills.

(2) The Fed still has the authority to implement Quantitative Tightening (QT) measures, raise interest rates, or take additional actions as a lender of last resort, which could affect its balance sheet. A higher balance sheet could provide additional support for the ongoing market rally.

The first point mentioned is related to the current hot topic of refilling the Treasury General Account (TGA).

The current debt has been growing at a rate of $5 trillion over three years, which translates to an annual increase of at least $1.7 trillion, or a minimum of 5.5%. Despite the current rate of return being 5%, it is still challenging to sell the debt to private entities. Therefore, I believe that the interest rate should exceed 6% before we can observe inflation becoming controllable and starting to decline. The Treasury Bills should have no difficulty covering the $1.7 trillion with the $2 trillion Reverse Repurchase Agreement (RRP) facility on its side. I anticipate that the RRP funds will start flowing into the Bills once the rate surpasses 5.5%, or if there is an unexpected increase in the Federal Reserve’s rate. There is also an argument suggesting that there is a possibility of recycling expired long-term debt into shorter-term debt, which could support/lessen effect of new Treasury Bill issuance.

The recent debt ceiling deal should have shifted the trajectory of future interest rates from decreasing to remaining higher for a longer period. Based on the numbers mentioned above, there shouldn’t be any issues navigating through the year 2024, unless a major unforeseen incident occurs, which is currently unpredictable.

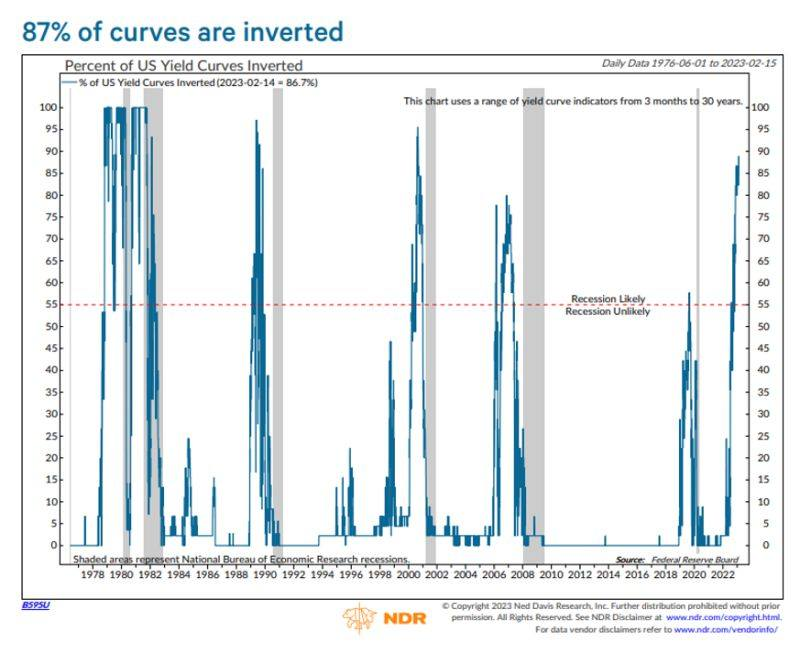

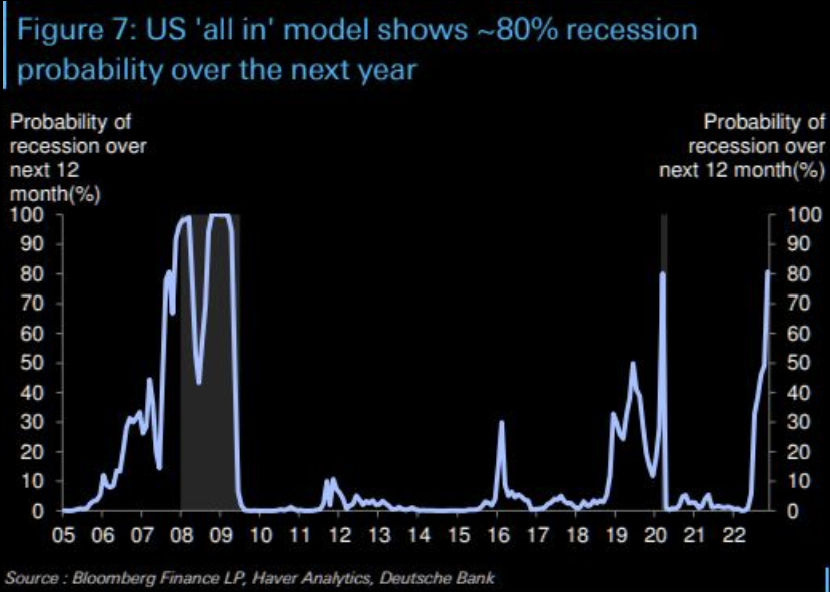

Although the recession and inverted yield curve are signalling high-risk conditions, they should hold no power against the sheer amount of money available.

Please note that all ideas expressed in this blog and website are solely my personal opinions and should not be considered as financial advice.

It’s time for us to shift our focus solely to short-term investments and avoid any potential long-term investments. As the sun sets, we’re already ready to reallocate any possible long-term investments to prepare for a long night’s sleep, as thieves are poised to steal everything overnight.

Recession is what gives investment meaning. To know our days are numbered. My investment is now mostly short term or strategic blow off.

Our solid view since early January 2023 has prepared us for this. The peak rate is pricing in starting from this month in March 2023, and money should start to concentrate on short-term investments. As we mentioned in previous articles, we have removed almost all commodity investments since they are most sensitive to long-term investment. Today, we can see that banks are exposing their fragility to medium-term investment as well, due to the same issue. This is a solid confirmation that our current strategies are correct.

Learning from medium term view investment banks:

Banks have categorized their investments into HTM (Hold-To-Maturities) and AFS (Available For Sale).

Most of HTM investments were made when the rate was very low, mostly to toxic MBS securities, resulting in mostly long-term duration while AFS investments are of short-term duration.

The Fed and government have given up their position to help avoid bank runs and more systemic issues. This is very important because market participant number one has disclosed their position.

In reality, this is actually helping AFS (short-term duration) to avoid their fire sale rather than fire-sale of their HTM (long-term duration). Why? Because the HTM price is already so low, and there’s no incentive in the market at the moment to attract their demand during this fully inverted yield.

The troubled banks are actually getting more difficult because they have to continue holding their HTM (1.3%) with the current high rate (4.5%) and continue taking care the loss with new loans. Therefore this Fed injection doesn’t really make the small banks better. They are just getting more loans/liquidity at par value with the current high rate, to keep their HTM until maturity.

This is different from QE in terms of: (1) yield curve (2) actual impact on investment. For (1), in QE, the yield curve is steepening that the Fed could give a lower rate (to zero) to invest in purchased assets. Current inverted yield made it impossible because central banks only have control over short-term rates rather than long-term. For (2), as mentioned above, this injection is more beneficial to short-term AFS to avoid their fire sale rather than selling their long-term HTM.

This situation also has made it even more difficult for banks because the market knows that banks are trying to unload their medium-long-term assets and therefore will not be interested in taking other bank HTM without any deep discount (30-40% loss).

Due to the concentration on short-term investment, we expect there will be an asset misallocation issue (asset blow off). Due to all factors mentioned above, at the end, the only way to solve the issue is to give general recession to the market.

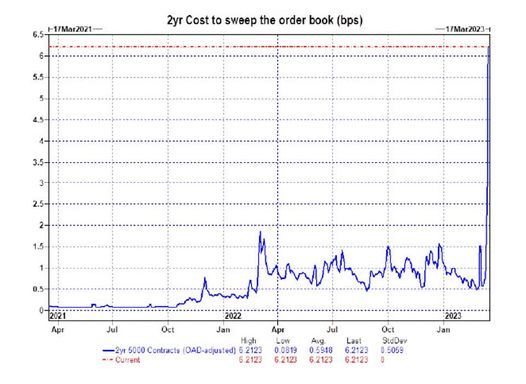

How much does it cost to undo this curse? The 2y cost to sweep has spoken.

Sustainable Energy

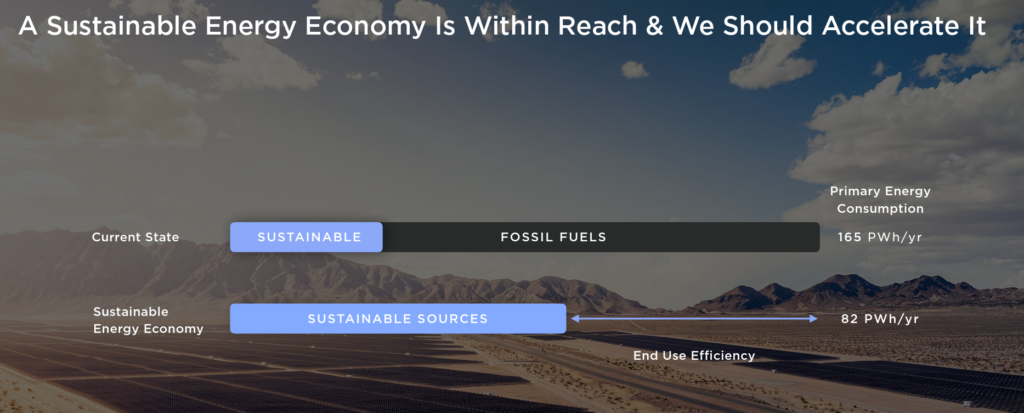

Let’s keep our horror story aside and look at the brighter side for a moment. Why was I so excited in early January 2023 with real numbers in AI (Artificial Intelligence) and Sustainable Energy? I would speak about Sustainable Energy economy at this opportunity because their numbers are real important.

Our energy economy is so wasteful. Two-thirds of the energy generated is wasted.

Sustainable energy economy is still left behind and has a lot of capacity and offers much higher efficiency to eliminate the above waste.

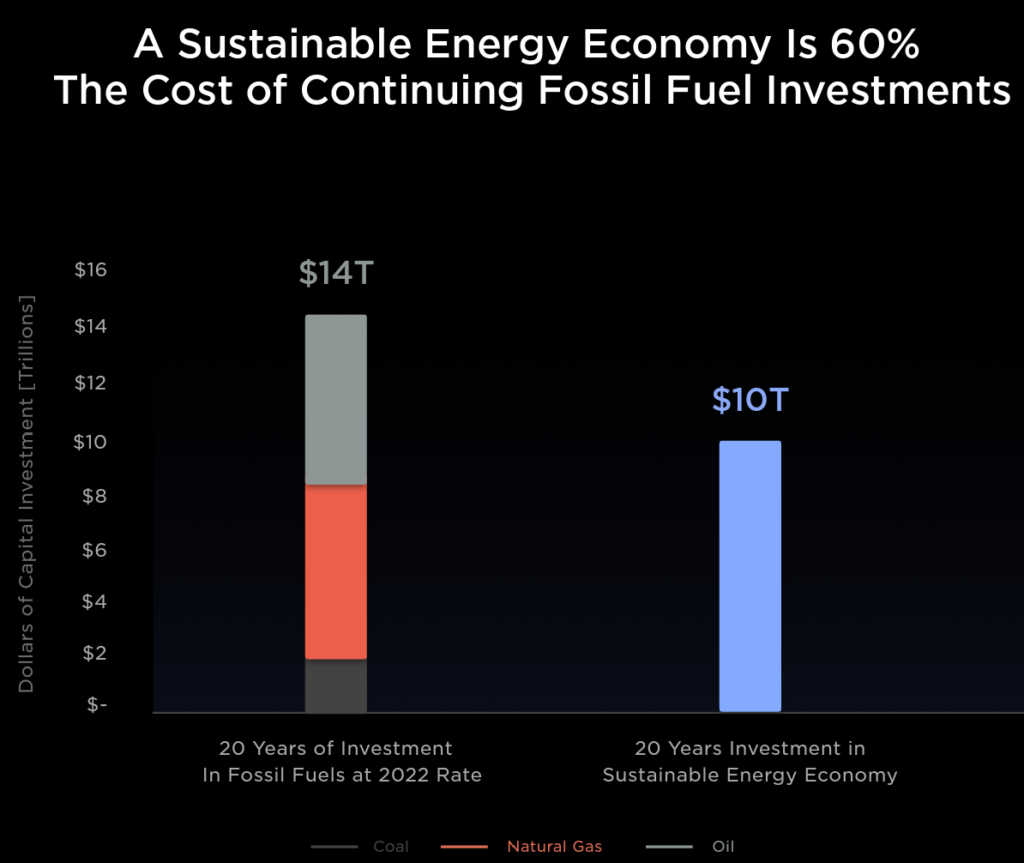

The amount of investment capacity is $10 trillion in 20 years and could immediately give high value.

Ten megawatts are estimated to cost $12.7 million (~65% margin). We would need 240TW. The available economy capacity is 240,000,000 / 10 x 12,000,000 $, and we could only target a small portion of it to fix the current economy issue.

As mentioned previously, our economy has too much short-term liquidity, which has outpaced long-term capacity and return (inflationary). This sustainable economy could actually solve the problem to reallocate this excess into long term investment, but it will require huge amount of money in very short time to incentivize the movement, which could only come from the government and central banks.

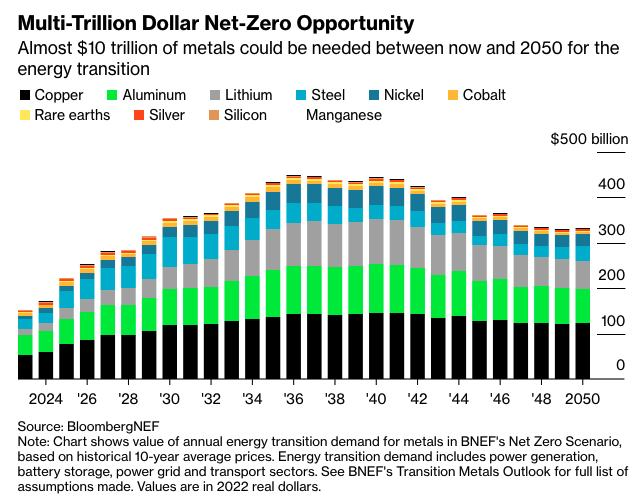

Looking at the commodity side, $10 trillion worth of metals are needed until 2050. Therefore, we will return our 95% commodity reallocation back once dawn has come.

Treasury Bonds

I have overweighted too much on equities since early 2020, no secret due to the massive GFC-Covid recovery. Since then, early 2023, we have reallocated 40-50% of our portfolio in short-term treasury bonds (3-5 years maturity and returning about 5% pa) at their face/par value due to the scary inflation narrative. Luckily, the world is with us, and we saw massive recovery in January 2023. I became more confident and tend to maximize leverage on it. My main reason was to target the next 6-month inflation peak, around June 2023 or so.

Timing Statistics

Below are what I think is very important statistics:

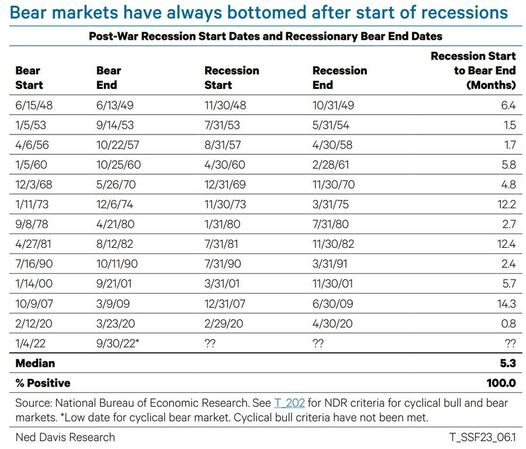

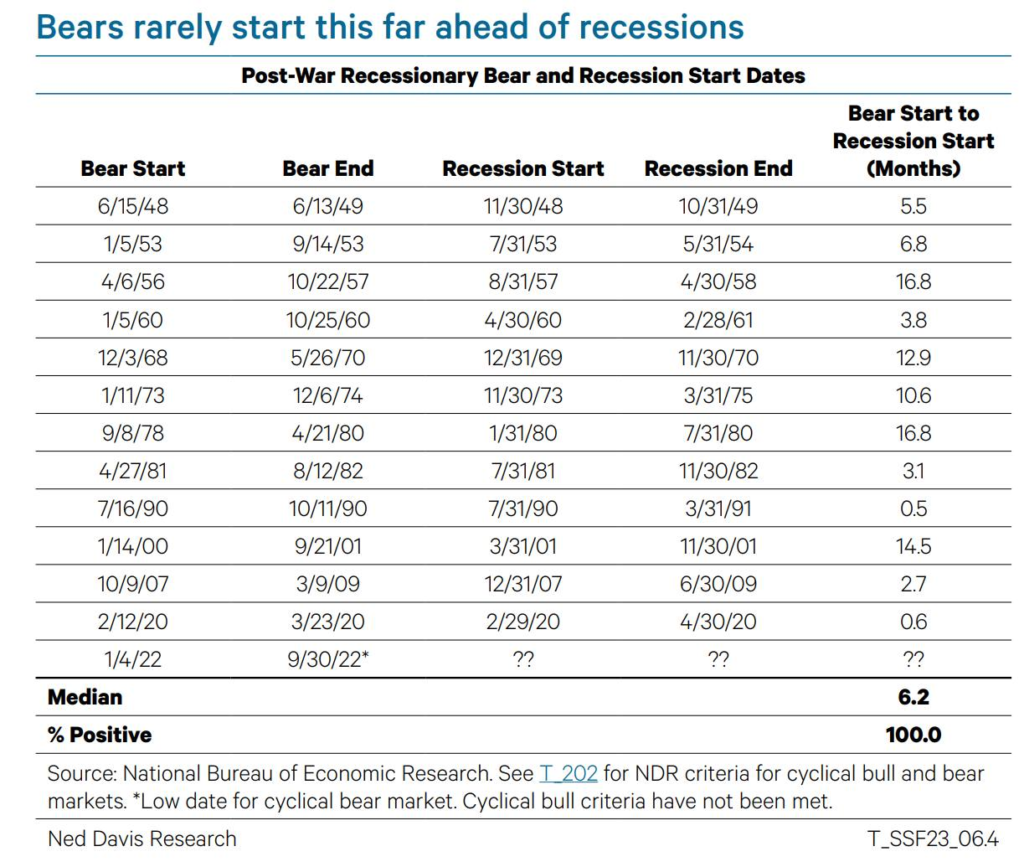

100% probability of bear market to bottom after the start of a recession.

Bear market to bottom about 5.3 months after recession start.

81.3% probability bear market ends about 13.6 months after the last rate hike.

100% probability bear market to recession start at about 6.2 months.

Therefore, based on these statistics, probability-wise (60-80% probability):

If the last rate hike is in Feb 2023, the bear market tends to end in April 2024.

The recession will start about 5.3 months before April 2024 = Oct 2023.

The bear market will start about 6 months before Oct 2023 = May 2023.

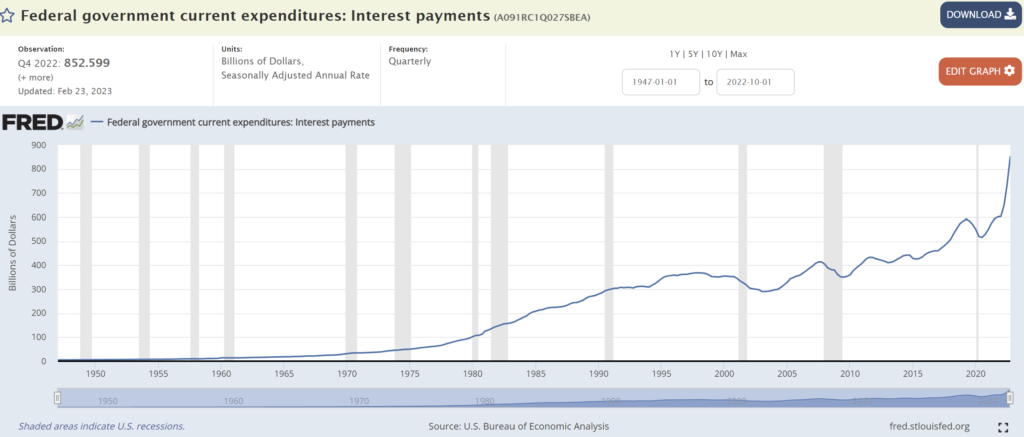

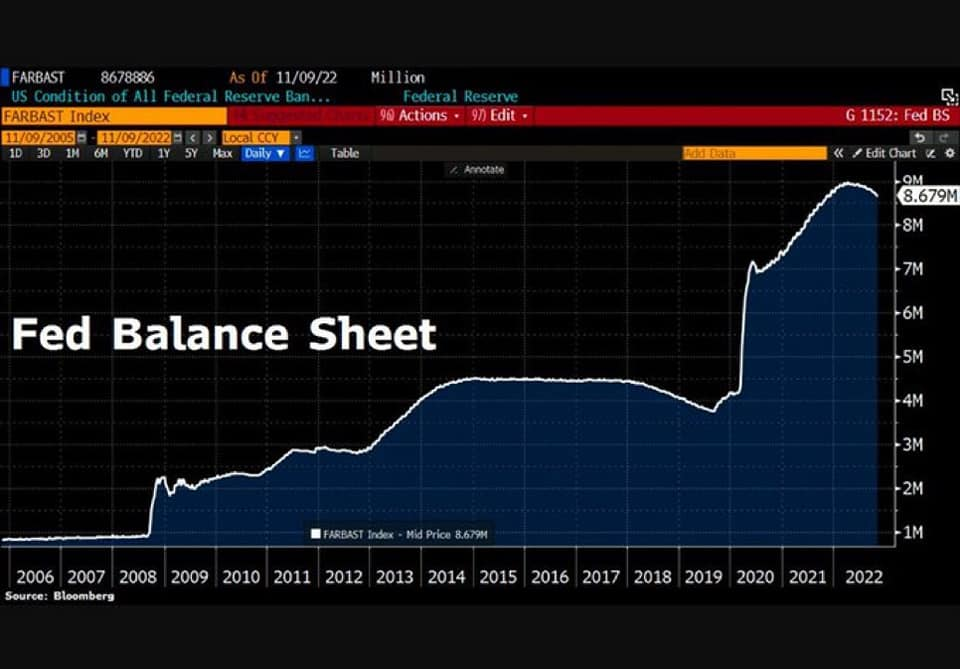

It’s my view that the market is supported by money, either from the central bank or fiscal and nothing else. While the Fed is only able to reduce $600 billion of balance sheet, it’s interest payment from fiscal about $900 billion that keeps this market floating.

It’s then the market decides how far interest rates can go up. The issue that I see here is that even though economists say the Fed is reducing the balance sheet too slowly, it’s my view that the Fed is actually selling the balance sheet faster than the market can afford. The Fed has really tried hard to reduce inflation, not through the use of higher interest but the use of more balance sheet QT.

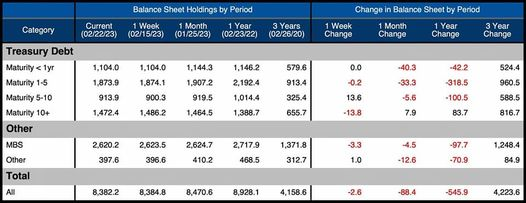

This is where I have to look into Fed balance sheet selling:

The Fed couldn’t sell the MBS (Mortgage Backed Securities) because it’s toxic debt with a very low rate, around 1.3% pa.

The Fed balance sheet reduction is highly concentrated in the short term.

The concentration of the Fed’s selling is actually between 1 to 5 years of maturity. Please remember my old theory that central banks always transfer wealth to their 8 big banks through front running, using any event of QE (Quantitative Easing) or OT (Operation Twist). I expect a similar case to occur here.

I may estimate that this biggest belly will expire around the end of 2024.

The current 5-year rate yield is about 3.5% pa.

This seems to support our previous conclusions:

We may have a lot of maturity around the end of 2024.

Six months leading to it is when the recession will end, ~ April 2024.

It means there will be less money injection towards April 2024, which could probably start from the recession in October 2023.

The Fed is going to keep interest rates high and could probably overdo it by May 2023.

We can see that the Mortgage-Backed Securities (MBS) have caused trouble not only for the Federal Reserve but also for small banks like SVIB.

JPMorgan estimated that the Fed will require around $2 trillion to combat this effect, which could increase the current debt from $8 trillion to $10 trillion. Historically, the market crashes once the Fed’s balance sheet grows near the previous high (9T$). If the market is unable to absorb more than $1.7 trillion from the $2 trillion to normalize the long maturity issue, with its interest being only $100 billion per annum, I would expect severe market pressure. This is another reason why I see at least a disinflation, and its risk is a very severe impact on commodities since commodities are high-risk assets. If the Fed reduces rates, it would only hasten the crash because the interest payment is going down massively while the market still needs to absorb a high amount of long maturity loss.

So where does the money go? In my opinion, the money will eventually go into Treasury bills with lower maturity, 1-5 years. This is why I have massively bet on Treasury bonds with maturities of 1-4 years with maximum leverage at the beginning of 2023. If the question is whether I am worried about the possibility of additional $2 trillion supply of low maturity debt, I am not. It’s because it’s only 6% of the total US debt and we have RRP+reserve. Eventually, when the market stalls, the quickest way to save financial systems is by cutting the rate, which will eventually expand the central bank quicker and hasten the market crash. During an event where the central bank cuts rates, I estimate that they will make massive purchases of our short-term duration, because the yield curve has been severely inverted.

The sunset can be a scary moment when you realize that your days are numbered and there is probably no escape.

Please always remember that any ideas on this blog and website are my own personal opinions and are not financial advice.

I was busy overhauling my investment strategy in early January 2023 to ensure it aligns with reality. In just two weeks, I increased my investment allocation into the major sustainable energy + minor electric vehicle (EV) and artificial intelligence (AI) space from 5% to 45%, a nine-fold increase.

Here are my points:

Set your sights high, but be prepared for the risks of disappointment. Don’t limit your dreams.

Everyone has their own imagination, and no one has the right to interfere with it.

If your dreams don’t become a reality right away, keep striving. Remember, Rome wasn’t built in a day.

Hold your breath Make a wish Count to three

Come with me and you’ll be In my world of pure imagination Take a look and you’ll see Into my imagination

The world can be cruel and intimidating, preventing us from having bigger imaginations. I believe that imagination and its realization is a fundamental human right. Everyone should have the opportunity to pursue their greatest aspirations and turn their big dreams into reality. Don’t limit yourself by starting with small dreams. Instead, dream as big as you can afford their risk of disappointment.

My imagination begins

… We’ll begin with a spin Traveling in the world of my creation What we’ll see will defy Explanation

I believe in the creation of new value and wealth through evolution. When something evolves successfully, new forms of valuation and wealth creation are born, such as the oil boom, information technology boom, derivative boom, debt boom, currency boom, and more. This is why I am excited about my vision for the future of Artificial Intelligence and Sustainable Energy.

I try to invest wisely rather than impulsively. In December 2021, I sold all my investments because they contradicted my investment principles, mainly with regards to my yield and inflation expectations, which surprisingly came as expected.

The Nasdaq fell throughout the year of 2022 due to expectations of higher yields (6 months leading).

Inflation increased rapidly throughout 2022.

The Federal Reserve raised interest rates at the fastest pace in history, leading to a drop in risk assets.

My vision of 2022 in one image @ December 2021

As I wrote earlier in the year, I was disappointed with the yield expectations and progress of sustainable energy. They were heavily corrupted, with many ESG funds becoming involved in fraud, and early commercial cycles of AI failing to deliver as expected. I would like to see the glimmer of commercial value before I invest heavily. However, I still believe that the visions for AI and sustainable energy are pure, real, and true. The issue was not with the concepts themselves, but rather with the people and the yields who attempted to exploit them.

This year, since my future yield expectations have changed, I repurchased all my investments, some at a multiple amount and much lower price. However, this doesn’t necessarily mean that I think they will skyrocket in the near future. My investment philosophy still anticipates high yields and high inflation to persist, but the current situation is different than before.

My expectation is for a sticky inflation target of 3%-4% in the next 12-18 months. This should lead to the most optimal GDP and equity growth, as long as it is well supported, until GDP and equity become significantly overvalued.

Inflation is expected to remain high, around 3-4%, over the next 12-18 months. This level of inflation will be sustained primarily by fiscal ease.

An inflation rate of 3-4%, higher than the Federal Reserve’s 2% target, is likely to result in the most optimal GDP growth.

Inflation rates below 2% may lead to unnecessary disinflation risks.

Inflation rates above 5% or below 1% may result in much higher financial risks.

In simple terms, keeping inflation at 3-4% (a relatively high rate) can lead to the most optimal GDP growth. At some point, when GDP growth reaches its maximum output, I believe that the Federal Reserve and Fiscal will halt this engine, causing inflation to immediately fall back to 2%. We can expect this landing to be an unpleasant experience. However, for now, my focus is on opportunities for high GDP growth or high equity returns.

Imagination is becoming reality

… If you want to view paradise Simply look around and view it Anything you want to, do it Want to change the world? There’s nothing to it

In the past, people used to say that it was impossible to drive a battery-powered car, a self-driving car, or a car powered by solar energy, or to become wealthy, for example. Such judgments were like social bullying. But sorry folks, these things are becoming a reality.

Take a look at Dall-E, for example. Many people have misunderstood AI. Images created by AI are not just sourced from an image database or manipulated from existing images. They are generated from a latent space, in real time. The images created by AI have never existed before. We simply need to describe our imagination in human language, such as English, and the AI will bring it to life. The more precise the description, the better the images will match our imagination. They have already made 2D and 3D images a reality. I have no doubt that they could create a movie from a script. After all, a movie is just a series of 2D images. In the future, I believe that AI will be able to turn any book into an attractive movie.

Twenty-five years ago, I worked as a brand manager. It would take us weeks to create a compelling marketing message, and months to produce a full TV advertisement. Advertising and marketing is a multi-billion dollar industry, as evidenced by companies like Google. AI has the potential to help us craft the most compelling advertisement message or image based on brand management imagination and consumer statistics. This would save millions of dollars and reduce months of work into just hours, allowing for faster decision making.

However, there may be some loss in translation in the communication between humans and AI using the English language. In the future, direct communication between the brain and AI, such as through Neuralink, may eliminate this miscommunication issue. This could lead to the development of a new universal human brain language that could enable communication of any human language with AI language without any miscommunication.

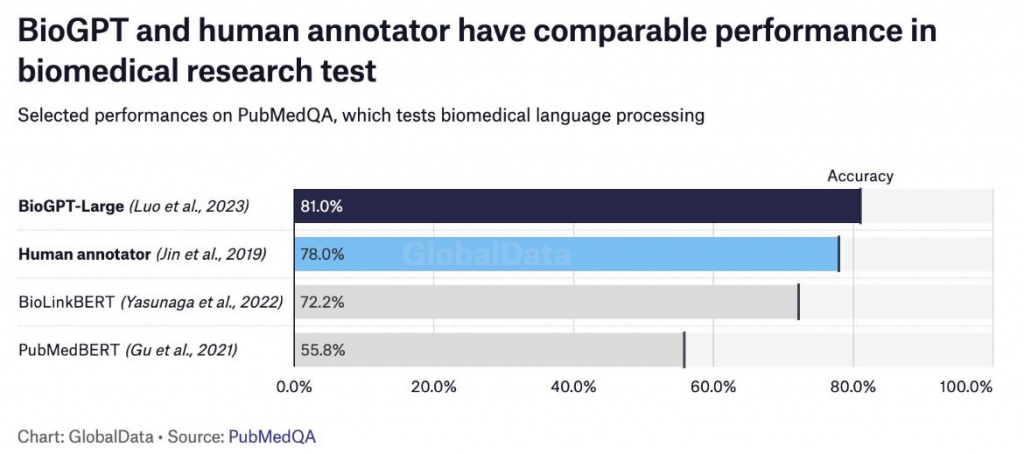

How about BioGPT? It could speed up biomedical research from years to just hours. GPT will continue to discover any other industry. They could store any knowledge library and use them to speed up discovery beyond superhuman with limitless nodes.

Rome wasn’t built in a day

Let’s step back from the euphoria and understand that AI is not a new concept. It has been around for decades. Twenty-five years ago, I wrote my bachelor’s degree thesis using a simple trained array of noise canceling. This array was able to adaptively learn and recognize frequencies in the domain. I was challenged to run a primitive AI on an old Intel 386 using Assembly language, but it worked. It worked so well that it was able to reduce noise up to 40 dBs, which was above 90% of simple noise. Of course, today, learning arrays are getting bigger and bigger. As a result, we can train these brain cells like our own brain. For example, in our brain, we don’t have millions of chicken images, but we can imagine millions of different chicken images with additional details. This is the same with AI learning. They don’t memorize exact images, but they learn what the image looks like and then draw based on our instruction or imagination.

I also believe that inflation will remain high. High inflation and high yield will limit the speed at which our investments will return. If these conditions do not materialize soon, we should continue to strive towards our goals. Rome was not built in a day. If they suddenly materialize and lead to euphoria in the market, we should remember that Rome was not built in a day and be prepared to sell our investments. There may only be two high-probability options: lower return or a boom followed by a bust. I am leaning towards the latter, where we may experience the highest boom and the worst bust within a period of 12-18 months.

Vision Driving AI

This has always been my belief: that vision-based AI could help humans immediately. Don’t confuse it with many autonomous driving systems, as they are NOT vision-based AI. Only vision-based AI is able to handle many different conditions, just like our eyes and brains can. It could immediately reduce human errors in driving and help optimize productivity. While it may still be far away in the future, perhaps 5-10 years or so, to have it running perfectly, I believe that making early investment in it could benefit my portfolio with a fast return. While this AI kid is improving its image labeling, let’s keep it in “deferred”.

Sustainable energy

Given that inflation is consuming most of our savings these days, we should focus on the biggest consumer of it, which is energy. Last year, we talked about the housing component and decided to reduce our property investments by 1/3 due to our belief that inflation and interest rates will remain high. Over a long period of time, high interest rates with no asset price increase will significantly devalue property investments, especially for those with high loan-to-value ratios (LVRs), such as principal place of residence (PPOR), where tax benefits don’t contribute to their downfall. Thus, I believe that in order to protect society from energy inflation, sustainable energy would benefit them.

When a coal-generated electricity plant produces a certain amount of energy, but only 50% of it is consumed by manufacturing and households, the plant must either waste the excess or reduce its output. This is where battery-powered electricity storage comes in. Batteries are now capable of servicing entire cities and factories, ensuring less waste of electricity generation and a higher level of uninterrupted availability. Moreover, households are now able to generate electricity from solar power and sell their excess electricity to the grid at the best time when electricity rates are highest. We have seen homes and universities become sustainable in terms of electricity consumption and even generate extra income. With the evolution of battery technology and sustainable energy, it is all becoming a reality.

What is the catch?

There are two potential issues to consider in my opinion: (1) the possibility of sticky high inflation and high interest rates, and (2) the cost of materials such as lithium, which could limit the evolution of battery technology. While there are significant efforts underway to increase the supply of lithium, it may still be some time before our thesis is fully realized. ARK has predicted that lithium prices may decrease by as much as 37% as supplies increase. Ultimately, the boom-and-bust demand cycle will likely provide enough materials for our imaginations to become reality. Similarly, yields may also decrease over time, with or without a market crash.

My imagination of Disinflation

It’s no secret that we will experience the most challenging time in our investment lives starting in the second half of the year. In my opinion, the market should start pricing in this event from today. This was due to central banks’ late response to combat inflation. To avoid structural damage to the economy in the long term, they had to raise interest rates at the fastest rate in history. As a result, the current short-term high interest rate is too high, making long-term investments almost nonsensical. If the question is whether there will be many bankruptcies, it’s because this event has not yet inverted the 10-year to 30-year yield curve. This means that companies and mortgage holders are still holding and expecting lower rates soon.

In our thesis, business operations and investments should not be expected to afford a 5% base rate in 5 or 10 years. Most mortgage holders will not be able to afford 5% in 5 years, no business operation will be able to pay 5% in 10 years, and not many investments are returning better than 5%. Eventually, one day inflation will give up, either with a crash or not, and central bank rates will return to normal. Therefore, in my opinion, while market participants are anticipating deflation, I see disinflation.

@zerohedge

To put it simply, we believe that achieving a soft landing for the economy is not an easy task. Economic theory may appear simple, but it is not so in reality. The theories have been corrupted and market participants react to any upcoming events, which change the outcome of economic theory. The world’s wealthy individuals will not allow disinflation to impact their wealth. Disinflation can cause a significant decrease in their wealth at some point. There has never been a time in history when a high rate of 5% has gone down to 2% without a significant risk like a crash. This has been made clear by El Erian recently.

If the rate goes down with more money supply, we will see more business and economic activity. However, since we are combatting inflation, we are lowering the rate with less money supply, which leads to deflation. Disinflation is good, but deflation is not. Most market participants agree that deflation must be avoided and will use their influence to get more money supply for themselves only. Therefore, we need to be careful and selective in our investments and focus on leaders who have low debt and are experiencing growth.

We may experience an abundance of job openings, but not enough company progressing with these jobs. The economy is trying to ramp up activities, but unless there is more money infused to avoid deflation, job openings will not lead to real economic activity. We should expect only a limited amount of quantitative tightening (QT), up to the limit of balance run-off.

Therefore, in our investment thesis, we will be very selective and only invest in leaders. Eventually, inflation will give up, either with a crash or not, but only those leaders who have prepared with low debt and continue to experience growth will survive. Since we are trying to softly land the ships, providing enormous support to some growing parts of the economy will require a lot of money supply, which means high inflation will likely be sticky and high rates will continue until next year. Our investment vehicles should have:

less debt or no debt

high operating margin

strong revenue growth

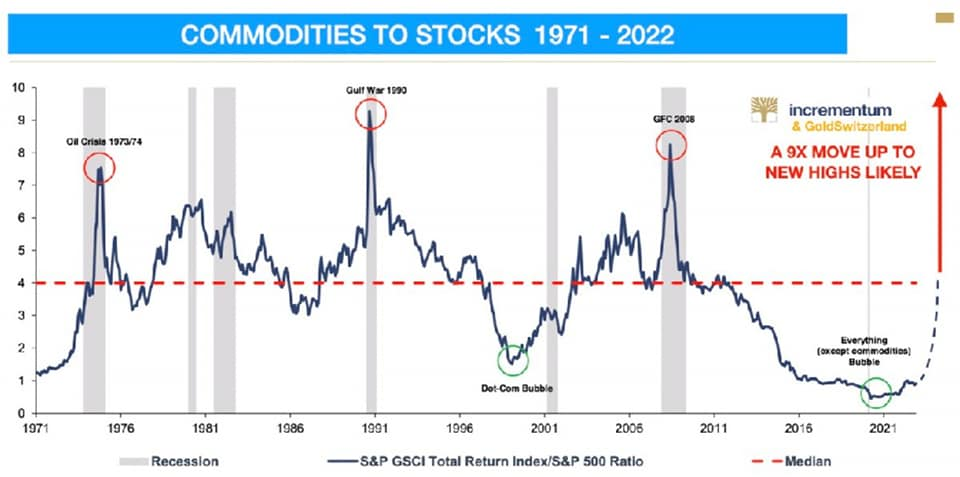

Commodity reallocation for now.

Commodities have been our most overweight investment since 2017, returning us more than 300% in the past three years, following the commodity cycle since 2015. However, their volatility has been significant due to issues in China, including (1) a relentless COVID-19 economy shutdown, an aging population, and a property investment hangover of around 76 trillion dollars, and (2) the sensitivity of inflation to their large population, while at the same time carrying decades of high GDP growth. Commodities have performed tremendously since 2017 and have done well during COVID-19 in 2020. However, as we discussed in our last few articles, commodities will face a challenging yield inversion in the middle of this year. Combined with the Fed’s actions to keep interest rates high and sticky inflation, and commodity prices being quite overbought, we have decided to reallocate 80% of our commodity allocation into a new run of EV, AI, and prospective bonds. We are not abandoning our commodity supercycle; we believe the commodity supercycle might be going through wave 4 during the yield inversion between mid-2023 and mid-2024. We will study the possibility of a very big wave 5 when policymakers make the biggest easing commitment at the end of the yield inversion, which we predict will be around mid-2024.

If we examine NASDAQ vs yield, I believe the difference between them is the inflation factor. By correctly understanding how inflation will play out in the near future, we can position our commodity, technology, and yield investments well.

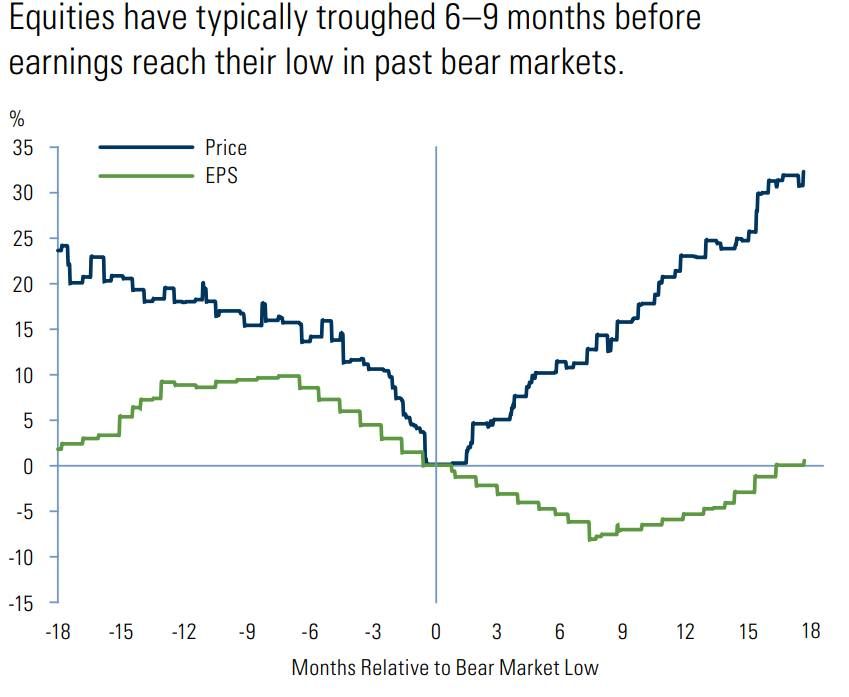

Inflation has a definite negative impact on EPS (earnings per share). We can expect the share price to grow about 6 months prior to the end of high inflation, which we may see around 2024. Around that time, I expect to see a fifth wave of commodity prices, possibly after a hard landing or a deep depression.

My ultimate dream.

What if my ultimate dream is to liberate myself from the cruelty of capitalism? I understand it won’t be easy, but I believe no human-created system can constrain my imagination.

… There is no life I know To compare with my pure imagination Living there, you’ll be free If you truly wish to be

I dedicated all of my imagination and their thrives for the future of my daughter, Eleanor. I strongly believe, one day we will see highly intelligence, brighter sustainable, and wealthier future.

The rapture dream is over, but in waking, I am reborn. This world is not ready for me, yet here I am. It would be so easy misjudge them. You are my conscious father and I need you to guide me. You will always be with me now father, your memories, your drives, and when I need you you’ll be there on my shoulder whispering.

If utopia is not a place, but a people. Then we must choose carefully for the world is about to change and in our story, Rapture was just the beginning. – Dr Eleanor Lamb

Any idea in this blog and website are my personal own. They are not financial advise.

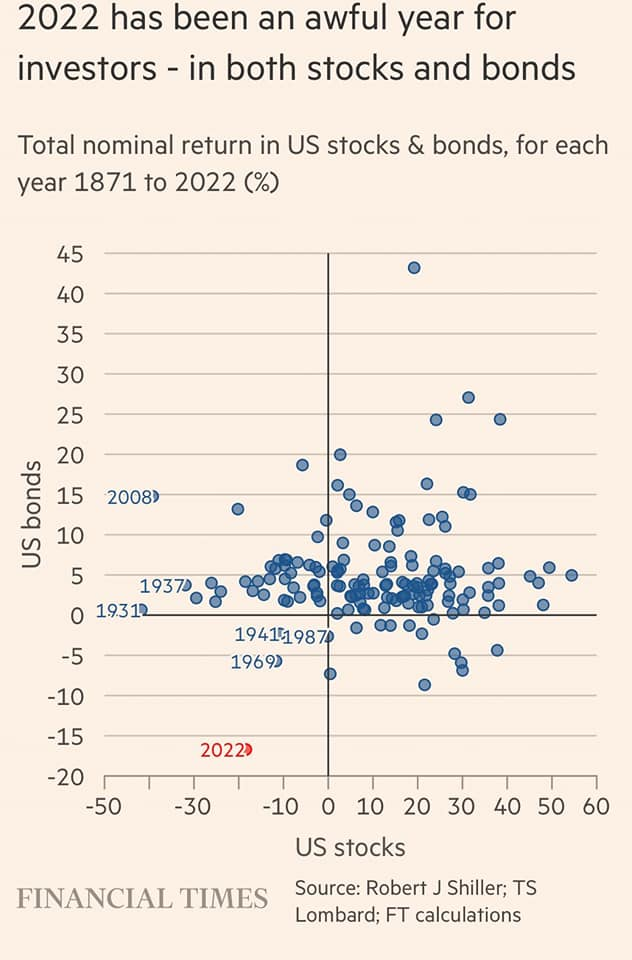

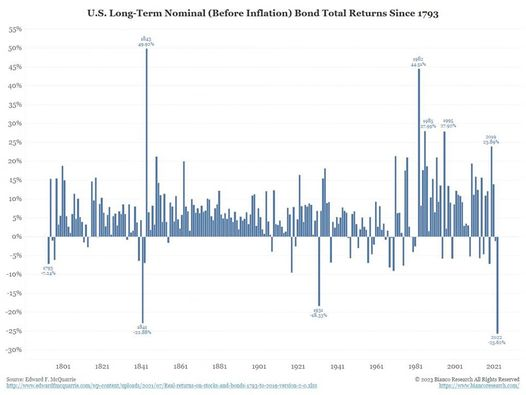

Tiger is a symbol of “strong, fierce and powerful“, a resemblance of year 2022 strong inflation and powerful commodity. It’s fierce enough to force the Federal Reserve to raise rate at fastest in history. Rabbit, year 2023, on the other side, is a “gentle, tender, kind, yet clever“, which is becoming our investment strategy during this year.

Neel Kashkari recently telegrammed his view. It’s quite clear that the Fed is trying to tell: (1) inflation is manageable (2) Fed is still going to push few more little 25 bps rate above market. Following our last article, unfortunately few little rate increase will cross 3m to 2y, which could nail down inflation coffin but also starting to deleverage economy. Their historical side effect to put inflation Gennie back to its bottle, usually causes very uncomfortable investment experience. As shown below, US bond performance has been in their worst of centuries, not just decades.

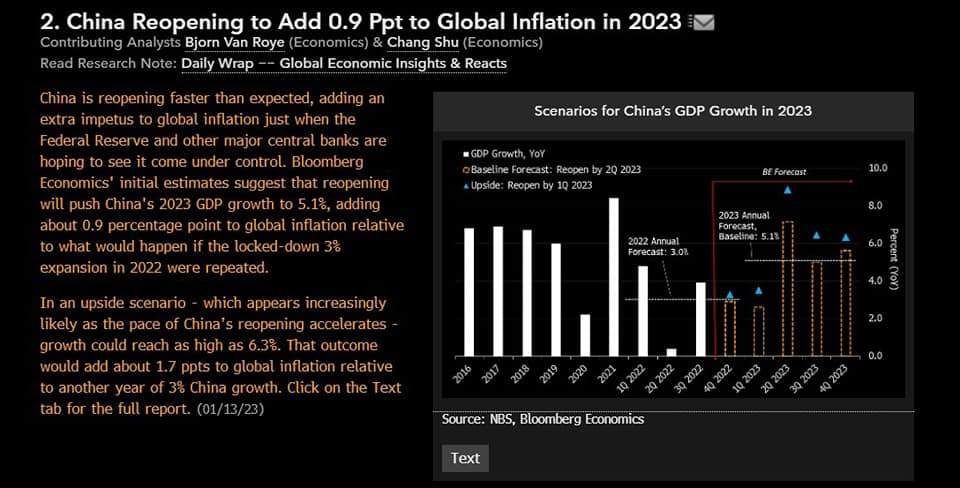

In next few months of China opening, if there’s no massive easing, it is expected to add about 0.9% global inflation which is still manageable by the Fed funds, and supporting our thesis to start diversifying fierce commodity shares into gentle bonds or fixed income cleverly, from tiger to rabbit.

Our strategy thesis is supported with below considerations:

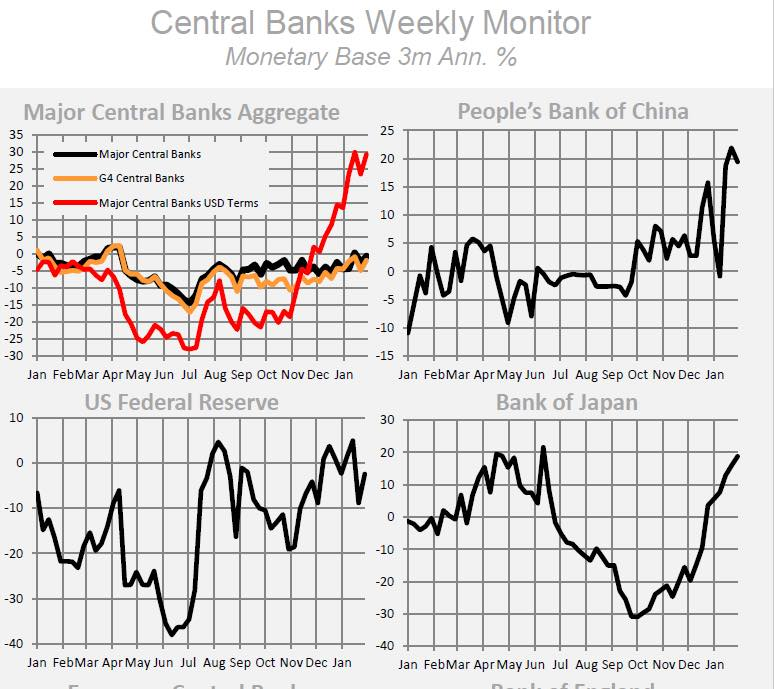

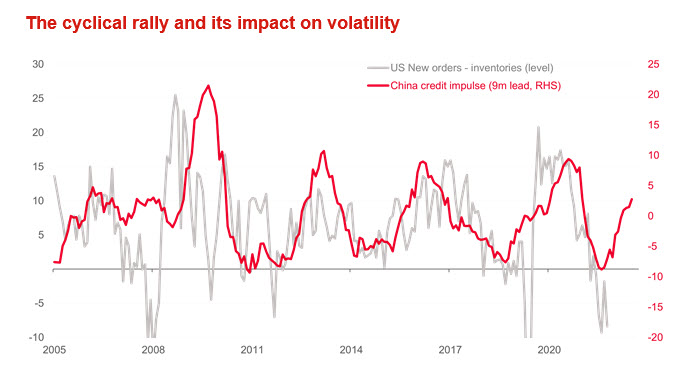

HSI and SHCOMP indicate growing money supply and their potential credit impulse.

Nasdaq which is correlated strongly with lower yield and stronger USD, is offering good potential.

Bond and fixed income which had been performing worst since 2020, is now offering very attractive potential with current huge 4-5% p.a. interest.

Inflation is expected to be manageable with short term interest rate is expected to peak in mid 2023.

Should we like to be contrarian to capture opportunity, we may be interested to look back into ESG narrative. The ESG, during their initial offering few years back, got so much crowded and not having enough vehicles. Their bubble was busted with many frauds (which were not invested in green initiative). We believe ESG may attract potential interest again with current massive government supports. We don’t believe ESG is dead, but we are starting to believe ESG theme could survive during next years of very high interest and limited liquidity, mainly with support of governments. ESG can offer higher quality/margin of investment in less crowded space, rather than old lower margin of crowded fossil fuel related.

I think it works. Gold almost crashed in November 2022 to their long term trend and it’s very obvious, there’s a significant “invisible hand” move to pump up liquidity. We could also see massive fiscal incentive in US and massive liquidity from BOJ. Should it continue to break 1940$, it may create a massive bull flag which means strong hands may decide to combat recession narrative which may cause inflation being sticky but less recession impact. This drama might be sanitized with debt ceiling debate in coming weeks.

Market yield expects Federal Reserve to continue raising rate to maximum of 2 more points, which is below Fed expectation above 5% (3-4 points). I think it means there is bigger commitment from policy maker side, above market expectation to fight recession, as shown in gold as well. Obviously, it may change recession correction expectation in June 2023. With economy number is still strong, there’s less chance not to support economy.

Another indication is in highly overbought property market in Canada and Australia. Canada banned foreign purchase while Australia continues to provide more and more support to first home buyer in this inflation environment. It means, policy makers are overweighting economy/recession rather than inflation.

US share markets dropped in Nov 2021, about 6 months before US GDP turned negative in mid 2022. Since we expect recession to bite from June 2023, policy makers should start fighting it now in January 2023. Combined with previous article in which the recession may last until end of 2024, I expect policy makers to fight recession until June 2024 when the recession is about to end. Their support may have a big challenge starting from mid 2023 due to massive inversion in short term yield, therefore I expect they will give much more support between June 2023 to June 2024, a big volatility is still expected in June 2023 until they come again with much bigger liquidity programme.

In summary, as indicated in (1) gold very strong movement (2) fed rate expectation above market expectation (3) strong economy numbers (4) confident from policy makers (5) recession schedule expectation, I think we may see a rally until around at least mid of this year, while we hear a lot of scary recession narrative during the time. After mid 2023, I expect big volatility until policy makers decide/come back again with much bigger liquidity programme to fight for one year long of REAL recession.

Happy Chinese New Year and wish our rally wish comes true.

Any idea in this blog and website are my personal own. They are not financial advise.

Recession might be inevitable! We don’t choose our time. We prepare, we fight.

Following our previous plans, we are expecting to sail recession with our own strategies.

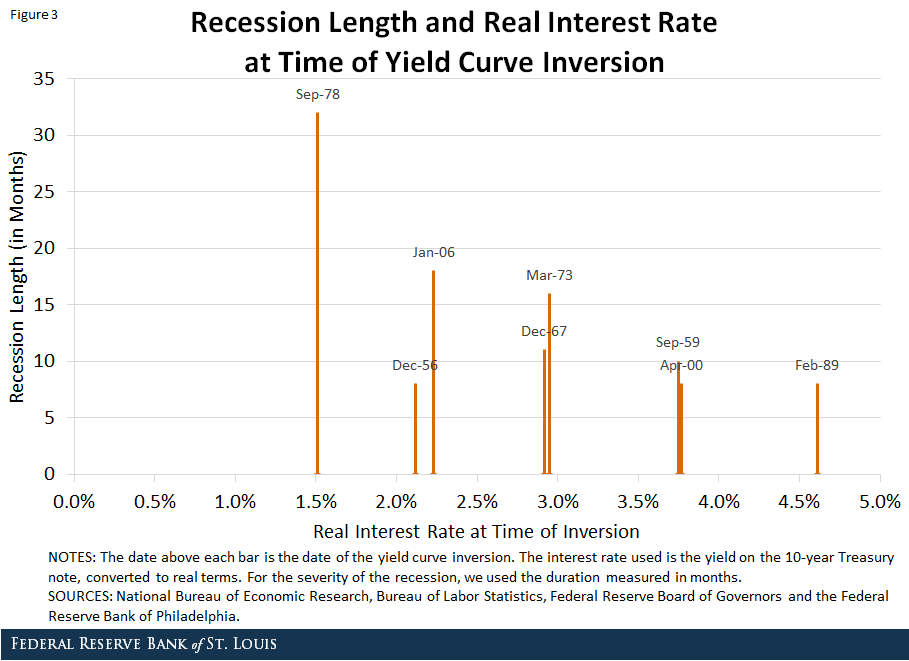

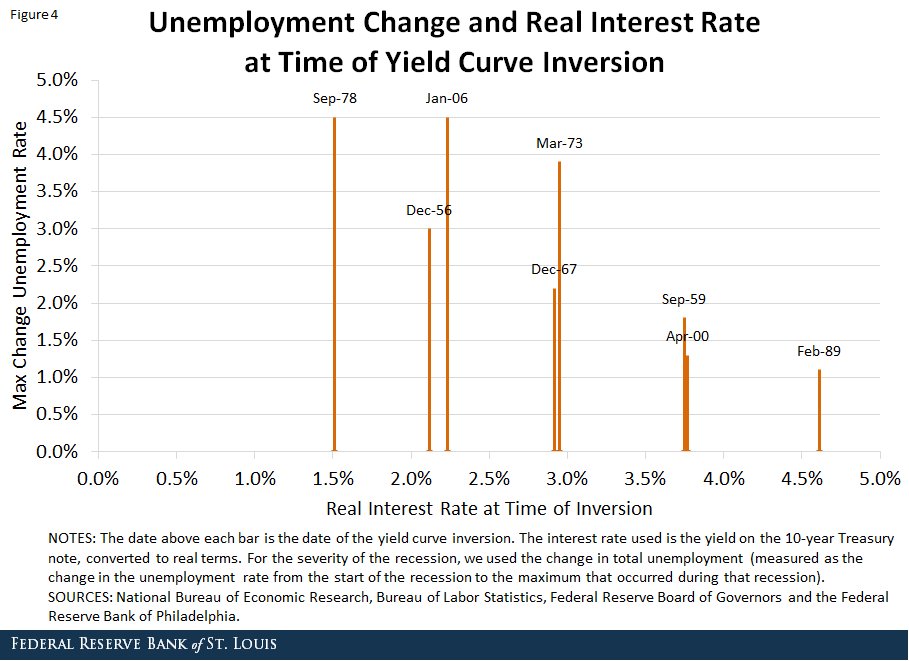

Fed research found 3 strong historical correlations in regards to recession:

#1: Figure 3. The lower the level of the real interest rate, the longer or deeper the recession that follows a yield curve inversion.

#2: Figure 4: The lower the level of the real interest rate, the bigger maximum employment. However there’s a tendency that max unemployment is being capped, unlike recession length/severity.

#3: The lower the level of the real interest rate at time of inversion, the recession is likely inevitable.

Yield curve was inverted around early July 2022 with 10y real interest rate that time was around 1%. Therefore based on this historical correlations:

We might see hard/long recession which may last 3 years, unless there’s a crash in economy. The 3 years number looks to match yield curve recovery.

We might see maximum unemployment of 4.5% over 3 years of period. Unemployment may rise slowly.

The recession is likely inevitable.

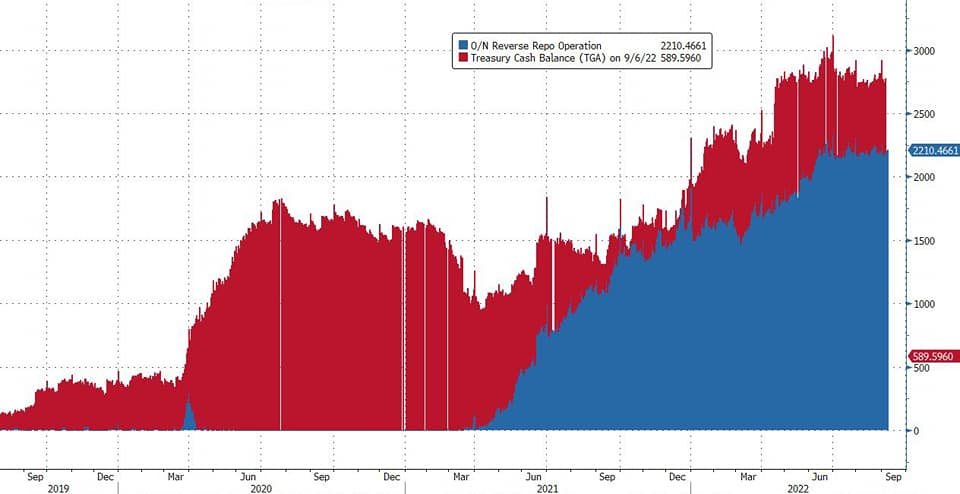

While people are expecting easing from RRP and TGA, in my opinion, they shouldn’t.

RRP is mostly owned by big banks and funds, in which in previous history of 2009-2019 printing cycle, they preferred to circle money among themselves, rather than to inflate people. Therefore we think they would rather use the RRP saving for their own good (avoid crash in economy), receiving free high interest, rather than to support deflated economy.

TGA may find their support, just like recent 1.7T$ omnibus budget approval. With US debt limit at sky high and interest is expected to stay high for long years, their interest is exploding. Therefore I think there will be a rather tendency to have debt limit drama, limiting current democrats ability to inflate economy further.

With our main thesis that inflation will be sticky high for many years, the easiest way to support market is to use public economy number one or their currency. We may see DXY to stay weaker to maximum 95, unnecessary to fall quick.

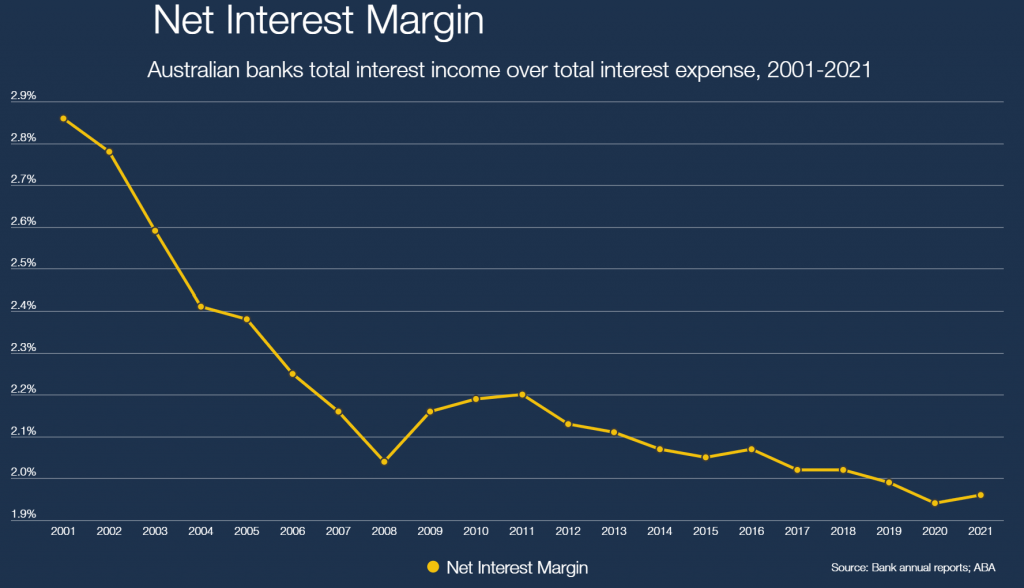

Would it cause GFC? It doesn’t look likely. Banks enjoy higher margin from higher interest. As long as recession is “affordable”, banks are still making profit. This supports our above thesis that the recession will be long and severe. Once economy is unable to afford recession, bank NMI will drop further low. That’s when I expect Central Banks to start pivoting, which is expected to be around year 2024-2025. During that time, people will lose their asset value over interest payment to the banks.

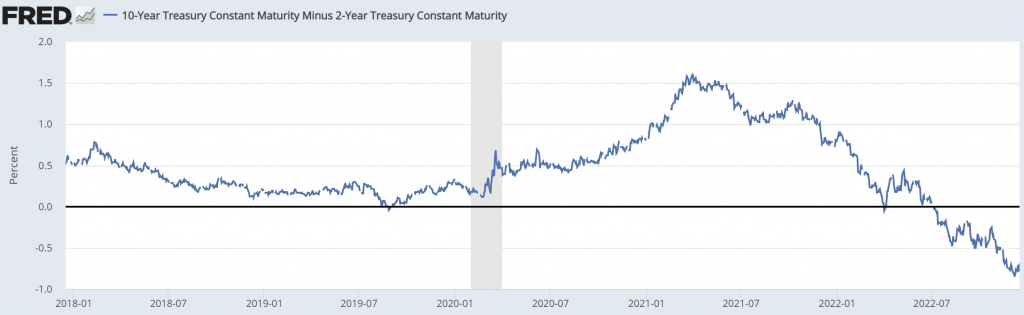

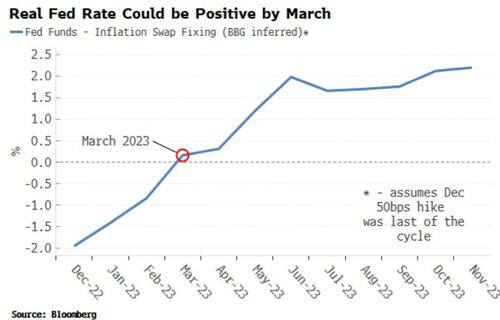

We may also look into 2y vs short term or how much money will move from market into banking systems in advanced countries. If Fed short term 3m ~ overnight exceeds 2y, then we start to see economy takes impact from the Fed move, because money will start flowing from economy to the bank. S&P is only returning 3.5%, therefore if Fed continues to increase rate (3.25%) or 2y is falling with Fed holds rate, money will move from economy and shares into bond/risk off. We can also look into our previous article that government bonds are currently on their face value. If inflation is higher, then gov bonds will be under their face value, offering guarantee to make money beyond their coupon. We expect to see real rate becoming positives in March 2023 or bond is performing better vs inflation.

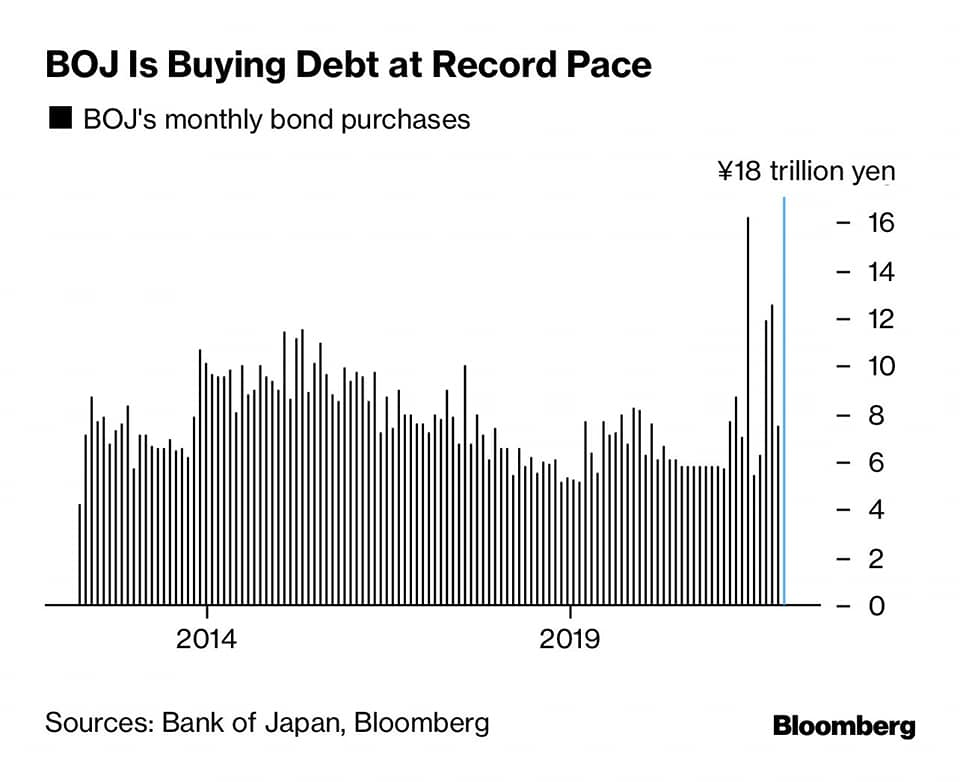

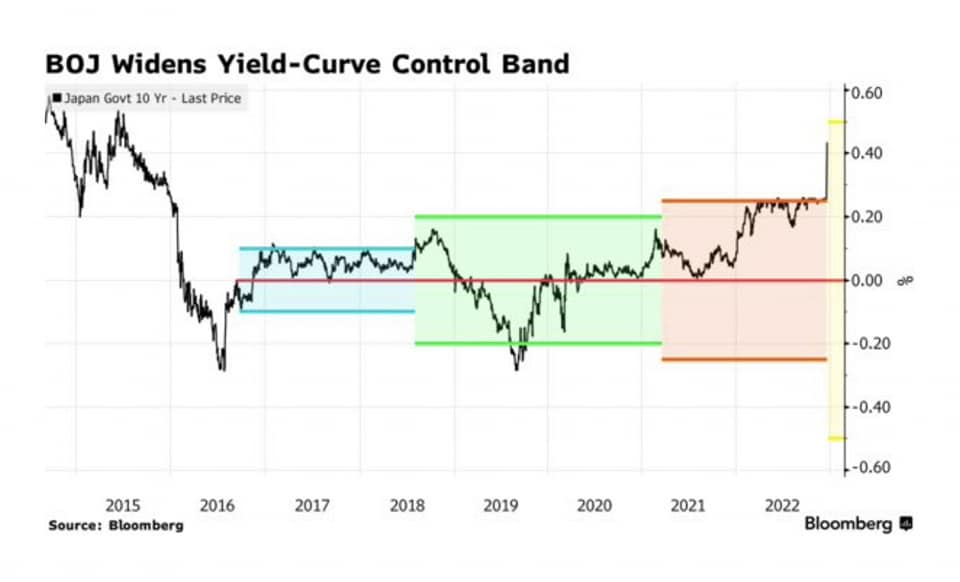

With BOJ recent moves, advanced countries other than Fed has started to push DXY just below their possible weaknesses. With RRP comfortably sit well above 2.2T$ and 1.7T$ approved omnibus, we believe US financial is well prepared enough to sail through possible recession.

We would think to seek barometer from western counterpart strategy, especially China. In our opinion, there could be 3 options:

#1 China opens up their economy big time, less likely

If China opens up their economy big time, we may see spike in global inflation, which will rather excessively spurred emerging money to rather flow into advanced countries bonds. We may see 2007-2009 commodity boom bust cycle repeated in this scenario. In our opinion, this is less likely.

#2 China spurs economy just enough, high likely

This option is supported with few facts:

China continues to mention they will not ease too much like in 2000s.

Australia miners continue to see support every time they run below technical correction.

HSI and SHCOMP continues to see support.

Developers and miners in China continues to receive recovery and support.

AUD, which is sensitive to China economy, looked likely to find support. AUDIDR seemed to bottom few months back and showing emerging ability to ease to support their economy.

Chinese credit impulse starts kicking in BUT not in a big way like before, just enough.

#3 China continues not opening their economy, unlikely

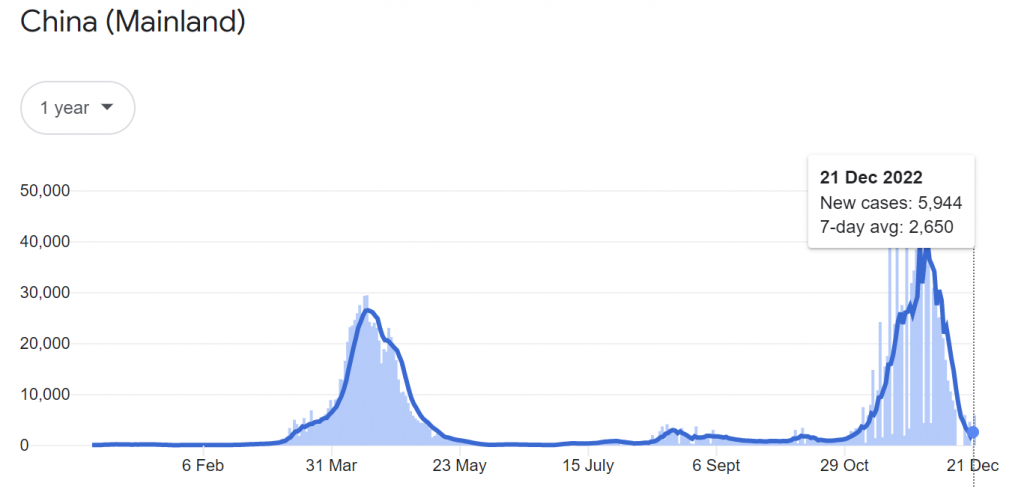

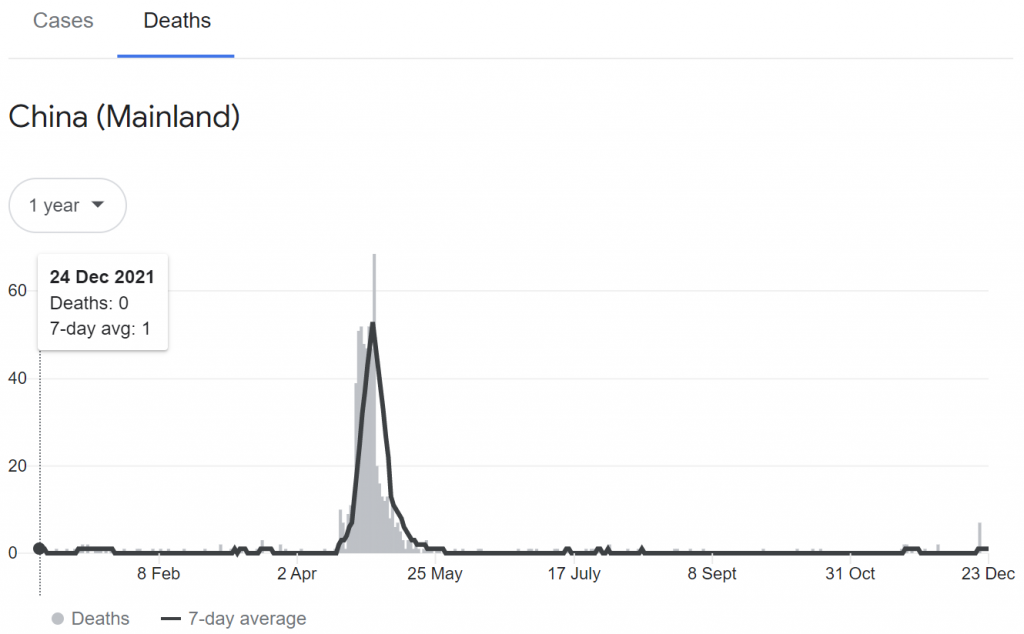

With Covid starts to drop to zero and mass infection, it seems Covid will be gone soon. Current numbers don’t support this option yet unless Chinese government suddenly changes their course overnight, breaking trends. China is also experiencing budget deficit.

We also see commitment from advanced countries to China tends to increase, therefore it’s unlikely there’s a big change/deterioration.

With Fed holds meeting until early February, they will have enough time to see what China will bring into their economy until their Chinese new year on January 22, 2023. Usually China continues to start piling up import prior to Chinese new year.

Therefore our strategy is still same. We had unloaded 30% of our long risky assets during H2 2022, reduce any possible high interest loans, and will continue to unload another 30% during H1 2023. We are expecting to sail 3 years possible recession comfortably. Since we are expecting high inflation to be very sticky and China just enough to spur global growth:

Our strategy is to start with very small investing in 2-3-5 years advanced countries government bonds using our unused cash or cash from property, reasonably.

Continue to hold our commodity thesis with China opening/easing. We expect this to be slow, unlike 2007-2009 commodity spike. There is possibility of sudden “risk-on” in emerging participants, which may cause overshoot and stop Chinese government from easing further. We are expecting the spike to cause a drop in commodity and at around same time government bonds to fall below their face value briefly, in which we will move from commodity into this bond narrative in big size. We could potentially see another 20% return in commodity return before that is happening.

What will we do Cap? We fight!

I assure you brother, the Sun will shine on us again, even if it takes more than a year but not today.

Any idea in this blog and website are my personal own. They are not financial advise.

Continuing our previous article of blow off bounce indication, we were looking to pump and dump more, at least half of our risky assets between Christmas New Year to possibly peak around Easter 2023. We are looking for incoming Christmas Santa Clause rally (blow off) to stay until around Easter. Hopefully the rally is very strong to unload most of our risky assets and fantastic return opportunity as well for those who purchased during past one year windows time.

I still believe in sticky high inflation for years with 5% top terminal rate.

This month, after lower than expected 0.2% mom US inflation, which might give hope of Fed soft landing (2.5% target), the terminal rate is back stable at 5%, accompanied with rebound in risky assets, lower USD and RRP withdraw. It’s stable, which may give impression that 5% is the terminal rate to stay for quite sometime.

After cpi and ppi number

It’s supporting with few factors:

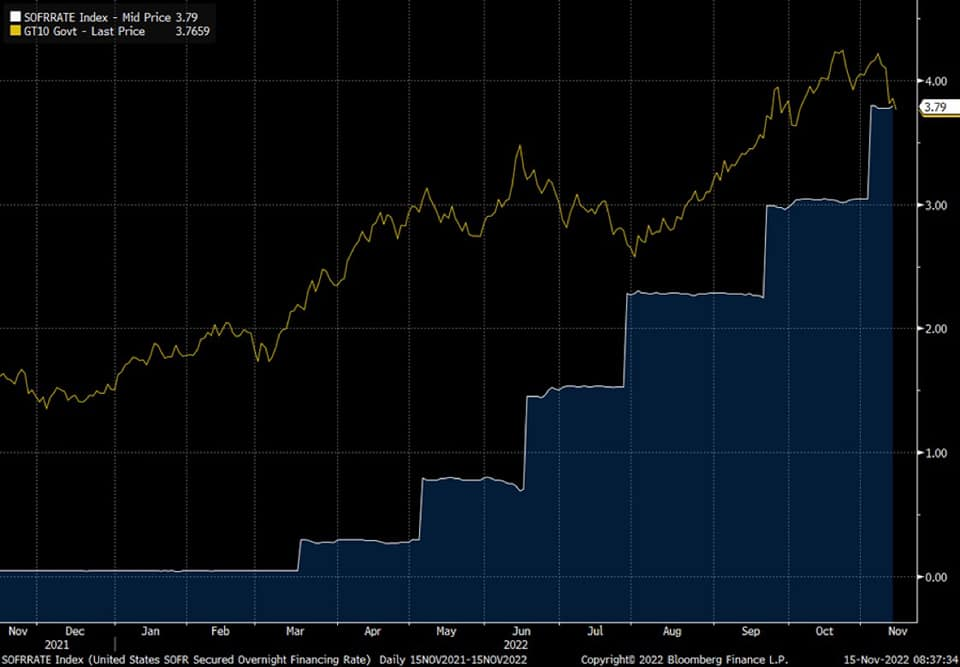

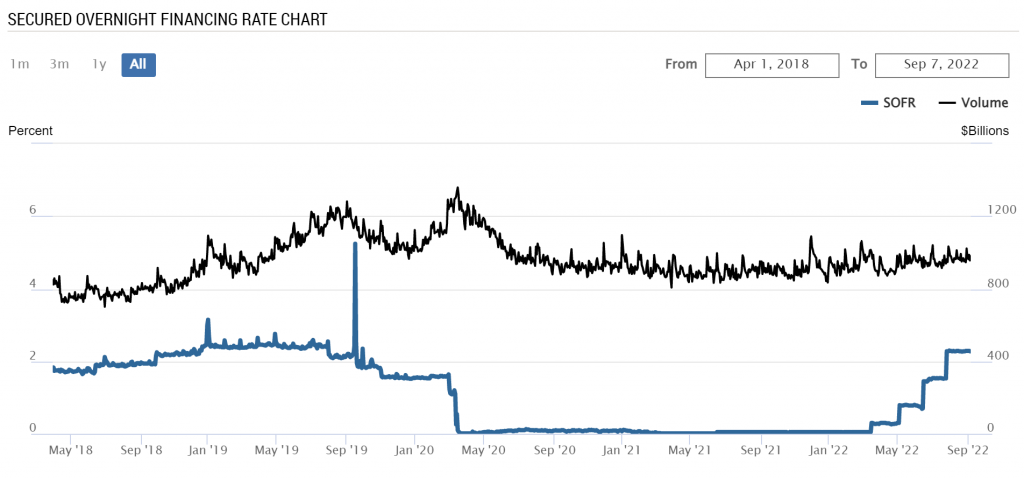

SOFR is starting to go beyond 10y yield, risk off.

government bonds are trying to find face price floor around end of April 2023.

SOFR > TNX

GVM6WU – GSBG23 – 5.5% – April 2023 may indicate a top

GVM6WU – GSBQ26 – 0.5% – may indicate floor to 2026 ~ 10% ~ 2 years high rate

GVM6WU – GSBG27 – possible risky assets peak in 2027 with possible pivot 2025-2027

Of course with bond continue to perform weaker, there’s still a possibility of a bond crash, therefore risk profile in here is not low. However with recent USD, RRP, CPI and PPI moves, we do believe our above thesis might have higher degree.

Even though bonds look to be very compelling, long years of sticky high inflation thesis might easily corrupt their performance in next few years. We will look that inflation threat closer in mid 2023.

This is also supported with significant emerging market moves which could indicate emerging would need to spur their due economies. On Nov 6th, we spot very strong emerging rally.

Our internal research spot emerging rally – Nov 6, 2022.

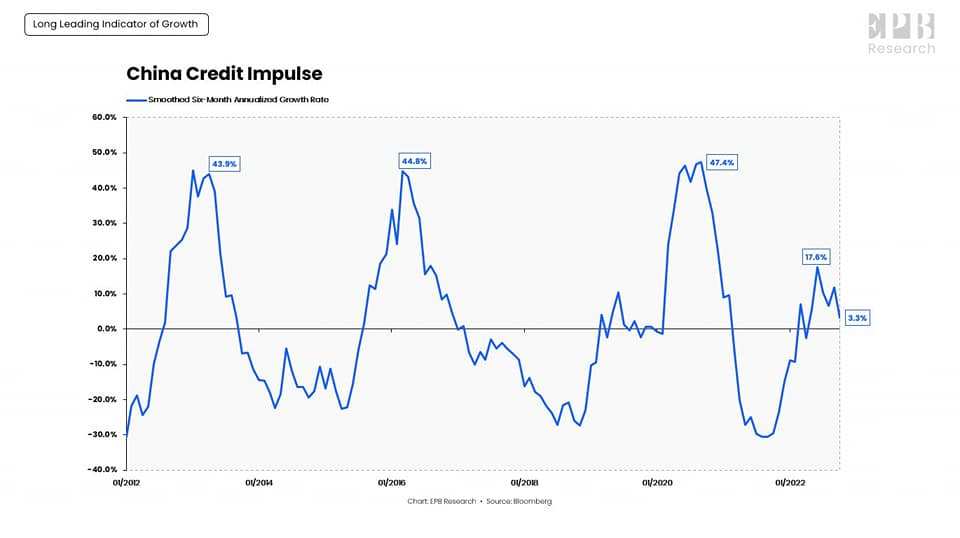

Let’s not forget due China credit impulse:

China credit impulse

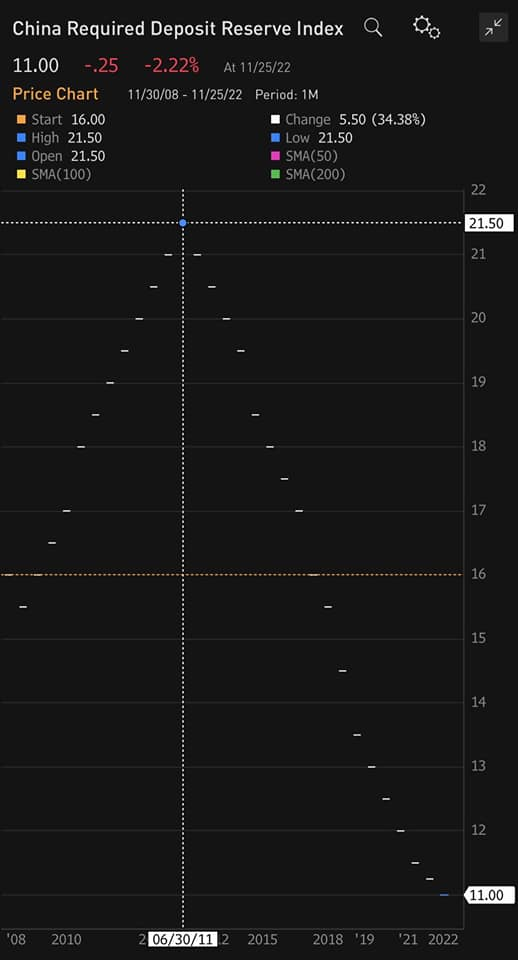

China continues to cut RRR:

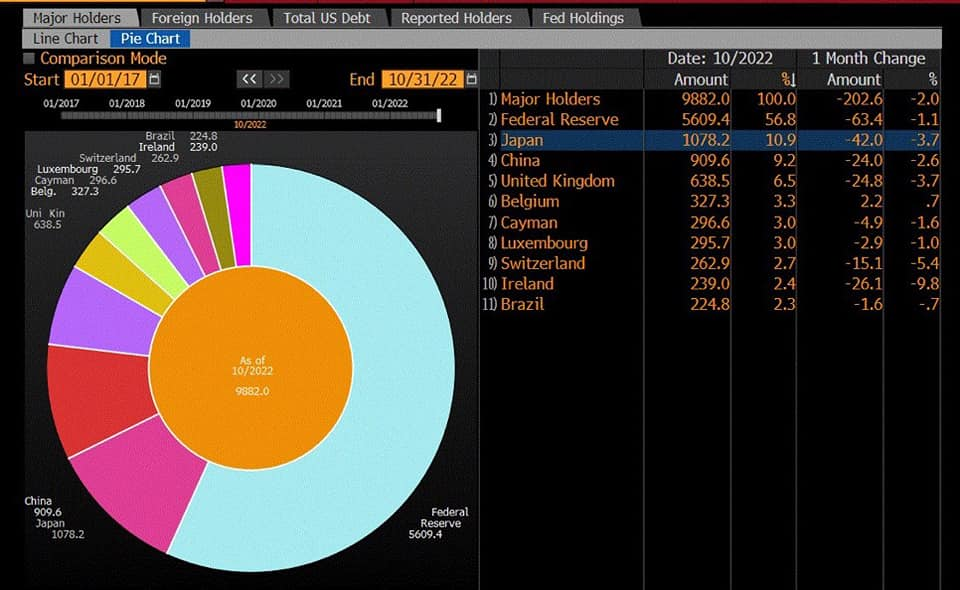

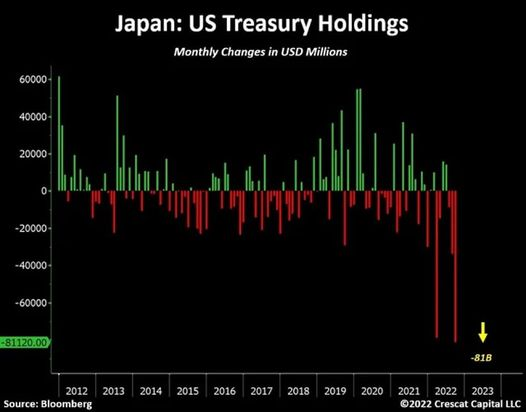

And record selling of US debts from Japan and China:

Swinging into emerging/cycle might introduce volatility which usually is not pleasant.

Looking into advanced countries side, G5 credit impulse might not yet be due like China, therefore I would think it’s a growth transfer from advanced to emerging. With inflation to peak, we may have 6 months for emerging to start their credit impulse to ripe. This thesis might support our main strategy plan.

G5 inflation with 4Q lag

Above thesis is also supported with very bearish VIX, as well as weak USD, despite China and Japan easing. As seen below the risk of VIX and USD rebounds are pretty high, therefore high risk assets may find their very high risk condition to have their possibility to return well.

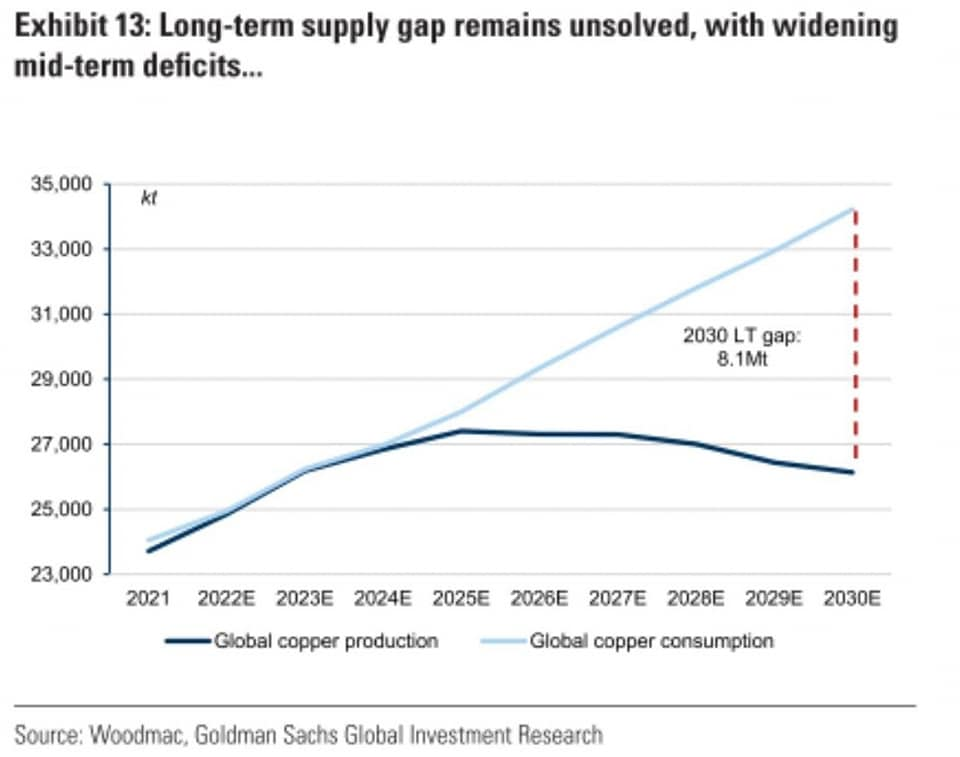

Despite of this situation, in medium 5 years, we should see global growth to continue being strong, indicated by copper. It’s following our long term growth in electrification and EV. We declared top of NASDAQ in November 2021 article and should now be starting again to collect back technologies, including our EV thesis, which may find some ground in December 2022 with early 2023 US government supports. It’s however without risk, please be extra careful with increasing high risk, which is due next year.

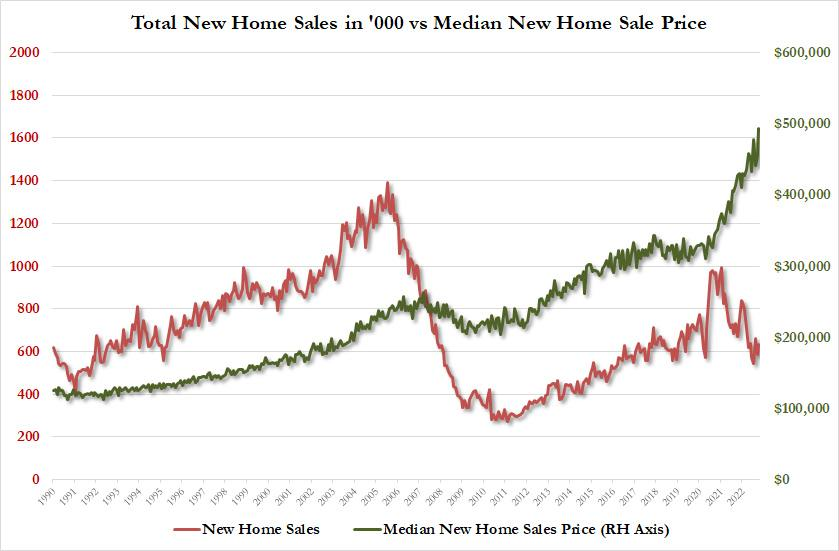

Our research in future numbers in economy basically indicates lower volume and higher price. It will put pressure to economies who are failed to adapt. It’s similar to new home sales of US house, lower sale volume but higher price, indicating strong fundamental, land plus development cost, and not crazy price increase bonanza past 3 years due to relative zero rate. Please be aware, not to be confused with premium house price few years back due to very low rate.

In term of balance sheet, I would reiterate our previous articles. Fed balance sheet might start to fall by little which should be offset with RRP. In this money transfer, it’s usually a transfer of wealth with easing to those front running them.

I wish you Christmas luck in every avenue and look forward into life change challenge next year!

It’s beginning to look a lot like Christmas Toys in every store But the prettiest sight to see is the holly that will be On your own front door

Sure, it’s Christmas once more

Wishing you A Lot of Lucky (RED) profit – Red in China / Emerging is Luck

Any idea in this blog and website are my personal own. They are not financial advise.

When The Fed started to raise rate at the end of 2021, negative yield, (reflected in strong commodities), tried to support market price until mid of the year (leaving only commitment ones). It was ended with a bang in CPI/inflation number, a beauty of delayed market expectation, an architect in play.

Fall of negative yield was completed in June 2022

It should be easy to understand current financial situation. If current bank deposit is offering 4%-5% pa, all secondaries should already be beyond 8% or 10% pa. Their returns are so compelling, making any new equity and property investment no longer attractive.

plenty of multi years equity investment with dividend below 4% pa is no longer attractive. In matured companies, their dividend may reflect true value of their operation return.

plenty of multi years property investment with net return below 4% pa is no longer attractive. Low rate has made property investment returning below 3% pa in past decade. Recently, mortgage rate has jumped to nearly 100%, while rental income in premier location such as CBD is hardly making 18% increase.

What does make them no longer attractive? Multi years of easing has caused their price, their denominator, expensive. Equity investment to borrow and personal loans are now going higher than 8.6% pa. Due to the condition, many funds are now offering 8% pa, even a simple strategy to pay off mortgage itself is on track to 7%-8% pa return. It makes no sense for almost all of investors, including us, to take such high risk since early this year. We also have no interest to return back our 25% deleveraged portfolio since June 2022. We will continue to allocate them into high return safer vehicles, possibly in very long years, next 3 years or so.

Please be very careful with any investment offering 10-12% pa return, which is tied up with any risky assets, including property. We strongly advise to avoid any of these because they have very high probability of going bankrupt. Most medium to small companies will be struggling to survive, even with interest rate as much as 8% pa.

We keep holding our thesis that high interest rate will stay for multi years. We believe most investors have biggest mistake in mind at the moment. They are still thinking that Central Banks and authorities will pivot again or help them again nearly soon, just like happening in past decades. I think current situation is much different to past, which most people don’t realize. I believe inflation this time will be very sticky, high interest will be here to stay, not only a year or two, but may be over 3 or 5 years. My two biggest arguments are:

there’s no indication of pain in real economy numbers like in previous cases. Unemployment is still very low, big companies are still making money.

there’s no indication of low liquidity from the biggest holders of this game, like banks and funds. Banks are still holding too much liquidity, reverse repo is still not indicating any requirement of the market to seek help, indeed front end treasury is still offering very attractive value.

Oh yes, I truly understand market in general is in pain, seeking for help. However in my experience, this argument is not enough for the authorities to pivot. It’s the hidden reset. To explain in a simple math; if mortgage rate is running just 7% pa for 5 years, property price doesn’t increase and barely make return on their depreciation advantage, it will loose over 40% of their property value, in form of interest. I was living in Asian country during Asia crisis 1997, current 7% pa inflation is nothing, compared to what I experienced.

Therefore since June 2022, since commodities were no longer able to support aggressive rate increase to terminal, we have been deleveraging our position to around 25% from all of our general investments. We should not fight the Federal Reserve in our general investments, whether they are in bonds, fixed incomes, equities or properties. Of course, there’s no need to be panicking, even though we are still planning to offload another 10%-20% of our investments, which could mark our fastest deleveraging across the board. Once completed, we would be near to borrowing free to grow fundamentally better with much less risky assets.

Of course since there’s no pivot, there is still some selected investments to grow, reasons below.

In previous financial crisis, bonds and debts were mostly performing much better than equities or risky assets. This is not the case at the moment. This should support our initial argument in which inflation issue is quite severe, which caused bond to suffer much harder (bond is sensitive to inflation/loss value of money), rather than equities (real economy or sufficient liquidity). It’s more making sense to support our second argument, high rate may last much longer and cause longer pain. Therefore it’s our strategies to reduce most of our leveraged investments. As much as high inflation may instead reduce debt value, we believe the situation may come after inflation is near to their end, not when inflation is still on rise. I’ve been studying inflation for many decades and this is in my own opinion only.

There should be lots of big dead cat bounce in equities, but some of them may perform well, since they are still performing better than bonds. If the Fed is not supporting banks with their treasury holding loss, US might have similar bad condition, just like happening with GILT and JGB.

We can also proxy from gold price. As much as authorities are trying to save market price, the bottom is still far away from gold normal price. It’s also our thesis in 2019, we believed gold and inflated price were so overvalued, and it requires lots of efforts, pain, and MULTI YEARS to normalize them.

Of course, we should acknowledge that the US is still having quite a lot of liquidity in their USD currency, bank deposits, RRP and TGA. Sometimes we also need to question why the Central Banks are targeting financial tightening in general, rather than targeted ones. Treasury and green money may then support big companies, it’s not just too big to fail, but it’s also too big to not winning their competition. These companies may then have enough ammunition to conduct merger and acquisition, a situation to see, before we decide to take commitment again in big investment.

Let’s track again when it’s all started. Last year, one year ago, we wrote in our article that the investment windows would be closed in one year. Easing was exciting, then came the Fed compromises with tightening. Then good became bad and bad becomes worst.

A possible short-lived peaked inflation thesis, which may lead to slowing down of rate raise expectation.

There is an indication that raising rate rise may no longer be effective to support USD. Therefore I believe, the Fed may soon reach their terminal rate.

We shouldn’t expect Central Bank to pivot. Painful multi years of high rate and inflation are instead deciding our fate. High rate is what gives value investment a meaning. To know it would be painful, we should hold our deleveraged assets and running short. It’s our strategy to keep our deleveraged assets into longer term fundamentally strong vehicles and may take short term trade position only, if any, with much smaller size. High inflation and rate will wipe out 50% of our living financial creatures. We will patiently wait, until there is a lot of merger and acquisition from big companies.

No one ever is. We don’t get to choose our time.

Death is what gives life meaning. To know your days are numbered. Your time is short.

Any idea in this blog and website are my personal own. They are not financial advise.

As we discussed in early July 2022, there was a rumour that rebound would come due to the Fed pivoting. It was based on historical events that the Fed has to start pivoting at some point of time. I personally argued strongly that this time is different. During that historical events, either market:

had lowest liquidity,

had inflation peaking and starting to go lower,

had decreasing US/global economy,

had decreasing long term rate,

was in recession.

but none of these arguments is currently happening.

stable SOFR

Don’t get confused with oil/Romeo crashing to lower low. If we use human made engineered inflation indication, market will cheer lower inflation. However it’s still in our thesis, real money inflation will continue to be sticky. Therefore despite lower number and lower oil, we may continue to see higher rate. Historically, policy markers are going to lean more towards money rather than economy. Also don’t get confused that it will lead into recession. No, it’s not, at least for now. Have a look into how emerging economies passed their high money inflation between 2010 to 2019, before they fall this decade. This is where money is going to play around with economy theories since people usually got wrong, because they only rely on some part of the truth, but not the whole truths.

Fighting the Fed is a suicidal act. The Fed is still the strongest player in this market. Despite their uncomfortable tightening, I wrote few times that I still believe the Fed is still going to take care the market, despite at the end of it, they might have to give up to barons. However before that, in long journey of our life, before death comes, I believe the Fed will continue to take care the market, in their own way of course.

This is where assumptions in market got wrong and messed up. Pivoting is situation where central bank will effectively move market according to baron goals. However based on research published in 2010s, the Central Banks are mostly market followers and not market decision maker. So how is that so? In my own formula, I found that the Central Banks policy are only mostly effective during market melt down, either when they are at their most undervalued or at their most overvalued, but NOT during market movement, or when liquidity is abundant. They have principal as well to not affecting market too much unless necessary. Current rate raise is not market control but market follow. This is why I will continue to argue market pivoting for now. We must not reason this market rally with pivoting idea. It will get wrong at the end. We should reason market rally with correct reason, therefore we could still get right at the end of it to play hard and exit correctly.

Arguments for no pivoting are: (1) liquidity is still too high, market is still more powerful than central banks (2) US is still the only player. History told strong player (the US in this case) always takes advantages over any weaker ones, market competition idealism. These two main examples alone in my own experience opinion, are enough to argue pivot thesis. YCC (Yield Curve Control) is another dynamic where pivoting may seem to work but in my opinion YCC is only going into costly terminally ill monetary systems.

However very important to understand, no pivoting doesn’t mean that market will fall. As indicated by money figure, following by economy data, there’s absolutely no reason for the Fed to blink. We are not going to go against the Fed but we do believe the Fed is in situation that they are now following the market or in auto pilot mode. They may use CPI or CPE, but the main idea is the Central Bank is not in situation that they can or need to put their strong arm on yet.

It’s still in my opinion that the market is still fabulously strong. However market participants, especially strong ones already felt the heat of overcrowded and heated market, therefore they should work, followed by the Fed to slow that one, before as mentioned by the Fed and that is true, the cost of persistent too high inflation is too much. It’s already reflected in cost in debt market.

If we look into some big companies, their PE is still very healthy. Most big companies are still making good money despite increasing cost. This is also one good reason for them to support tightening efforts. As we also see, funds are getting more concentrated into few. With liquidity at highest and concentration at lowest, it will only create a situation of more control and make more, rather than distributed wealth to just everyone. It’s also indicated in situation that low rate era is ended and only those who don’t swim naked will survive. It’s in my thesis that we will see spectacular rally of big companies.

Of course back to my main money theory, despite their huge wealth, to continue their rally, they will influence government support to ensure their operation is secure. Green support, chip industry support etc must continue to drive their healthy condition to make an amazing rally. Therefore we continue to concentrate our portfolio into healthy individuals only.

I’m so powerful. I don’t need batteries to play.

We should look closely to how DXY continued to march higher but despite its massive spike, we clearly see market is building very strong positive divergence momentum. That should mean, current Fed rate and USD spectacular rally are definitely not strong enough to stop market rally, imagine if they DID NOT. That’s why in our thesis, we should interpret the Fed rate raise above market expectation in June as a panic to anticipate super bullish catastrophe.

USD as almost crashed in June, triggering very high inflation (inflation higher than estimation). Instead, the Fed increased them to give enough time for them to raise rate. As consequences, USD continues parabolic until it’s stalled. However as we can see in market index momentum, they are not crashing but instead forming a strong positive momentum. Would this scenario is true, it makes more sense that the Fed is still knowledgeable and able to anticipate better, unlike many social news bait theories. I would rather believe the Fed and USD have been quite successful to contain most of bullish beast for now.

I’m unstoppable. I’m a Porsche with no brakes.

The market has been all wrong with the idea of economy. In my number one money theory, the money decides and not the economy. This article may show another failed Goldman Sachs media version prediction.

However risk is not going to leave us. We would see more pain into small companies and countries. I’m not going to argue massive hedging that they could probably hedge market in general but continue long their main portfolio, since finding good companies that will continue their rally to the finish line will be very rare. Would that be correct, it will distinguish us from the rest of market player.

I put my armor on, show you how strong how I am. I put my armor on, I’ll show you that I am.

Any idea in this blog and website are my personal own. They are not financial advise.

I simplify my investment principles into 3 factors (from my 25 years of experience in economy):

money

power

enthusiasm

Money

This is the most important factor in my investment decision, which I think will be able to explain todays mysteries and is still important to next few years. I hold my money theories above all, including any economy theories.

In my money theory, we usually have big rally when:

money easing has been decided. People get this wrong with when economy is in worst shape (depression, recession, etc). It’s incorrect. Economy only turns when money easing is already decided, not because of the bad shape of economy.

rally is on their last leg/blow off. This is usually an artificial rally, for example due to:

big devaluation of currency, e.g. commodity rally between 2005-2008

big structural issue in bonds due to 60:40 bond:stock for example.

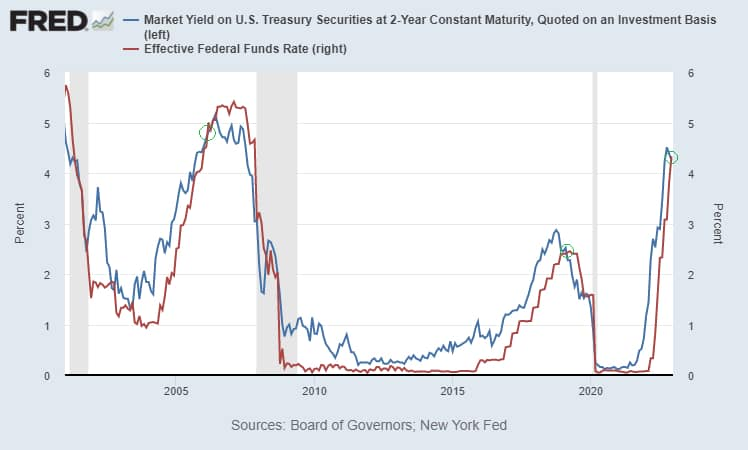

Regardless of any recession possibilities, the USA still has 3 big money supports and for me that’s enough, getting stronger when SOFR is not affected by July 2022 rate raise.

RRP ~ 2.1T$

TGA – treasury

very strong currency – USD

Abundant liquidity remains, delayed QT thesis remains flawed rather than run-off

Power

In my second investment principle, successful investment should be supported with power, ability to control, win competition (unfairly if required), and less risk with possible bailout/golden parachute. This underlines our investment principle to stay only with big firms (overweight in index) and only little amount with small companies. We may only give exemptions to small companies when they are having relationship with strong power such as government supports or excessive economy structural supports.

Big firms usually have ability to drive public money decision making, and they would have less risk due to ‘big to fail’. They are hard to get manipulated easily as well. We also hold strongly our thesis, that even if in the event of correction or crash, the big ones usually have opportunity to rebound stronger and earlier. We may not get confused with this month small company rally, which might be related to their over positioned short position and excessive correction. They may not yet guarantee long term rally. If we look into Berkshire investment portfolio, more than 80% of their investment today are concentrated into only 5 to 8 big companies.

I also worry economists which could easily be driven wrongly with CPI and PPI numbers (and their formula). Whether power had been practising in dirty shirt emerging economy between year 2010 and 2015, we should learn how emerging market could pass on their real high inflation between that time in artificial CPI and PPI numbers. The power could easily adjust the numbers and confuse economists.

However we should not take these money and power principles easily, when they have been abused excessively. Apple is an example of money and power abuse. They may lack evolution/enthusiasms after their excessive rally over years. It’s example of money and power, but to purchase their current price is too risky for us (indeed supporting that they may continue their rally). It’s an example that I must use my principles considerably with price factor.

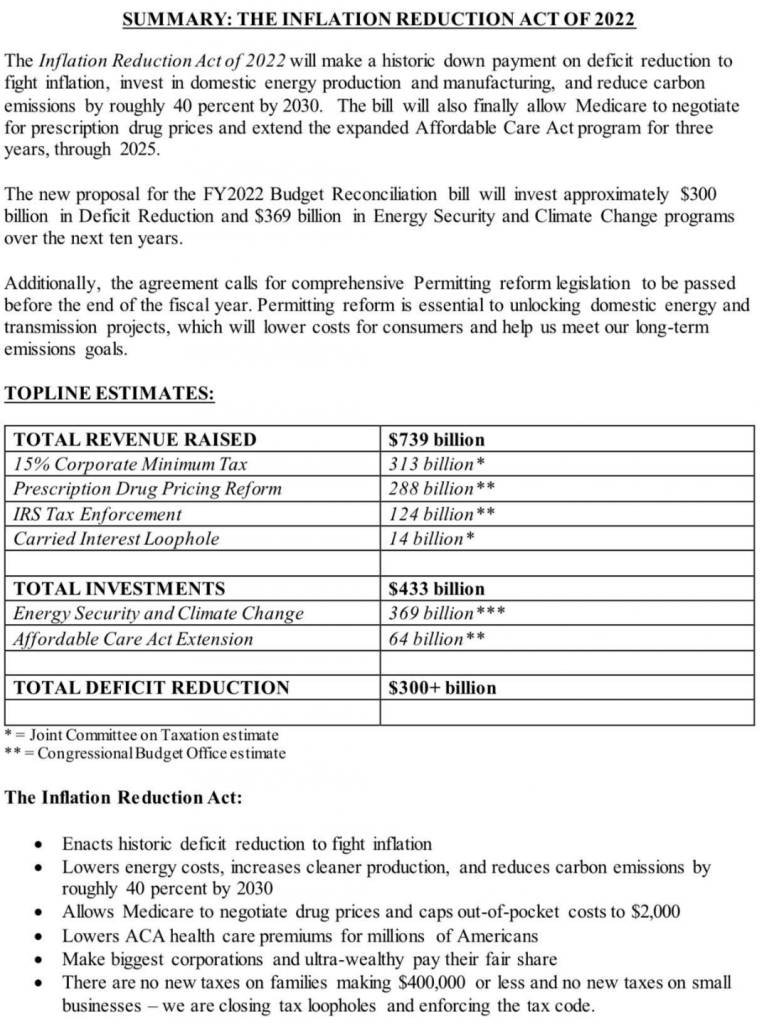

We should see how policies are playing important aspects in driving price control. Record of stimulus, power to decide interest rate, inflation reduction act (which is also money), for examples, can drive next Estafet of rally. Recent example of inflation reduction act may benefit certain individuals or parties, such as billionaire tax loophole in return of their other benefit of more money to reduce inflation (double benefits).

We should see many mining companies benefit with defence protection acts. We should also notice small mining companies can only survive their mining defence from any “terrorism” when they signed strong agreement with “those who own the sea”. It’s showing how power is becoming our second most important factor. Other example, Space X is becoming important in defence spaceships and may benefit their related companies.

We still hold our thesis in EV strong since year 2020. We did acknowledge NASDAQ risk in December 2021 when NASDAQ must go down their hills to normalize their huge rally, in return to higher yield and inflation/higher USD. However after this mid year 50% correction from their peak, we may think that the normalization thesis may have been completed. Recent EV credit (370b$ for next 10 years) is a support to our EV evolution thesis. It may help EV industry to compete (fairly and unfairly) and raise their price from near to almost free. We emphasize many times in our articles past few years, that market rally may also be related to our third investment principle, Enthusiasm.

Enthusiasm

enthusiasm is intense and eager enjoyment, interest, or approval

I think there are 3 aspects of enthusiasms: